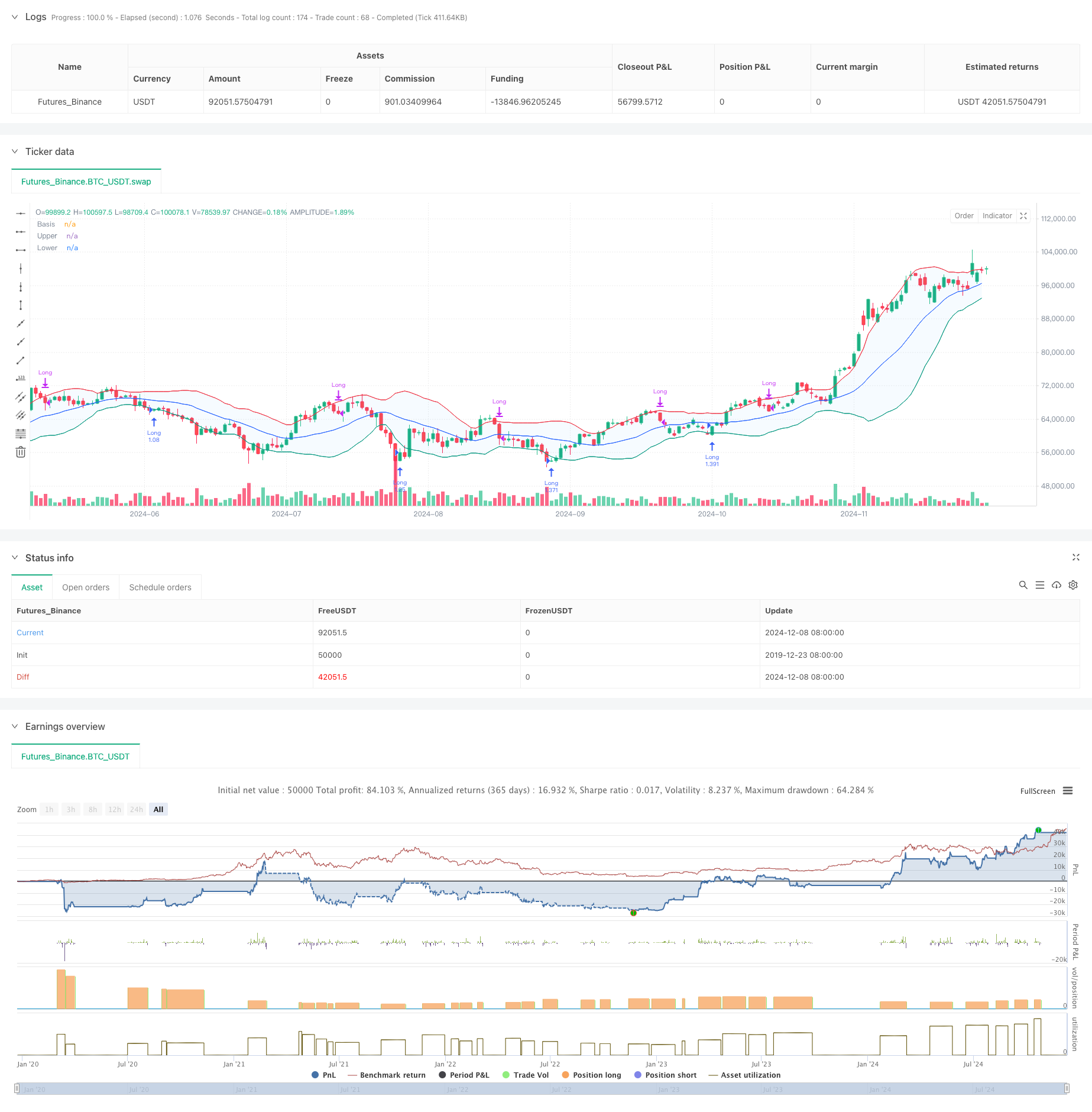

Descripción general

La estrategia es un sistema de negociación inteligente basado en el indicador de la banda de Brin y el ATR, combinado con un mecanismo de stop-loss de varios niveles. La estrategia se ejecuta principalmente mediante la identificación de señales de reversión cerca de la banda de Brin, y administra el riesgo utilizando un método de stop-loss de seguimiento dinámico. El sistema está diseñado para alcanzar un objetivo de ganancia del 20% y un punto de parada del 12%, al tiempo que realiza un stop-loss de seguimiento dinámico en combinación con el indicador de ATR, lo que permite dar suficiente espacio a la tendencia mientras protege las ganancias.

Principio de estrategia

La lógica central de la estrategia incluye las siguientes partes clave:

- Condiciones de ingreso: Se requiere que el aro rojo toque la banda de Brin y que aparezca el aro verde después de la baja, una forma que generalmente indica una posible señal de reversión.

- Opción de promedio móvil: soporta varios tipos de promedio móvil (SMA, EMA, SMMA, WMA, VWMA), usa 20 ciclos SMA por defecto.

- Parámetros de la banda de Brin: Utiliza 1.5 veces la diferencia estándar como ancho de banda, una configuración más conservadora que el tradicional 2 veces la diferencia estándar.

- El mecanismo de suspensión: Establecer un objetivo de ganancias iniciales del 20%.

- Mecanismo de detención de pérdidas: establezca un límite de pérdidas fijo del 12% para proteger los fondos.

- La pérdida de seguimiento dinámico:

- Activar el ATR de seguimiento de stop loss cuando el precio alcance el nivel de ganancias objetivo

- El ATR se detiene en el seguimiento dinámico después de tocar la cinta de Brin

- Ajuste dinámico de seguimiento de la distancia de parada con ATR multiplicado

Ventajas estratégicas

- Control de riesgos en varios niveles:

- Capital fijo para la protección del nivel de pérdida fija

- Dinámica de seguimiento de pérdidas para bloquear ganancias

- El deterioro dinámico provocado por la cinta de Brin en la vía proporciona protección adicional

- La opción de media móvil flexible permite que las estrategias se adapten a diferentes entornos de mercado

- El stop tracking dinámico combinado con el indicador ATR se puede ajustar automáticamente según la volatilidad del mercado para evitar salidas prematuras

- Las señales de entrada se combinan con la morfología de los precios y los indicadores técnicos para mejorar la fiabilidad de la señal

- Apoyo a la gestión de posiciones y configuración de costos de transacción, más cerca del entorno de transacción real

Riesgo estratégico

- Los mercados rápidos y convulsivos pueden provocar transacciones frecuentes y aumentar los costos de las transacciones.

- El Stop Loss fijo del 12% puede ser demasiado pequeño en algunos mercados altamente volátiles

- Las señales de las bandas de Bryn pueden generar falsas señales en mercados de tendencia

- El deterioro de la trazabilidad ATR puede causar una mayor retirada en caso de una gran volatilidad Medidas de mitigación:

- Se recomienda su uso en períodos de tiempo más largos (de 30 minutos a 1 hora)

- Se puede ajustar la proporción de pérdidas según las características de cada variedad

- Considere agregar filtros de tendencia y reducir las señales falsas

- Ajuste dinámico del ATR para adaptarse a las diferentes condiciones del mercado

Dirección de optimización de la estrategia

- Optimización para el ingreso:

- Añadir mecanismo de confirmación del volumen de transacciones

- Agrega una señal de filtro de la intensidad de la tendencia

- Considerar la inclusión de indicadores de movilidad para el juicio auxiliar

- Optimización de pérdidas:

- Cambiar el stop fijo por el stop dinámico basado en el ATR

- Desarrollo de algoritmos de parada de pérdidas adaptativos

- Ajuste de la distancia de pérdida en función de la fluctuación de la tasa

- Optimización de la media móvil:

- Prueba de diferentes combinaciones de ciclos

- El estudio del ciclo de adaptación

- Considere usar el comportamiento del precio en lugar de la media móvil

- Optimización de la gestión de posiciones:

- Desarrollo de un sistema de gestión de posiciones basado en la volatilidad

- Implementar un mecanismo para construir y reducir posiciones en lotes

- Incorporar el control de las aberturas de riesgo

Resumir

La estrategia construye un sistema de negociación multicapa a través de la banda de Brin y el indicador ATR, y utiliza un método de gestión dinámica en los aspectos de entrada, parada de pérdidas y cierre de ganancias. La ventaja de la estrategia reside en su sistema de control de riesgos completo y su capacidad de adaptación a la fluctuación del mercado.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Demo GPT - Bollinger Bands Strategy with Tightened Trailing Stops", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=100, commission_value=0.1, slippage=3)

// Input settings

length = input.int(20, minval=1)

maType = input.string("SMA", "Basis MA Type", options=["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"])

src = input(close, title="Source")

mult = 1.5 // Standard deviation multiplier set to 1.5

offset = input.int(0, "Offset", minval=-500, maxval=500)

atrMultiplier = input.float(1.0, title="ATR Multiplier for Trailing Stop", minval=0.1) // ATR multiplier for trailing stop

// Time range filters

start_date = input(timestamp("2018-01-01 00:00"), title="Start Date")

end_date = input(timestamp("2069-12-31 23:59"), title="End Date")

in_date_range = true

// Moving average function

ma(source, length, _type) =>

switch _type

"SMA" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

// Calculate Bollinger Bands

basis = ma(src, length, maType)

dev = mult * ta.stdev(src, length)

upper = basis + dev

lower = basis - dev

// ATR Calculation

atr = ta.atr(length) // Use ATR for trailing stop adjustments

// Plotting

plot(basis, "Basis", color=#2962FF, offset=offset)

p1 = plot(upper, "Upper", color=#F23645, offset=offset)

p2 = plot(lower, "Lower", color=#089981, offset=offset)

fill(p1, p2, title="Background", color=color.rgb(33, 150, 243, 95))

// Candle color detection

isGreen = close > open

isRed = close < open

// Flags for entry and exit conditions

var bool redTouchedLower = false

var float targetPrice = na

var float stopLossPrice = na

var float trailingStopPrice = na

if in_date_range

// Entry Logic: First green candle after a red candle touches the lower band

if close < lower and isRed

redTouchedLower := true

if redTouchedLower and isGreen

strategy.entry("Long", strategy.long)

targetPrice := close * 1.2 // Set the target price to 20% above the entry price

stopLossPrice := close * 0.88 // Set the stop loss to 12% below the entry price

trailingStopPrice := na // Reset trailing stop on entry

redTouchedLower := false

// Exit Logic: Trailing stop after 20% price increase

if strategy.position_size > 0 and not na(targetPrice) and close >= targetPrice

if na(trailingStopPrice)

trailingStopPrice := close - atr * atrMultiplier // Initialize trailing stop using ATR

trailingStopPrice := math.max(trailingStopPrice, close - atr * atrMultiplier) // Tighten dynamically based on ATR

// Exit if the price falls below the trailing stop after 20% increase

if strategy.position_size > 0 and not na(trailingStopPrice) and close < trailingStopPrice

strategy.close("Long", comment="Trailing Stop After 20% Increase")

targetPrice := na // Reset the target price

stopLossPrice := na // Reset the stop loss price

trailingStopPrice := na // Reset trailing stop

// Stop Loss: Exit if the price drops 12% below the entry price

if strategy.position_size > 0 and not na(stopLossPrice) and close <= stopLossPrice

strategy.close("Long", comment="Stop Loss Triggered")

targetPrice := na // Reset the target price

stopLossPrice := na // Reset the stop loss price

trailingStopPrice := na // Reset trailing stop

// Trailing Stop: Activate after touching the upper band

if strategy.position_size > 0 and close >= upper and isGreen

if na(trailingStopPrice)

trailingStopPrice := close - atr * atrMultiplier // Initialize trailing stop using ATR

trailingStopPrice := math.max(trailingStopPrice, close - atr * atrMultiplier) // Tighten dynamically based on ATR

// Exit if the price falls below the trailing stop

if strategy.position_size > 0 and not na(trailingStopPrice) and close < trailingStopPrice

strategy.close("Long", comment="Trailing Stop Triggered")

trailingStopPrice := na // Reset trailing stop

targetPrice := na // Reset the target price

stopLossPrice := na // Reset the stop loss price