Strategi Mengikuti Tren Bollinger Band Adaptif Dua Arah

Tanggal Pembuatan:

2024-02-04 15:30:46

Akhirnya memodifikasi:

2024-02-04 15:30:46

menyalin:

4

Jumlah klik:

623

1

fokus pada

1628

Pengikut

Ringkasan

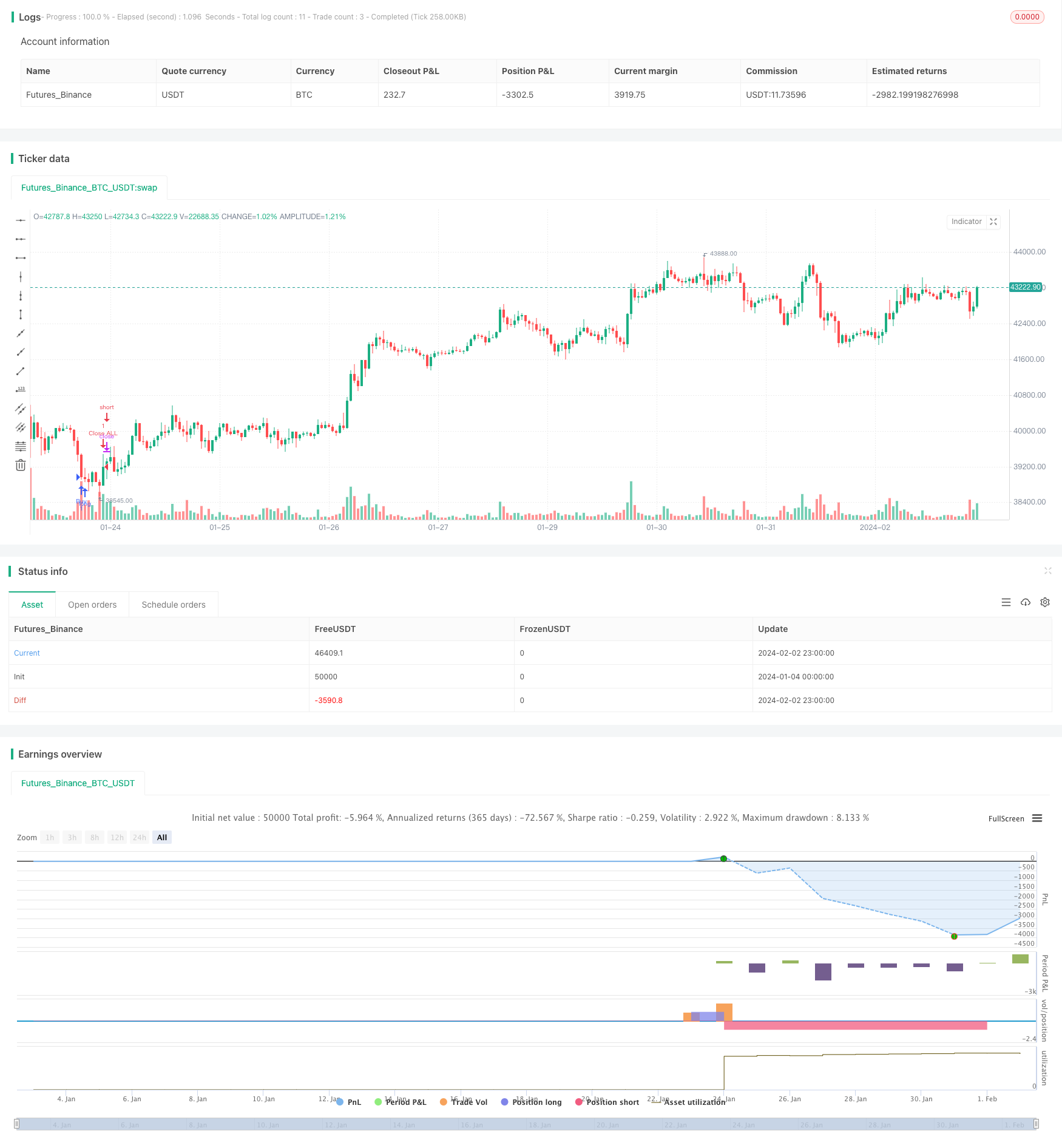

Strategi ini menggunakan indikator BRI bidirectional untuk mengidentifikasi arah tren, dan dalam kombinasi dengan harga pasar untuk melakukan stop loss tracking, untuk mencapai efisiensi tinggi dalam perdagangan trend tracking.

Prinsip Strategi

- Brin tengah, atas dan bawah rel berdasarkan siklus tertentu

- Jika harga naik, Anda akan melakukan pelacakan lebih banyak, dan jika harga turun, Anda akan melakukan pelacakan kosong.

- Masuk cepat dengan harga pasar

- Setting Stop Loss Posisi, Stop Stop Posisi untuk Manajemen Posisi

Analisis Keunggulan

- Adaptasi terhadap indikator BRI, sensitif terhadap fluktuasi pasar, dan dapat dengan cepat menilai perubahan tren

- Menggunakan harga pasar untuk cepat masuk ke lapangan, mengurangi risiko slippage

- Stop loss otomatis, kontrol risiko ketat, kunci keuntungan

Analisis risiko

- Blinking sendiri memiliki keterbelakangan dan tidak dapat sepenuhnya menghindari terobosan palsu.

- Harga pasar tidak bisa dikendalikan

- Stop loss dan stop loss harus diatur dengan baik

Arah optimasi

- Menyesuaikan parameter Brin Belt untuk mengoptimalkan sensitivitas penilaian tren

- Menambahkan penyaringan untuk indikator seperti volume transaksi atau MACD

- Optimalkan pengaturan stop loss dan stop loss

Meringkaskan

Strategi ini memanfaatkan sepenuhnya keunggulan Bollinger Bands untuk menentukan arah tren dan perubahan, menggabungkan dengan daftar harga pasar yang keluar cepat untuk melakukan pelacakan dua arah, dengan asumsi pengendalian risiko, untuk mendapatkan keuntungan tambahan. Dengan mengoptimalkan parameter Bollinger Bands lebih lanjut, menambahkan indikator penyaringan tambahan, menyesuaikan logika stop loss, dan lain-lain, kinerja strategi yang lebih baik dapat diperoleh.

Kode Sumber Strategi

/*backtest

start: 2024-01-04 00:00:00

end: 2024-02-03 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © CryptoRox

//@version=4

//Paste the line below in your alerts to run the built-in commands.

//{{strategy.order.alert_message}}

strategy("Automated - Fibs with Market orders", "Strategy", true)

//Settings

testing = input(false, "Live")

//Use epochconverter or something similar to get the current timestamp.

starttime = input(1600976975, "Start Timestamp") * 1000

//Wait XX seconds from that timestamp before the strategy starts looking for an entry.

seconds = input(60, "Start Delay") * 1000

testPeriod = true

leverage = input(1, "Leverage")

tp = input(1.0, "Take Profit %") / leverage

dca = input(-1.0, "DCA when < %") / leverage *-1

fibEntry = input("1", "Entry Level", options=["1", "2", "3", "4", "5", "6", "7", "8", "9", "10"])

//Strategy Calls

equity = strategy.equity

avg = strategy.position_avg_price

symbol = syminfo.tickerid

openTrades = strategy.opentrades

closedTrades = strategy.closedtrades

size = strategy.position_size

//Fibs

lentt = input(60, "Pivot Length")

h = highest(lentt)

h1 = dev(h, lentt) ? na : h

hpivot = fixnan(h1)

l = lowest(lentt)

l1 = dev(l, lentt) ? na : l

lpivot = fixnan(l1)

z = 400

p_offset= 2

transp = 60

a=(lowest(z)+highest(z))/2

b=lowest(z)

c=highest(z)

fib0 = (((hpivot - lpivot)) + lpivot)

fib1 = (((hpivot - lpivot)*.21) + lpivot)

fib2 = (((hpivot - lpivot)*.3) + lpivot)

fib3 = (((hpivot - lpivot)*.5) + lpivot)

fib4 = (((hpivot - lpivot)*.62) + lpivot)

fib5 = (((hpivot - lpivot)*.7) + lpivot)

fib6 = (((hpivot - lpivot)* 1.00) + lpivot)

fib7 = (((hpivot - lpivot)* 1.27) + lpivot)

fib8 = (((hpivot - lpivot)* 2) + lpivot)

fib9 = (((hpivot - lpivot)* -.27) + lpivot)

fib10 = (((hpivot - lpivot)* -1) + lpivot)

notna = nz(fib10[60])

entry = 0.0

if fibEntry == "1"

entry := fib10

if fibEntry == "2"

entry := fib9

if fibEntry == "3"

entry := fib0

if fibEntry == "4"

entry := fib1

if fibEntry == "5"

entry := fib2

if fibEntry == "6"

entry := fib3

if fibEntry == "7"

entry := fib4

if fibEntry == "8"

entry := fib5

if fibEntry == "9"

entry := fib6

if fibEntry == "10"

entry := fib7

profit = avg+avg*(tp/100)

pause = 0

pause := nz(pause[1])

paused = time < pause

fill = 0.0

fill := nz(fill[1])

count = 0.0

count := nz(fill[1])

filled = count > 0 ? entry > fill-fill/100*dca : 0

signal = testPeriod and notna and not paused and not filled ? 1 : 0

neworder = crossover(signal, signal[1])

moveorder = entry != entry[1] and signal and not neworder ? true : false

cancelorder = crossunder(signal, signal[1]) and not paused

filledorder = crossunder(low[1], entry[1]) and signal[1]

last_profit = 0.0

last_profit := nz(last_profit[1])

// if neworder and signal

// strategy.order("New", 1, 0.0001, alert_message='New Order|e=binancefuturestestnet s=btcusdt b=long q=0.0011 fp=' + tostring(entry))

// if moveorder

// strategy.order("Move", 1, 0.0001, alert_message='Move Order|e=binancefuturestestnet s=btcusdt b=long c=order|e=binancefuturestestnet s=btcusdt b=long q=0.0011 fp=' + tostring(entry))

if filledorder and size < 1

fill := entry

count := count+1

pause := time + 60000

p = close+close*(tp/100)

strategy.entry("Buy", 1, 1, alert_message='Long|e=binancefuturestestnet s=btcusdt b=long q=0.0011 t=market')

if filledorder and size >= 1

fill := entry

count := count+1

pause := time + 60000

strategy.entry("Buy", 1, 1, alert_message='Long|e=binancefuturestestnet s=btcusdt b=long q=0.0011 t=market')

// if cancelorder and not filledorder

// pause := time + 60000

// strategy.order("Cancel", 1, 0.0001, alert_message='Cancel Order|e=binancefuturestestnet s=btcusdt b=long c=order')

if filledorder

last_profit := profit

closeit = crossover(high, profit) and size >= 1

if closeit

strategy.entry("Close ALL", 0, 0, alert_message='Close Long|e=binancefuturestestnet s=btcusdt b=long c=position t=market')

count := 0

fill := 0.0

last_profit := 0.0

//Plots

// bottom = signal ? color.green : filled ? color.red : color.white

// plot(entry, "Entry", bottom)