Analise pacientemente a estratégia de banda de média móvel tripla contendo informações valiosas na linha K

Visão geral

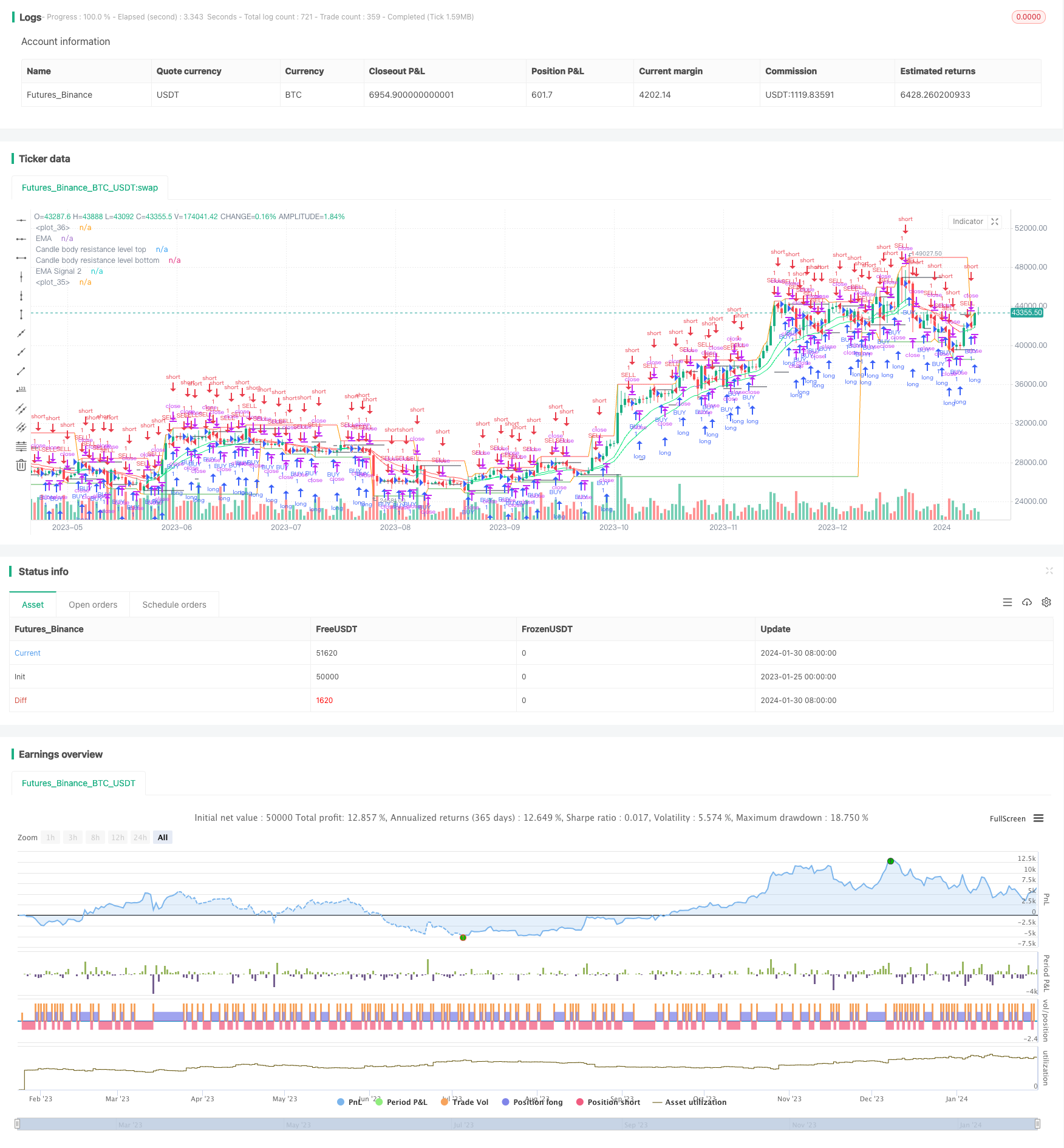

A estratégia de banda de onda de linha média tripla usa vários indicadores de média móvel para explorar as leis ocultas nas flutuações de preços através de uma análise profunda da linha K, permitindo negociações de arbitragem de baixo risco.

Princípio da estratégia

A estratégia consiste em sobrepor um conjunto de EMAs à base de linhas de Brin, construindo um canal de preços e descobrindo as leis de flutuação dos preços.

- Utilize o indicador BodyResistanceChannel para mapear o ponto de resistência de uma entidade em linha K.

- Use o indicador de Suporte/Resistência para traçar pontos de suporte e resistência de vários dias.

- O uso de um sistema de dupla EMA para determinar a direção da tendência dos preços.

- O indicador de linha média de Hull para suavizar a curva de preços.

Com base nisso, é possível identificar formas, avaliar oportunidades de reversão e elaborar estratégias de arbitragem.

Análise de vantagens

A estratégia tem as seguintes vantagens:

- Usando múltiplos EMAs para construir um canal de preços, é possível determinar claramente a direção da flutuação dos preços.

- Aplicando o indicador de linha média de Hull, pode-se determinar com eficácia a ruptura do preço de suavização.

- Combinando a forma inversa e o indicador de canal, permite transações de baixa probabilidade e baixo risco.

- Construção de um sistema de indicadores em várias camadas, com sinais de negociação estáveis e confiáveis.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

- O risco de ruptura do canal de preços pode levar a grandes perdas. A solução adequada é usar o stop loss móvel para reduzir as perdas individuais.

- Risco de erro de julgamento de forma invertida, provocando sinais errados. A solução específica é otimizar os parâmetros e melhorar a precisão de julgamento de forma.

- Risco de não correspondência de parâmetros do indicador, resultando em diminuição da qualidade do sinal de negociação. A solução específica é o teste de otimização de parâmetros de combinação múltipla.

Direção de otimização

A estratégia pode ser melhorada em:

- Optimizar a combinação de parâmetros do ciclo EMA para que o indicador seja mais adequado às características do mercado.

- Ajustar a posição de parada para minimizar o risco de perdas individuais, garantindo lucro.

- A adição de módulos de ajustamento de posição dinâmico baseado na volatilidade, para controlar o risco de forma eficaz.

- A tecnologia de aprendizagem profunda pode ser usada para extrair mais regras de preços e melhorar a qualidade do sinal.

Resumir

A estratégia de três bandas de ondas de linha uniforme explora profundamente a lei da oscilação dos preços, é estável e eficiente, e vale a pena a aplicação e otimização contínua a longo prazo. O investimento requer racionalidade e paciência, e o caminho para a vitória é o progresso.

/*backtest

start: 2023-01-25 00:00:00

end: 2024-01-31 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//╭╮╱╱╭╮╭╮╱╱╭╮

//┃╰╮╭╯┃┃┃╱╱┃┃

//╰╮┃┃╭┻╯┣╮╭┫╰━┳╮╭┳━━╮

//╱┃╰╯┃╭╮┃┃┃┃╭╮┃┃┃┃━━┫

//╱╰╮╭┫╰╯┃╰╯┃╰╯┃╰╯┣━━┃

//╱╱╰╯╰━━┻━━┻━━┻━━┻━━╯

//╭━━━┳╮╱╱╱╱╱╱╱╭╮

//┃╭━╮┃┃╱╱╱╱╱╱╱┃┃

//┃┃╱╰┫╰━┳━━┳━╮╭━╮╭━━┫┃

//┃┃╱╭┫╭╮┃╭╮┃╭╮┫╭╮┫┃━┫┃

//┃╰━╯┃┃┃┃╭╮┃┃┃┃┃┃┃┃━┫╰╮

//╰━━━┻╯╰┻╯╰┻╯╰┻╯╰┻━━┻━╯

//━╯

// http://www.vdubus.co.uk/

strategy(title='Vdub FX SniperVX3 / Strategy v3', shorttitle='Vdub_FX_SniperVX3_Strategy', overlay=true, pyramiding=0, initial_capital=1000, currency=currency.USD)

//Candle body resistance Channel-----------------------------//

len = 34

src = input(close, title="Candle body resistance Channel")

out = sma(src, len)

last8h = highest(close, 13)

lastl8 = lowest(close, 13)

bearish = cross(close,out) == 1 and falling(close, 1)

bullish = cross(close,out) == 1 and rising(close, 1)

channel2=input(false, title="Bar Channel On/Off")

ul2=plot(channel2?last8h:last8h==nz(last8h[1])?last8h:na, color=black, linewidth=1, style=linebr, title="Candle body resistance level top", offset=0)

ll2=plot(channel2?lastl8:lastl8==nz(lastl8[1])?lastl8:na, color=black, linewidth=1, style=linebr, title="Candle body resistance level bottom", offset=0)

//fill(ul2, ll2, color=black, transp=95, title="Candle body resistance Channel")

//-----------------Support and Resistance

RST = input(title='Support / Resistance length:', defval=10)

RSTT = valuewhen(high >= highest(high, RST), high, 0)

RSTB = valuewhen(low <= lowest(low, RST), low, 0)

RT2 = plot(RSTT, color=RSTT != RSTT[1] ? na : red, linewidth=1, offset=+0)

RB2 = plot(RSTB, color=RSTB != RSTB[1] ? na : green, linewidth=1, offset=0)

//--------------------Trend colour ema------------------------------------------------//

src0 = close, len0 = input(13, minval=1, title="EMA 1")

ema0 = ema(src0, len0)

direction = rising(ema0, 2) ? +1 : falling(ema0, 2) ? -1 : 0

plot_color = direction > 0 ? lime: direction < 0 ? red : na

plot(ema0, title="EMA", style=line, linewidth=1, color = plot_color)

//-------------------- ema 2------------------------------------------------//

src02 = close, len02 = input(21, minval=1, title="EMA 2")

ema02 = ema(src02, len02)

direction2 = rising(ema02, 2) ? +1 : falling(ema02, 2) ? -1 : 0

plot_color2 = direction2 > 0 ? lime: direction2 < 0 ? red : na

plot(ema02, title="EMA Signal 2", style=line, linewidth=1, color = plot_color2)

//=============Hull MA//

show_hma = input(false, title="Display Hull MA Set:")

hma_src = input(close, title="Hull MA's Source:")

hma_base_length = input(8, minval=1, title="Hull MA's Base Length:")

hma_length_scalar = input(5, minval=0, title="Hull MA's Length Scalar:")

hullma(src, length)=>wma(2*wma(src, length/2)-wma(src, length), round(sqrt(length)))

plot(not show_hma ? na : hullma(hma_src, hma_base_length+hma_length_scalar*6), color=black, linewidth=2, title="Hull MA")

//============ signal Generator ==================================//

Piriod=input('720')

ch1 = request.security(syminfo.tickerid, Piriod, open)

ch2 = request.security(syminfo.tickerid, Piriod, close)

longCondition = crossover(request.security(syminfo.tickerid, Piriod, close),request.security(syminfo.tickerid, Piriod, open))

if (longCondition)

strategy.entry("BUY", strategy.long)

shortCondition = crossunder(request.security(syminfo.tickerid, Piriod, close),request.security(syminfo.tickerid, Piriod, open))

if (shortCondition)

strategy.entry("SELL", strategy.short)

///////////////////////////////////////////////////////////////////////////////////////////