디지털 통화 선물 이중 EMA 전환점 전략 (교습)

저자:FMZ~리디아, 창작: 2022-11-09 09:44:38, 업데이트: 2023-09-20 10:25:53

이 기사에서는 간단한 트렌딩 전략을 설계하는 방법을 설명할 것이며, 전략 설계 수준에서만, 초보자가 간단한 전략을 설계하는 방법을 배우고 전략 실행 과정을 이해하는 데 도움이 될 것입니다. 전략의 성능은 전략 매개 변수와 크게 관련이 있습니다 (거의 모든 트렌딩 전략과 마찬가지로).

전략 설계

우리는 두 개의 EMA 지표를 사용한다. 두 EMA 평균이 전환점이 있을 때. 전환점은 긴 포지션을 열고 짧은 포지션을 열고 고정된 목표 이익 미연 포지션을 닫는 것을 위한 포지션을 열 (또는 오픈 포지션을 판매) 하는 신호로 사용됩니다. 댓글은 편리한 읽기 위해 전략 코드에 직접 작성됩니다. 전략 코드는 일반적으로 매우 짧고 초보자 학습에 적합합니다.

전략 코드

/*backtest

start: 2021-09-01 00:00:00

end: 2021-12-02 00:00:00

period: 1h

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"ETH_USDT"}]

*/

// The above /**/ is the default setting for backtesting, you can reset it on the backtesting page by using the relevant controls

var LONG = 1 // Markers for holding long positions, enum constant

var SHORT = -1 // Markers for holding short positions, enum constant

var IDLE = 0 // Markers without holding positions, enum constant

// Obtain positions in the specified direction. Positions is the position data, and direction is the position direction to be obtained

function getPosition(positions, direction) {

var ret = {Price : 0, Amount : 0, Type : ""} // Define a structure when no position is held

// Iterate through the positions and find the positions that match the direction

_.each(positions, function(pos) {

if (pos.Type == direction) {

ret = pos

}

})

// Return to found positions

return ret

}

// Cancel all makers of current trading pairs and contracts

function cancellAll() {

// Dead loop, keep detecting until break is triggered

while (true) {

// Obtain the makers' data of the current trading pair and contract, i.e. orders

var orders = _C(exchange.GetOrders)

if (orders.length == 0) {

// When orders is an empty array, i.e. orders.length == 0, break is executed to exit the while loop

break

} else {

// Iterate through all current makers and cancel them one by one

for (var i = 0 ; i < orders.length ; i++) {

// The function to cancel the specific order, cancel the order with ID: orders[i].Id

exchange.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

Sleep(500)

}

}

// The closing function, used for closing positions according to the trading function-tradeFunc and direction passed in

function cover(tradeFunc, direction) {

var mapDirection = {"closebuy": PD_LONG, "closesell": PD_SHORT}

var positions = _C(exchange.GetPosition) //Obtain the position data of the current trading pair and contract

var pos = getPosition(positions, mapDirection[direction]) // Find the position information in the specified closing position direction

// When the position is greater than 0 (the position can be closed only when there is a position)

if (pos.Amount > 0) {

// Cancel all possible makers

cancellAll()

// Set the trading direction

exchange.SetDirection(direction)

// Execute closing position trade functions

if (tradeFunc(-1, pos.Amount)) {

// Return to true if the order is placed

return true

} else {

// Return to false if the order is failed to place

return false

}

}

// Return to true if there is no position

return true

}

// Strategy main functions

function main() {

// For switching to OKEX V5 Demo

if (okexSimulate) {

exchange.IO("simulate", true) // Switch to OKEX V5 Demo for a test

Log("Switch to OKEX V5 Demo")

}

// Set the contract code, if ct is swap, set the current contract to be a perpetual contract

exchange.SetContractType(ct)

// Initialization status is open position

var state = IDLE

// The initialized position price is 0

var holdPrice = 0

// Timestamp for initialization comparison, used to compare whether the current K-Line BAR has changed

var preTime = 0

// Strategy main loop

while (true) {

// Obtain the K-line data for current trading pairs and contracts

var r = _C(exchange.GetRecords)

// Obtain the length of the K-line data, i.e. l

var l = r.length

// Judge the K-line length that l must be greater than the indicator period (if not, the indicator function cannot calculate valid indicator data), or it will be recycled

if (l < Math.max(ema1Period, ema2Period)) {

// Wait for 1,000 milliseconds, i.e. 1 second, to avoid rotating too fast

Sleep(1000)

// Ignore the code after the current if, and execute while loop again

continue

}

// Calculate ema indicator data

var ema1 = TA.EMA(r, ema1Period)

var ema2 = TA.EMA(r, ema2Period)

// Drawing chart

$.PlotRecords(r, 'K-Line') // Drawing the K-line chart

// When the last BAR timestamp changes, i.e. when a new K-line BAR is created

if(preTime !== r[l - 1].Time){

// The last update of the last BAR before the new BAR appears

$.PlotLine('ema1', ema1[l - 2], r[l - 2].Time)

$.PlotLine('ema2', ema2[l - 2], r[l - 2].Time)

// Draw the indicator line of the new BAR, i.e. the indicator data on the current last BAR

$.PlotLine('ema1', ema1[l - 1], r[l - 1].Time)

$.PlotLine('ema2', ema2[l - 1], r[l - 1].Time)

// Update the timestamp used for comparison

preTime = r[l - 1].Time

} else {

// When no new BARs are generated, only the indicator data of the last BAR on the chart is updated

$.PlotLine('ema1', ema1[l - 1], r[l - 1].Time)

$.PlotLine('ema2', ema2[l - 1], r[l - 1].Time)

}

// Conditions for opening long positions, turning points

var up = (ema1[l - 2] > ema1[l - 3] && ema1[l - 4] > ema1[l - 3]) && (ema2[l - 2] > ema2[l - 3] && ema2[l - 4] > ema2[l - 3])

// Conditions for opening short positions, turning points

var down = (ema1[l - 2] < ema1[l - 3] && ema1[l - 4] < ema1[l - 3]) && (ema2[l - 2] < ema2[l - 3] && ema2[l - 4] < ema2[l - 3])

// The condition of opening a long position is triggered and the current short position is held, or the condition of opening a long position is triggered and no position is held

if (up && (state == SHORT || state == IDLE)) {

// If you have a short position, close it first

if (state == SHORT && cover(exchange.Buy, "closesell")) {

// Mark open positions after closing them

state = IDLE

// The price of reset position is 0

holdPrice = 0

// Mark on the chart

$.PlotFlag(r[l - 1].Time, 'coverShort', 'CS')

}

// Open a long position after closing the position

exchange.SetDirection("buy")

if (exchange.Buy(-1, amount)) {

// Mark the current status

state = LONG

// Record the current price

holdPrice = r[l - 1].Close

$.PlotFlag(r[l - 1].Time, 'openLong', 'L')

}

} else if (down && (state == LONG || state == IDLE)) {

// The same as the judgment of up condition

if (state == LONG && cover(exchange.Sell, "closebuy")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverLong', 'CL')

}

exchange.SetDirection("sell")

if (exchange.Sell(-1, amount)) {

state = SHORT

holdPrice = r[l - 1].Close

$.PlotFlag(r[l - 1].Time, 'openShort', 'S')

}

}

// Stop profits

if (state == LONG && r[l - 1].Close - holdPrice > profitTarget && cover(exchange.Sell, "closebuy")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverLong', 'CL')

} else if (state == SHORT && holdPrice - r[l - 1].Close > profitTarget && cover(exchange.Buy, "closesell")) {

state = IDLE

holdPrice = 0

$.PlotFlag(r[l - 1].Time, 'coverShort', 'CS')

}

// Display time on the status bar

LogStatus(_D())

Sleep(500)

}

}

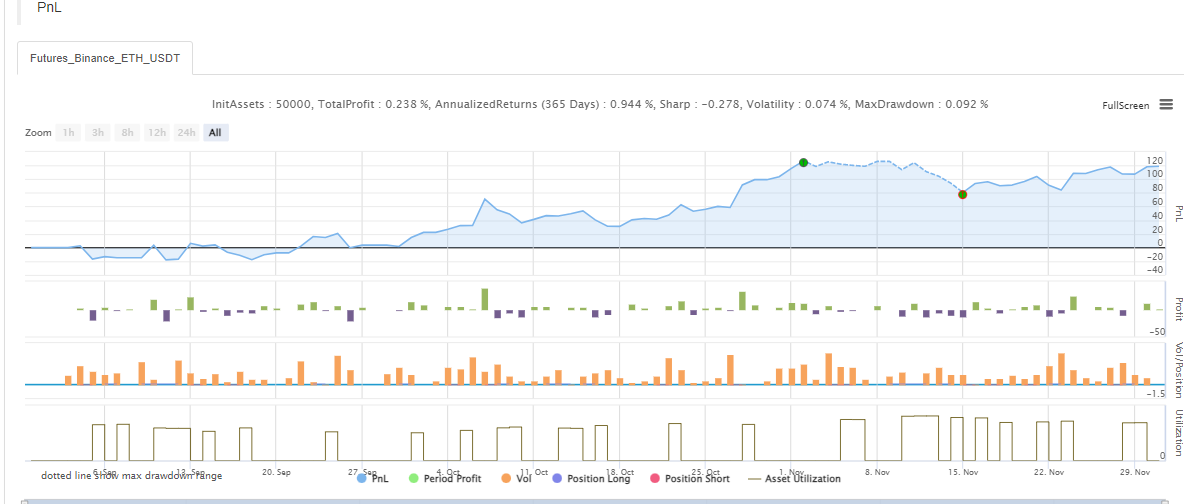

전략 소스 코드:https://www.fmz.com/strategy/333269

이 전략은 프로그램 설계 자습서에만 적용됩니다. 실제 봇에서는 사용하지 마세요.

관련 내용

- DEX 거래소의 양적 관행 (2) -- 하이퍼 액성 사용자 가이드

- DEX 거래소 정량화 연습 ((2)-- Hyperliquid 사용 지침

- DEX 거래소의 양적 관행 (1) -- dYdX v4 사용자 안내

- 암호화폐의 리드-래그 중재에 대한 소개 (3)

- DEX 거래소 정량화 연습 ((1)-- dYdX v4 사용 설명서

- 디지털 화폐의 리드-래그 스위트 소개 (3)

- 암호화폐의 리드-래그 중재에 대한 소개 (2)

- 디지털 화폐의 리드-래그 스위트 소개 (2)

- FMZ 플랫폼의 외부 신호 수신에 대한 논의: 전략 내 내장 Http 서비스와 함께 신호 수신에 대한 완전한 솔루션

- FMZ 플랫폼 외부 신호 수신에 대한 탐구: 전략 내장 HTTP 서비스 신호 수신의 전체 방안

- 암호화폐의 리드-래그 중재에 대한 소개 (1)

더 많은 내용

- [Binance 챔피언십] 바이낸스 배달 계약 전략 3 - 나비 헤지

- 양적 거래에서 서버의 사용

- 도커에서 전송된 http 요청 메시지를 얻는 솔루션

- 계약 헤지 전략으로 OKEX에서 자산 이동을 달성하는 것이 왜 실현 불가능한지에 대한 간략한 설명

- 미래에 대한 자세한 설명 역수 두 배 알고리즘 전략 참고

- 5일만에 80배를 벌고, 고주파 전략의 힘

- 메이커 스팟 및 선물 헤지 전략 설계에 대한 연구 및 예제

- SQLite로 FMZ의 양적 데이터베이스를 구축

- 전략 임대 코드 메타데이터를 통해 임대 전략에 다른 버전 데이터를 할당하는 방법

- 바이낸스 영구금융율의 금리 중재 (현재의 황소 시장 연간화 100%)

- 디지털 화폐 스팟에 대한 새로운 주식 전략 (교습)

- 60줄의 코드로 아이디어를 실현합니다. 계약 하단 낚시 전략

- 디지털 화폐 현금 다채용 이중 EMA 전략 (교습)

- FMZ 퀀트를 기반으로 하는 주문 동기화 관리 시스템의 설계 (2)

- 디지털 화폐 선물 다종 ATR 전략 (교습)

- 파인 언어를 사용하여 반 자동 거래 도구를 작성

- 리크스리퍼의 마법적 변화에서 고주파 전략 디자인을 탐구하십시오.

- 리크리퍼 전략 분석 (2)

- 유튜브 베테랑들의 "마법적인 이중 EMA 전략"

- 피셔 지표의 자바스크립트 언어 구현 및 FMZ에 대한 도화