1

フォロー

1628

フォロワー

概要

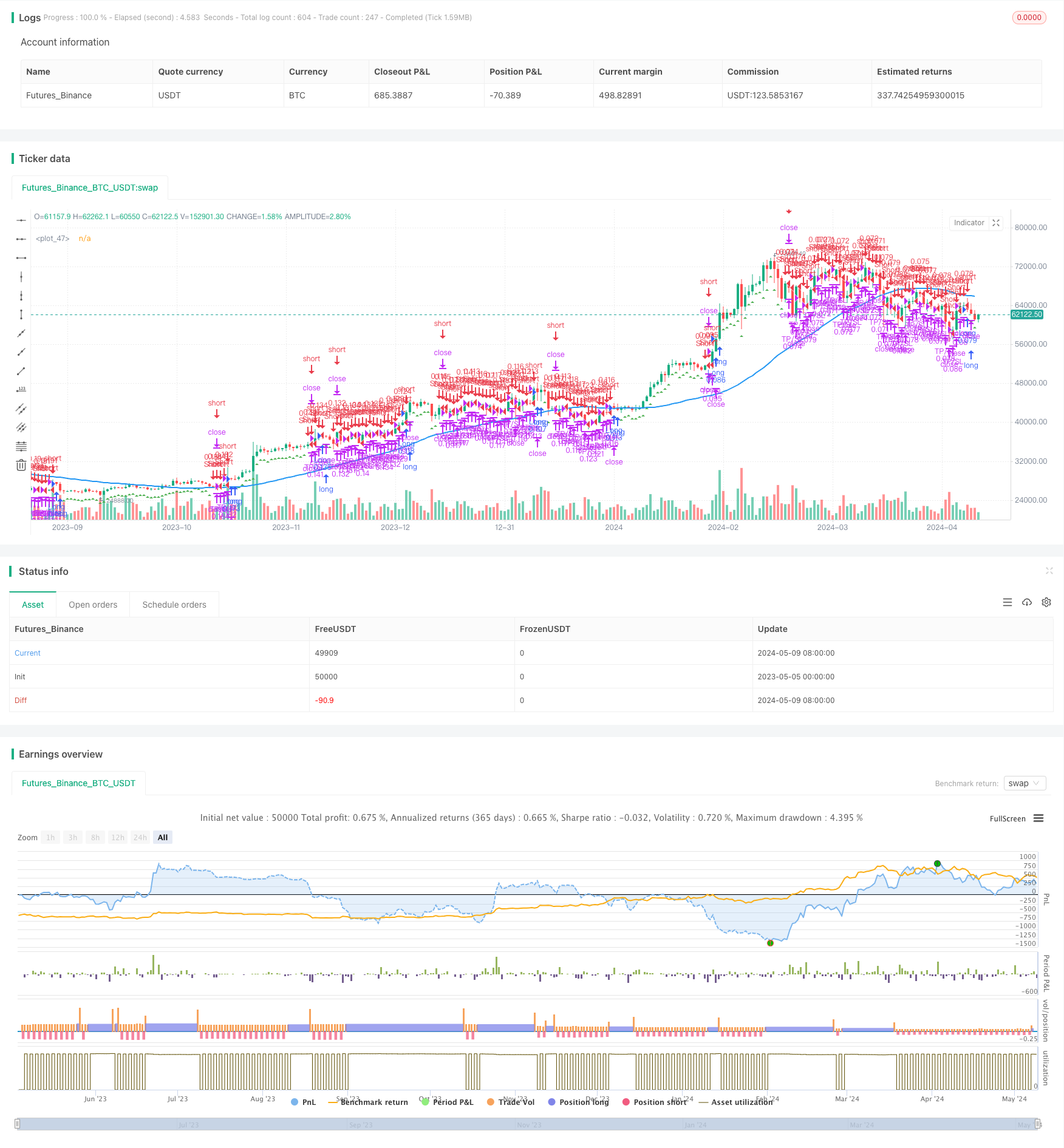

この戦略は,1時間のチャート上のトレンド偏差,15分チャート上のMACD指標のクロスシグナル,そして5分チャート上の急速な波動率とギャップに基づいてエントリーポイントを決定します.この戦略は,異なる時間周期で複数の指標を使用することにより,市場の長期の傾向,中期の動き,短期の変動を捉え,より正確な市場予測を実現することを目的としています.

戦略原則

この戦略の核心原則は,異なる時間周期の技術指標を組み合わせて,市場をより全面的に分析することです.具体的には:

- 1時間のグラフで,閉盤価格と50周期移動平均を比較して長期トレンド偏差を決定する.

- 15分グラフ上では,MACD指標の交差信号によって中期多空運動量を確認する.

- 5分間のグラフで,急速な波動率 (平均リアルレンジ指標を用いて計算) と価格のギャップを観察することで潜在的なエントリーポイントを見つけます.

この3つの異なる時間周期のシグナルを組み合わせることで,戦略は市場の全体的な動きをよりよく把握し,短期的な波動を利用してエントリーポイントを最適化することで,取引の正確性と収益性の可能性を高めます.

戦略的優位性

- マルチタイムサイクル分析:この戦略は,異なるタイムサイクルで複数の指標を使用することにより,市場をより全面的に分析し,異なるレベルのトレンドと動力の信号を捉えます.

- トレンド確認:この戦略は,1時間チャートの閉盤価格と移動平均を比較することで,長期のトレンド偏差を特定し,取引決定に強力なサポートを提供します.

- 動態信号:15分間のグラフでMACD指標を使用し,市場の多空動態の変化をタイムリーに捉え,トレンド確認のためのさらなる根拠を提供します.

- 精確なエントリー:この戦略は,5分間のグラフの急速な波動と価格のギャップを観察することで,より最適のエントリーポイントを見つけ,取引の効率性を向上させます.

- リスクコントロール:この戦略は,利害を考慮したストップ・ストップ・損失設定を使用し,利益を追求しながら潜在的リスクを制御することができます.

戦略リスク

- パラメータ最適化:この戦略のパフォーマンスは,MACD指標のパラメータ設定,移動平均周期などのパラメータ選択に敏感である可能性があり,十分な反測と最適化が必要である.

- 市場の変動: 市場の激しい変動やトレンドの変化の場合には,この戦略の有効性が影響を受ける可能性があります.

- 杆リスク:この戦略は杆要因を考慮しているが,過高な杆は依然として大きな損失を引き起こす可能性がある.杆倍数を慎重に選択し,リスクを厳密に管理する必要があります.

戦略最適化の方向性

- 動的パラメータ最適化: 機械学習または最適化アルゴリズムを使用することを検討し,市場状況に応じて動的に戦略パラメータを調整し,異なる市場環境に対応します.

- 多空のポジション管理:より高度なポジション管理戦略を導入できます.例えば,市場の変動やトレンドの強さに応じてポジションサイズを動的に調整することで,リスクをよりよく制御し,利益を最適化できます.

- 他の指標を追加する: 戦略の安定性と適応性をさらに向上させるために,他の技術指標や基本的要素,例えば相対的な強さ指数 (RSI),市場情緒指標などの導入を検討する.

要約する

この戦略は,1時間チャートのトレンド偏差,15分チャートのMACD動向信号,および5分チャートの急速な波動率と価格ギャップを組み合わせて,複数の時間周期,複数の指標の取引システムを構築しています.この方法は,市場をより全面的に分析し,さまざまなレベルのトレンドと機会を捉え,リスクを制御することができます.しかし,戦略のパフォーマンスは,パラメータ選択に敏感であり,特定の市場の激しい波動で課題に直面することがあります.

ストラテジーソースコード

/*backtest

start: 2023-05-05 00:00:00

end: 2024-05-10 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("H1 Bias + M15 MSS + M5 FVG", overlay=true, initial_capital=1000, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// H1 Bias

h1_bias = request.security(syminfo.tickerid, "60", close)

h1_ma = ta.sma(h1_bias, 50)

// M15 MSS

[m15_macd_line, m15_macd_signal, _] = ta.macd(request.security(syminfo.tickerid, "15", close), 12, 26, 9)

// M5 FVG Entry

m5_volatility = ta.atr(14)

// Entry conditions for long and short positions

long_condition = m15_macd_line > m15_macd_signal and m5_volatility > 0.001

short_condition = m15_macd_line < m15_macd_signal and m5_volatility > 0.001

// Exit conditions

exit_long_condition = m15_macd_line < m15_macd_signal

exit_short_condition = m15_macd_line > m15_macd_signal

// Strategy

if (long_condition)

strategy.entry("Long", strategy.long)

if (short_condition)

strategy.entry("Short", strategy.short)

if (exit_long_condition)

strategy.close("Long")

if (exit_short_condition)

strategy.close("Short")

// Take-Profit and Stop-Loss settings considering leverage

leverage = 10.0 // Leverage as a float

tp_percentage = 15.0 // TP percentage without leverage as a float

sl_percentage = 5.0 // SL percentage without leverage as a float

tp_level = strategy.position_avg_price * (1.0 + (tp_percentage / 100.0 / leverage)) // TP considering leverage as a float

sl_level = strategy.position_avg_price * (1.0 - (sl_percentage / 100.0 / leverage)) // SL considering leverage as a float

strategy.exit("TP/SL", "Long", limit=tp_level, stop=sl_level)

strategy.exit("TP/SL", "Short", limit=tp_level, stop=sl_level)

// Plotting

plot(h1_ma, color=color.blue, linewidth=2)

plotshape(long_condition, style=shape.triangleup, location=location.belowbar, color=color.green, size=size.small)

plotshape(short_condition, style=shape.triangledown, location=location.abovebar, color=color.red, size=size.small)