Triangular Moving Average Crossover Trading Strategy

Author: ChaoZhang, Date: 2024-01-16 18:18:02Tags:

Overview

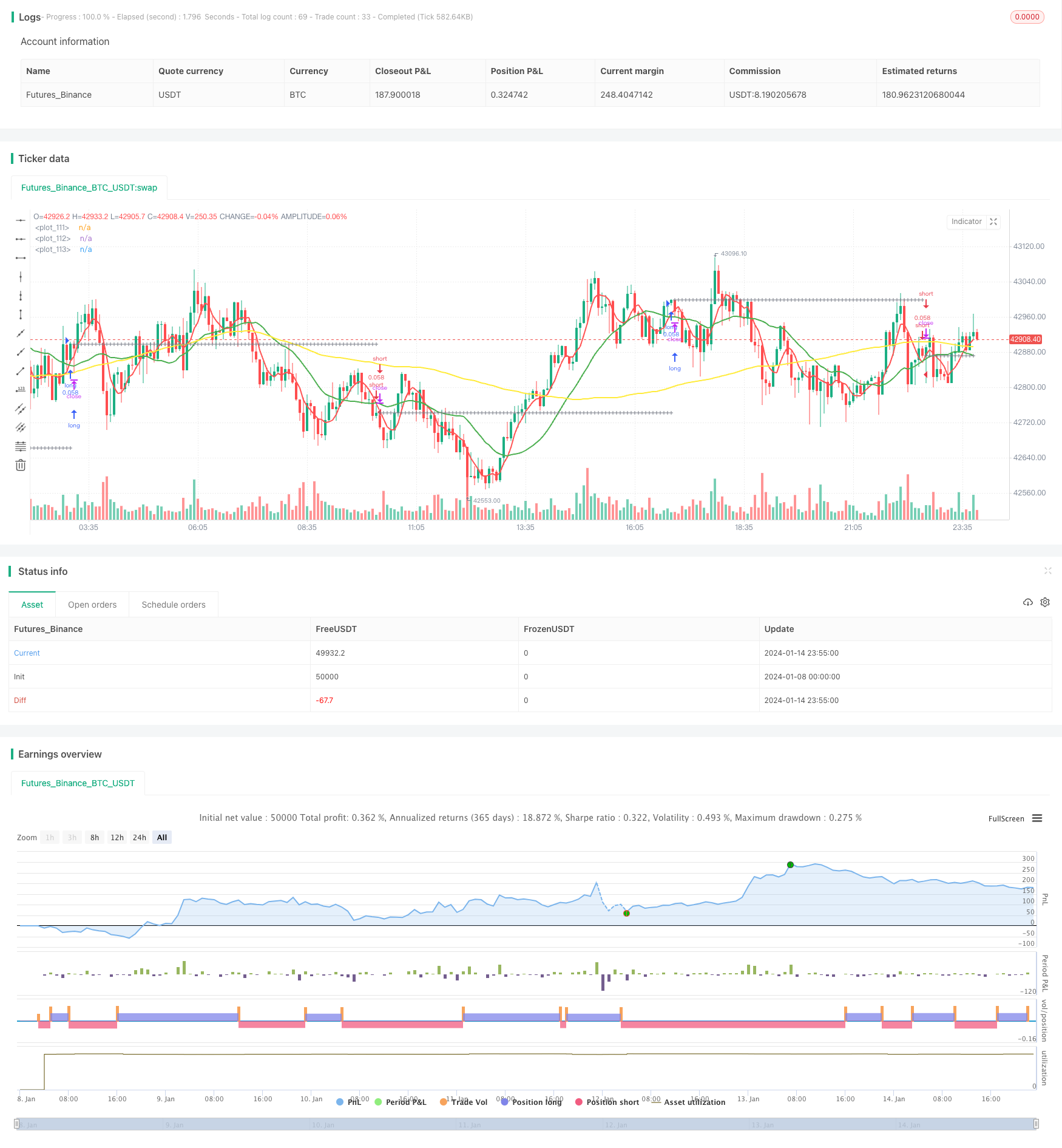

The Triangular Moving Average (TMA) Crossover trading strategy is a typical technical analysis strategy. It utilizes three moving average lines of different time lengths to capture trends and implement low-risk trading. When the short-term moving average crosses over the medium-term moving average upwards, and the medium-term moving average is above the long-term moving average, a buy signal is generated. When the short-term moving average crosses below the medium-term moving average downwards, and the medium-term moving average is below the long-term moving average, a sell signal is generated.

Strategy Logic

The TMA strategy mainly relies on three moving average lines to determine the trend direction. The short-term moving average responds sensitively to price changes; the medium-term moving average provides a clearer judgment of the trend; the long-term moving average filters out market noise and determines the long-term trend direction.

When the short-term moving average crosses over the medium-term moving average upwards, it indicates the price has started to break out upwards. At this time, if the medium-term moving average is above the long-term moving average, it means the current market is in an uptrend. Therefore, a buy signal is generated here.

On the contrary, when the short-term moving average crosses below the medium-term moving average downwards, it indicates the price has started to break out downwards. At this time, if the medium-term moving average is below the long-term moving average, it means the current market is in a downtrend. As a result, a sell signal is generated.

This strategy also sets stop-loss and take-profit lines. After entering a trade, stop-loss and take-profit prices will be calculated based on the percentage settings. If the price touches either line, the position will be closed.

Advantage Analysis

- Utilize three moving averages together to improve judgment accuracy

- Set stop-loss and take-profit to effectively control per trade risk

- Customizable moving average parameters suitable for different products

- Seven options for moving average types, diversified strategy types

Risk Analysis and Solutions

-

Wrong signals when three MAs are consolidating

Solution: Adjust MA parameters properly to avoid wrong signals

-

Over-aggressive stop-loss/take-profit percentage

Solution: Fine-tune percentages; cannot be too big or too small

-

Improper parameter settings leading to too many or too few trades

Solution: Test different parameter combinations to find optimum

Optimization Directions

The TMA strategy can be optimized from the following aspects:

-

Test different type and length combinations to find optimum

Test different MA length or type combinations for best results

-

Add other technical indicators as signal filters

Add indicators like KDJ, MACD etc. for multi-factor verification

-

Select parameters based on product characteristics

Shorten MA periods for volatile products; Lengthen periods for steady products

-

Utilize machine learning to find optimum parameters

Auto parameter sweeping to quickly locate optimum

Conclusion

The TMA Crossover strategy is an easy-to-use trend following strategy overall. It utilizes three MAs together to capture trends and sets stop-loss/take-profit to control risks, enabling stable profits. Further improvements can be achieved through parameter optimization and integrating extra technical indicators. In conclusion, this strategy suits investors seeking steady gains.

/*backtest

start: 2024-01-08 00:00:00

end: 2024-01-15 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy("Kozlod - 3 MA strategy with SL/PT", shorttitle="kozlod_3ma", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 5)

//

// author: Kozlod

// date: 2018-03-25

//

////////////

// INPUTS //

////////////

ma_type = input(title = "MA Type", defval = "SMA", options = ['SMA', 'EMA', 'WMA', 'VWMA', 'HMA', 'SMMA', 'DEMA'])

short_ma_len = input(title = "Short MA Length", defval = 5, minval = 1)

short_ma_src = input(title = "Short MA Source", defval = close)

medium_ma_len = input(title = "Medium MA Length", defval = 20, minval = 2)

medium_ma_src = input(title = "Medium MA Source", defval = close)

long_ma_len = input(title = "Long MA Length", defval = 100, minval = 3)

long_ma_src = input(title = "Long MA Source", defval = close)

sl_lev_perc = input(title = "SL Level % (0 - Off)", type = float, defval = 0, minval = 0, step = 0.01)

pt_lev_perc = input(title = "PT Level % (0 - Off)", type = float, defval = 0, minval = 0, step = 0.01)

// Set initial values to 0

short_ma = 0.0

long_ma = 0.0

medium_ma = 0.0

// Simple Moving Average (SMA)

if ma_type == 'SMA'

short_ma := sma(short_ma_src, short_ma_len)

medium_ma := sma(medium_ma_src, medium_ma_len)

long_ma := sma(long_ma_src, long_ma_len)

// Exponential Moving Average (EMA)

if ma_type == 'EMA'

short_ma := ema(short_ma_src, short_ma_len)

medium_ma := ema(medium_ma_src, medium_ma_len)

long_ma := ema(long_ma_src, long_ma_len)

// Weighted Moving Average (WMA)

if ma_type == 'WMA'

short_ma := wma(short_ma_src, short_ma_len)

medium_ma := wma(medium_ma_src, medium_ma_len)

long_ma := wma(long_ma_src, long_ma_len)

// Hull Moving Average (HMA)

if ma_type == 'HMA'

short_ma := wma(2*wma(short_ma_src, short_ma_len / 2) - wma(short_ma_src, short_ma_len), round(sqrt(short_ma_len)))

medium_ma := wma(2*wma(medium_ma_src, medium_ma_len / 2) - wma(medium_ma_src, medium_ma_len), round(sqrt(medium_ma_len)))

long_ma := wma(2*wma(long_ma_src, long_ma_len / 2) - wma(long_ma_src, long_ma_len), round(sqrt(long_ma_len)))

// Volume-weighted Moving Average (VWMA)

if ma_type == 'VWMA'

short_ma := vwma(short_ma_src, short_ma_len)

medium_ma := vwma(medium_ma_src, medium_ma_len)

long_ma := vwma(long_ma_src, long_ma_len)

// Smoothed Moving Average (SMMA)

if ma_type == 'SMMA'

short_ma := na(short_ma[1]) ? sma(short_ma_src, short_ma_len) : (short_ma[1] * (short_ma_len - 1) + short_ma_src) / short_ma_len

medium_ma := na(medium_ma[1]) ? sma(medium_ma_src, medium_ma_len) : (medium_ma[1] * (medium_ma_len - 1) + medium_ma_src) / medium_ma_len

long_ma := na(long_ma[1]) ? sma(long_ma_src, long_ma_len) : (long_ma[1] * (long_ma_len - 1) + long_ma_src) / long_ma_len

// Double Exponential Moving Average (DEMA)

if ma_type == 'DEMA'

e1_short = ema(short_ma_src , short_ma_len)

e1_medium = ema(medium_ma_src, medium_ma_len)

e1_long = ema(long_ma_src, long_ma_len)

short_ma := 2 * e1_short - ema(e1_short, short_ma_len)

medium_ma := 2 * e1_medium - ema(e1_medium, medium_ma_len)

long_ma := 2 * e1_long - ema(e1_long, long_ma_len)

/////////////

// SIGNALS //

/////////////

long_signal = crossover( short_ma, medium_ma) and medium_ma > long_ma

short_signal = crossunder(short_ma, medium_ma) and medium_ma < long_ma

// Calculate PT/SL levels

// Initial values

last_signal = 0

prev_tr_price = 0.0

pt_level = 0.0

sl_level = 0.0

// Calculate previous trade price

prev_tr_price := (long_signal[1] and nz(last_signal[2]) != 1) or (short_signal[1] and nz(last_signal[2]) != -1) ? open : nz(last_signal[1]) != 0 ? prev_tr_price[1] : na

// Calculate SL/PT levels

pt_level := nz(last_signal[1]) == 1 ? prev_tr_price * (1 + pt_lev_perc / 100) : nz(last_signal[1]) == -1 ? prev_tr_price * (1 - pt_lev_perc / 100) : na

sl_level := nz(last_signal[1]) == 1 ? prev_tr_price * (1 - sl_lev_perc / 100) : nz(last_signal[1]) == -1 ? prev_tr_price * (1 + sl_lev_perc / 100) : na

// Calculate if price hit sl/pt

long_hit_pt = pt_lev_perc > 0 and nz(last_signal[1]) == 1 and close >= pt_level

long_hit_sl = sl_lev_perc > 0 and nz(last_signal[1]) == 1 and close <= sl_level

short_hit_pt = pt_lev_perc > 0 and nz(last_signal[1]) == -1 and close <= pt_level

short_hit_sl = sl_lev_perc > 0 and nz(last_signal[1]) == -1 and close >= sl_level

// What is last active trade?

last_signal := long_signal ? 1 : short_signal ? -1 : long_hit_pt or long_hit_sl or short_hit_pt or short_hit_sl ? 0 : nz(last_signal[1])

//////////////

// PLOTTING //

//////////////

// Plot MAs

plot(short_ma, color = red, linewidth = 2)

plot(medium_ma, color = green, linewidth = 2)

plot(long_ma, color = yellow, linewidth = 2)

// Plot Levels

plotshape(prev_tr_price, style = shape.cross, color = gray, location = location.absolute, size = size.small)

plotshape(sl_lev_perc > 0 ? sl_level : na, style = shape.cross, color = red, location = location.absolute, size = size.small)

plotshape(pt_lev_perc > 0 ? pt_level : na, style = shape.cross, color = green, location = location.absolute, size = size.small)

//////////////

// STRATEGY //

//////////////

strategy.entry("long", true, when = long_signal)

strategy.entry("short", false, when = short_signal)

strategy.close("long", when = long_hit_pt or long_hit_sl)

strategy.close("short", when = short_hit_pt or short_hit_sl)

- Extreme Short-term Scalping Strategy

- Optimized EMA Crossover Strategy

- MA Turning Point Long and Short Strategy

- RSI Target and Stop Loss Tracking Strategy

- RSI Indicator Based Short-term Trading Strategy

- Moving Average and Super Trend Tracking Stop Loss Strategy

- Linear Regression Channel Strategy

- Combination Trading Strategy Based on Dual EMA and Bandpass Filter

- Trend Tracking Trailing Stop Strategy

- Key Reversal Backtest Strategy

- Quantitative Trading Strategy Based on Moving Average

- Trend Following Strategy Based on Price Action and Volume

- Ichimoku Kinko Hyo Breakout Strategy

- ADX Momentum Trend Strategy

- Combination Strategy of 123 Reversal and Pivot Point

- Moving Average and Stochastic RSI Combination Trading Strategy

- Dynamic Trend Tracking Reversal Strategy

- Daily DCA Strategy with Touching EMAs

- Trend Strength Confirm Bars Strategy

- Super Trend Dual Moving Average Strategy