Analisis dengan sabar strategi jalur purata bergerak tiga kali ganda yang mengandungi maklumat berharga dalam K-line

Gambaran keseluruhan

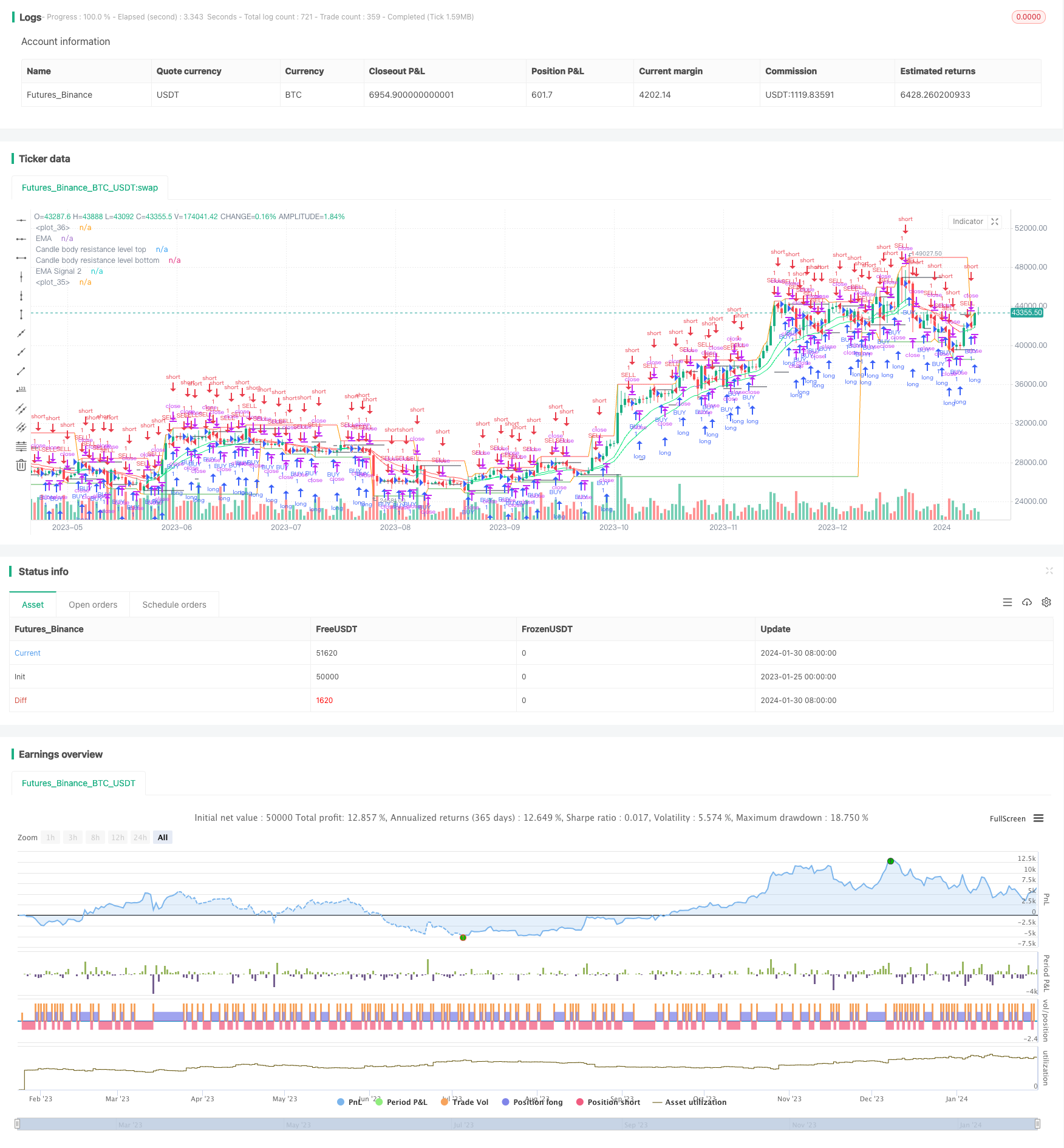

Strategi tiga jalur rata-rata menggunakan pelbagai petunjuk purata bergerak untuk menggali peraturan yang tersembunyi di dalam pergerakan harga dengan menganalisis garis K secara mendalam, untuk perdagangan risiko rendah.

Prinsip Strategi

Strategi ini meletakkan pelbagai EMA berdasarkan garis Brin, membina saluran harga, dan menemui peraturan pergerakan harga. Secara khusus:

- Menggunakan penunjuk BodyResistanceChannel untuk memetakan titik rintangan entiti K line.

- Menggunakan penunjuk Sokongan / rintangan untuk memetakan sokongan dan rintangan berbilang hari.

- Menggunakan sistem dua EMA untuk menentukan arah trend harga.

- Menggunakan Hull Average Line Indicator untuk meluruskan kurva harga.

Berdasarkan ini, ia boleh digunakan untuk mengenal pasti bentuk, menilai peluang untuk berbalik, dan membuat strategi perdagangan lelang.

Analisis kelebihan

Strategi ini mempunyai kelebihan berikut:

- Menggunakan pelbagai kumpulan EMA untuk membina saluran harga, anda dapat mengetahui dengan jelas ke mana pergerakan harga akan pergi.

- Penggunaan Hull Average Line Indicator dapat menilai harga peluruskan yang berkesan.

- Gabungan bentuk terbalik dan penunjuk saluran untuk mencapai perdagangan berisiko rendah dengan kebarangkalian tinggi.

- Membina sistem penunjuk pelbagai lapisan, isyarat perdagangan stabil dan boleh dipercayai.

Analisis risiko

Strategi ini juga mempunyai risiko:

- Penyelesaian yang disasarkan adalah dengan menggunakan hentian bergerak untuk mengurangkan kerugian tunggal.

- Kesalahan penghakiman bentuk terbalik berisiko menyebabkan isyarat yang salah. Penyelesaian yang disasarkan adalah untuk mengoptimumkan parameter dan meningkatkan ketepatan penghakiman bentuk.

- Risiko tidak sepadan parameter penunjuk yang menyebabkan penurunan kualiti isyarat perdagangan. Penyelesaian yang disasarkan adalah ujian pengoptimuman parameter pelbagai kombinasi.

Arah pengoptimuman

Strategi ini boleh dioptimumkan dengan cara:

- Mengoptimumkan kombinasi parameter kitaran EMA untuk menjadikan penunjuk lebih sesuai dengan ciri pasaran.

- Menyesuaikan kedudukan henti rugi untuk meminimumkan risiko kerugian tunggal dengan jaminan keuntungan.

- Tambah modul penyesuaian kedudukan dinamik berdasarkan kadar turun naik untuk mengawal risiko dengan berkesan.

- Dengan menggunakan teknologi pembelajaran mendalam, kami akan menggali lebih banyak peraturan harga dan meningkatkan kualiti isyarat.

ringkaskan

Strategi gelombang tiga garis rata mendalam menggali undang-undang turun naik harga, stabil dan cekap, bernilai penggunaan jangka panjang dan pengoptimuman berterusan. Pelaburan memerlukan akal dan kesabaran, langkah demi langkah adalah cara untuk menang.

/*backtest

start: 2023-01-25 00:00:00

end: 2024-01-31 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//╭╮╱╱╭╮╭╮╱╱╭╮

//┃╰╮╭╯┃┃┃╱╱┃┃

//╰╮┃┃╭┻╯┣╮╭┫╰━┳╮╭┳━━╮

//╱┃╰╯┃╭╮┃┃┃┃╭╮┃┃┃┃━━┫

//╱╰╮╭┫╰╯┃╰╯┃╰╯┃╰╯┣━━┃

//╱╱╰╯╰━━┻━━┻━━┻━━┻━━╯

//╭━━━┳╮╱╱╱╱╱╱╱╭╮

//┃╭━╮┃┃╱╱╱╱╱╱╱┃┃

//┃┃╱╰┫╰━┳━━┳━╮╭━╮╭━━┫┃

//┃┃╱╭┫╭╮┃╭╮┃╭╮┫╭╮┫┃━┫┃

//┃╰━╯┃┃┃┃╭╮┃┃┃┃┃┃┃┃━┫╰╮

//╰━━━┻╯╰┻╯╰┻╯╰┻╯╰┻━━┻━╯

//━╯

// http://www.vdubus.co.uk/

strategy(title='Vdub FX SniperVX3 / Strategy v3', shorttitle='Vdub_FX_SniperVX3_Strategy', overlay=true, pyramiding=0, initial_capital=1000, currency=currency.USD)

//Candle body resistance Channel-----------------------------//

len = 34

src = input(close, title="Candle body resistance Channel")

out = sma(src, len)

last8h = highest(close, 13)

lastl8 = lowest(close, 13)

bearish = cross(close,out) == 1 and falling(close, 1)

bullish = cross(close,out) == 1 and rising(close, 1)

channel2=input(false, title="Bar Channel On/Off")

ul2=plot(channel2?last8h:last8h==nz(last8h[1])?last8h:na, color=black, linewidth=1, style=linebr, title="Candle body resistance level top", offset=0)

ll2=plot(channel2?lastl8:lastl8==nz(lastl8[1])?lastl8:na, color=black, linewidth=1, style=linebr, title="Candle body resistance level bottom", offset=0)

//fill(ul2, ll2, color=black, transp=95, title="Candle body resistance Channel")

//-----------------Support and Resistance

RST = input(title='Support / Resistance length:', defval=10)

RSTT = valuewhen(high >= highest(high, RST), high, 0)

RSTB = valuewhen(low <= lowest(low, RST), low, 0)

RT2 = plot(RSTT, color=RSTT != RSTT[1] ? na : red, linewidth=1, offset=+0)

RB2 = plot(RSTB, color=RSTB != RSTB[1] ? na : green, linewidth=1, offset=0)

//--------------------Trend colour ema------------------------------------------------//

src0 = close, len0 = input(13, minval=1, title="EMA 1")

ema0 = ema(src0, len0)

direction = rising(ema0, 2) ? +1 : falling(ema0, 2) ? -1 : 0

plot_color = direction > 0 ? lime: direction < 0 ? red : na

plot(ema0, title="EMA", style=line, linewidth=1, color = plot_color)

//-------------------- ema 2------------------------------------------------//

src02 = close, len02 = input(21, minval=1, title="EMA 2")

ema02 = ema(src02, len02)

direction2 = rising(ema02, 2) ? +1 : falling(ema02, 2) ? -1 : 0

plot_color2 = direction2 > 0 ? lime: direction2 < 0 ? red : na

plot(ema02, title="EMA Signal 2", style=line, linewidth=1, color = plot_color2)

//=============Hull MA//

show_hma = input(false, title="Display Hull MA Set:")

hma_src = input(close, title="Hull MA's Source:")

hma_base_length = input(8, minval=1, title="Hull MA's Base Length:")

hma_length_scalar = input(5, minval=0, title="Hull MA's Length Scalar:")

hullma(src, length)=>wma(2*wma(src, length/2)-wma(src, length), round(sqrt(length)))

plot(not show_hma ? na : hullma(hma_src, hma_base_length+hma_length_scalar*6), color=black, linewidth=2, title="Hull MA")

//============ signal Generator ==================================//

Piriod=input('720')

ch1 = request.security(syminfo.tickerid, Piriod, open)

ch2 = request.security(syminfo.tickerid, Piriod, close)

longCondition = crossover(request.security(syminfo.tickerid, Piriod, close),request.security(syminfo.tickerid, Piriod, open))

if (longCondition)

strategy.entry("BUY", strategy.long)

shortCondition = crossunder(request.security(syminfo.tickerid, Piriod, close),request.security(syminfo.tickerid, Piriod, open))

if (shortCondition)

strategy.entry("SELL", strategy.short)

///////////////////////////////////////////////////////////////////////////////////////////