1

フォロー

1628

フォロワー

概要

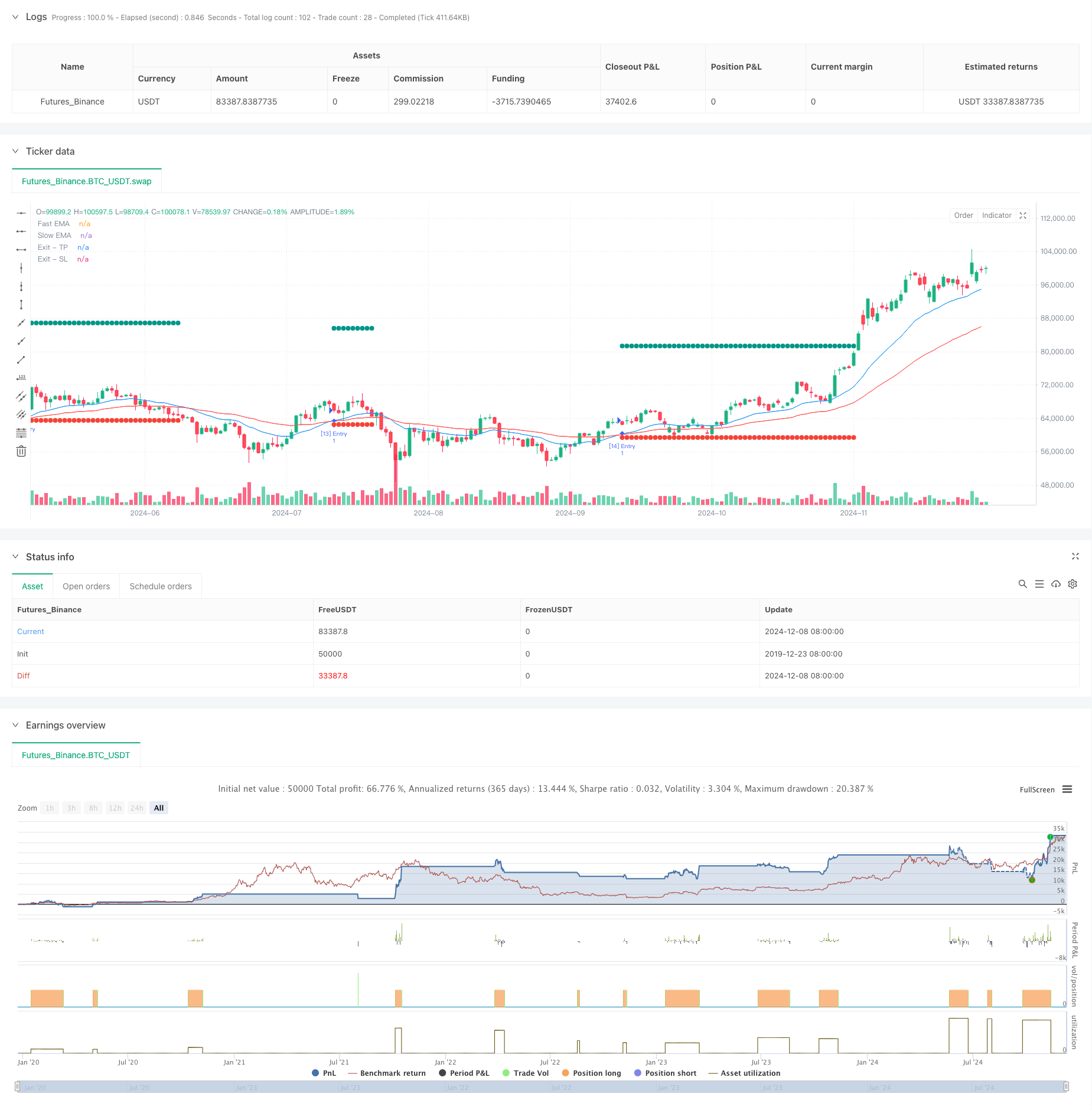

これは,双均線交差信号に基づく定量取引戦略で,急速指数移動平均 ((EMA) と遅速指数移動平均 ((EMA) の交差によって市場動向を判断し,動的ストップ・ロズ・コントロールと組み合わせてリスクを管理する. 戦略は,パーセントポジション管理を採用し,デフォルトで10%の資金を使用して取引し,動的ストップ・ロズ・価格を設定することで利益を保護し,リスクを管理する.

戦略原則

戦略の核心的な論理は,20周期と50周期の指数移動平均 (EMA) の交差を監視することによってトレンドの変化を認識することです. 急速なEMAが上昇して遅いEMAを横断すると,システムは複数の信号を生成します. ポジションを開設したたびに,システムは,入場価格 (入場価格の1.3倍) と止損価格 (入場価格の0.95倍) に基づいて自動でストップ価格を設定します. このダイナミックなストップ損失の設計は,異なる市場環境に適応して戦略の柔軟性を高めます.

戦略的優位性

- 信号の安定性 - 単純な移動平均 (SMA) ではなくEMAを使用し,価格変化により迅速に反応し,同時に一部の市場のノイズをフィルターすることができます.

- リスク管理の改善 - ダイナミックなストップ・ストップ・メカニズムを使用し,ストップ・ストップの価格は入場価格の変化に合わせて調整されます.

- 資金管理は合理的 - 固定比率のポジション管理を使用し,全ポジション操作の高リスクを回避する.

- 高い自動化度 - 信号生成からポジション管理まで自動化され,人間の干渉が軽減されています.

- 適応性 - 戦略は異なる市場環境に適応し,パラメータは実際の状況に応じて柔軟に調整できます.

戦略リスク

- 平均線遅れ - EMAは反応が早いが,まだ一定の遅れがあるため,入場タイミングがわずかに遅れる可能性がある.

- 振動市場には適用されない - 横軸の振動で,頻繁に偽の突破信号が生じる可能性があります.

- 固定倍数ストップ・ロス - 固定倍数でストップ・ロスを設定し,すべての市場環境には適さない場合があります.

- 撤回リスク - 変動が激しい市場では,5%のストップは大きな波動に対応するには不十分である.

戦略最適化の方向性

- 波動率指標の導入 - 市場波動に適したストップ・ストップ・ロスの倍数を動的に調整するためにATR指標の追加が推奨されている.

- トレンド確認を増やす - RSI,MACDなどの指標を組み合わせて取引信号をフィルターして勝率を向上させる.

- ポジション管理の最適化 - 市場の変動率の動向に応じてポジションのサイズを調整して,より精密なリスク管理を実現する.

- タイムフィルターを追加 - 取引時間ウィンドウの制限を増やすことを検討し,波動が大きい時期を避ける.

- 停止の仕組みの改善 - 移動停止を実現し,状況が良くなればより多くの利益を得ることができます.

要約する

これは,合理的で論理的に明確なトレンド追跡戦略を設計し,双均線交差でトレンドをキャプチャし,ダイナミックなストップ・ロスを使用してリスクを管理する戦略である.戦略の優点は,操作ルールは明確であり,リスクは制御可能であり,中長期の取引システムの基本的枠組みに適合するものである.より多くのフィルタリング条件を追加し,ストップ・ロスを最適化するメカニズムを最適化することにより,この戦略には大きな最適化余地がある.

ストラテジーソースコード

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-09 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Pineify

//======================================================================//

// ____ _ _ __ //

// | _ \(_)_ __ ___(_)/ _|_ _ //

// | |_) | | '_ \ / _ \ | |_| | | | //

// | __/| | | | | __/ | _| |_| | //

// |_| |_|_| |_|\___|_|_| \__, | //

// |___/ //

//======================================================================//

//@version=5

strategy(title="TQQQ EMA Strategy", overlay=true)

//#region —————————————————————————————————————————————————— Common Dependence

p_comm_time_range_to_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int start_unix_time = na

int end_unix_time = na

int start_time_hour = na

int start_time_minute = na

int end_time_hour = na

int end_time_minute = na

if str.length(time_range) == 11

// Format: hh:mm-hh:mm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 3, 5)))

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 6, 8)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 9, 11)))

else if str.length(time_range) == 9

// Format: hhmm-hhmm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 2, 4)))

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 5, 7)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 7, 9)))

start_unix_time := timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), start_time_hour, start_time_minute, 0)

end_unix_time := timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), end_time_hour, end_time_minute, 0)

[start_unix_time, end_unix_time]

p_comm_time_range_to_start_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int start_time_hour = na

int start_time_minute = na

if str.length(time_range) == 11

// Format: hh:mm-hh:mm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 3, 5)))

else if str.length(time_range) == 9

// Format: hhmm-hhmm

start_time_hour := math.floor(str.tonumber(str.substring(time_range, 0, 2)))

start_time_minute := math.floor(str.tonumber(str.substring(time_range, 2, 4)))

timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), start_time_hour, start_time_minute, 0)

p_comm_time_range_to_end_unix_time(string time_range, int date_time = time, string timezone = syminfo.timezone) =>

int end_time_hour = na

int end_time_minute = na

if str.length(time_range) == 11

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 6, 8)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 9, 11)))

else if str.length(time_range) == 9

end_time_hour := math.floor(str.tonumber(str.substring(time_range, 5, 7)))

end_time_minute := math.floor(str.tonumber(str.substring(time_range, 7, 9)))

timestamp(timezone, year(date_time, timezone), month(date_time, timezone), dayofmonth(date_time, timezone), end_time_hour, end_time_minute, 0)

p_comm_timeframe_to_seconds(simple string tf) =>

float seconds = 0

tf_lower = str.lower(tf)

value = str.tonumber(str.substring(tf_lower, 0, str.length(tf_lower) - 1))

if str.endswith(tf_lower, 's')

seconds := value

else if str.endswith(tf_lower, 'd')

seconds := value * 86400

else if str.endswith(tf_lower, 'w')

seconds := value * 604800

else if str.endswith(tf_lower, 'm')

seconds := value * 2592000

else

seconds := str.tonumber(tf_lower) * 60

seconds

p_custom_sources() =>

[open, high, low, close, volume]

//#endregion —————————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Ta Dependence

//#endregion —————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Constants

// Input Groups

string P_GP_1 = ""

//#endregion —————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Inputs

// Default

int p_inp_1 = input.int(defval=20, title="Fast EMA Length", group=P_GP_1)

int p_inp_2 = input.int(defval=50, title="Slow EMA Length", group=P_GP_1)

float p_inp_3 = input.float(defval=1.3, title="Take Profit Price Multiplier", group=P_GP_1, step=0.01)

float p_inp_4 = input.float(defval=0.95, title="Stop Loss Price Multiplier", group=P_GP_1, step=0.01)

//#endregion ———————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Price Data

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Indicators

p_ind_1 = ta.ema(close, p_inp_1) // Fast EMA

p_ind_2 = ta.ema(close, p_inp_2) // Slow EMA

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Conditions

p_cond_1 = (ta.crossover(p_ind_1, p_ind_2))

//#endregion ———————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Strategy

// Strategy Order Variables

string p_st_name_1 = "Entry"

string p_st_name_2 = "Exit"

var float p_st_name_2_tp = na

var bool p_st_name_2_tp_can_drawing = true

var float p_st_name_2_sl = na

var bool p_st_name_2_sl_can_drawing = true

// Strategy Global

open_trades_number = strategy.opentrades

pre_bar_open_trades_number = na(open_trades_number[1]) ? 0 : open_trades_number[1]

var p_entry_order_id = 1

p_can_place_entry_order() =>

strategy.equity > 0

get_entry_id_name(int current_order_id, string name) =>

"[" + str.tostring(current_order_id) + "] " + name

is_entry_order(string order_id, string name) =>

str.startswith(order_id, "[") and str.endswith(order_id, "] " + name)

get_open_trades_entry_ids() =>

int p_open_trades_count = strategy.opentrades

string[] p_entry_ids = array.new_string(0, "")

if p_open_trades_count > 0

for i = 0 to p_open_trades_count - 1

array.push(p_entry_ids, strategy.opentrades.entry_id(i))

p_entry_ids

// Entry (Entry)

if p_cond_1 and p_can_place_entry_order()

p_st_name_1_id = get_entry_id_name(p_entry_order_id, p_st_name_1)

p_entry_order_id := p_entry_order_id + 1

string entry_message = ""

strategy.entry(id=p_st_name_1_id, direction=strategy.long, alert_message=entry_message, comment=p_st_name_1_id)

// TP/SL Exit (Exit)

float p_st_name_2_limit = close * p_inp_3

if p_st_name_2_tp_can_drawing

p_st_name_2_tp_can_drawing := false

p_st_name_2_tp := p_st_name_2_limit

float p_st_name_2_stop = close * p_inp_4

if p_st_name_2_sl_can_drawing

p_st_name_2_sl_can_drawing := false

p_st_name_2_sl := p_st_name_2_stop

string p_st_name_2_alert_message = ""

strategy.exit(id=p_st_name_1_id + "_0", from_entry=p_st_name_1_id, qty_percent=100, limit=p_st_name_2_limit, stop=p_st_name_2_stop, comment_profit=p_st_name_2 + " - TP", comment_loss=p_st_name_2 + " - SL", alert_message=p_st_name_2_alert_message)

if high >= p_st_name_2_tp or (pre_bar_open_trades_number > 0 and open_trades_number == 0)

p_st_name_2_tp_can_drawing := true

p_st_name_2_sl_can_drawing := true

p_st_name_2_tp := na

p_st_name_2_sl := na

plot(p_st_name_2_tp, title="Exit - TP", color=color.rgb(0, 150, 136, 0), linewidth=1, style = plot.style_circles)

if low <= p_st_name_2_sl or (pre_bar_open_trades_number > 0 and open_trades_number == 0)

p_st_name_2_sl_can_drawing := true

p_st_name_2_tp_can_drawing := true

p_st_name_2_sl := na

p_st_name_2_tp := na

plot(p_st_name_2_sl, title="Exit - SL", color=color.rgb(244, 67, 54, 0), linewidth=1, style = plot.style_circles)

//#endregion —————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Indicator Plots

// Fast EMA

plot(p_ind_1, "Fast EMA", color.rgb(33, 150, 243, 0), 1)

// Slow EMA

plot(p_ind_2, "Slow EMA", color.rgb(255, 82, 82, 0), 1)

//#endregion ————————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Custom Plots

//#endregion —————————————————————————————————————————————————————————————

//#region —————————————————————————————————————————————————— Alert

//#endregion ——————————————————————————————————————————————————————