Обзор

Стратегия пересечения движущихся средних, основанная на двух равновесных линиях, является простым и эффективным методом торговли в течение дня, предназначенным для выявления потенциальных возможностей покупки и продажи на рынке путем анализа взаимосвязи между движущимися средними двух различных циклов. Эта стратегия использует краткосрочную простую движущуюся среднюю (SMA) и долгосрочную простую движущуюся среднюю, которая указывает на потенциальные возможности покупки, когда она пересекает долгосрочную среднюю на краткосрочной средней; наоборот, когда она пересекает долгосрочную среднюю ниже короткой средней, она указывает на сигнал падения, указывающий на потенциальные возможности продажи.

Стратегический принцип

Основной принцип этой стратегии заключается в том, чтобы использовать тенденционные характеристики и отставание движущихся средних с различными периодами, чтобы судить о направлении тенденции на текущем рынке, сравнивая краткосрочные средние и долгосрочные средние, и принимать соответствующие торговые решения. Когда рынок имеет тенденцию к повышению, цена сначала прорывает долгосрочную среднюю, а затем пересекает долгосрочную среднюю, образуя золотую вилку, создавая сигнал покупки; когда рынок имеет тенденцию к снижению, цена сначала падает на долгосрочную среднюю, а затем пересекает долгосрочную среднюю, образуя мертвую вилку, создавая сигнал продажи.

Стратегические преимущества

- Простая и понятная: стратегия основана на классической теории движущихся средних, логика четкая, легко понятна и реализуема.

- Эластичность: Стратегия может применяться на нескольких рынках и в различных торговых видах, и может гибко реагировать на различные рыночные особенности путем корректировки параметров.

- Поймать тренд: определить направление тренда с помощью пересечения двойных равнозначных линий, что помогает трейдерам вовремя следить за основными тенденциями и увеличивать возможности получения прибыли.

- Управление рисками: стратегия вводит концепцию управления рисками, чтобы контролировать риск на каждой сделке путем корректировки позиции и эффективно управлять потенциальными потерями.

- Снижение шума: использование задержек средней линии для эффективной фильтрации случайного шума на рынке и повышения надежности торговых сигналов.

Стратегический риск

- Выбор параметров: различные параметры имеют важное влияние на эффективность стратегии. Неправильный выбор может привести к ее сбоям или плохой производительности.

- Рыночные тенденции: в случае, если стратегия может потерять в течение длительного периода времени в условиях рыночной нестабильности или в момент перелома тенденции.

- Стоимость скольжения: частое совершение сделок может привести к более высокой стоимости скольжения, что может повлиять на общую прибыль стратегии.

- Чёрные свинны: стратегия плохо адаптирована к экстремальным ситуациям, и черные свинны могут привести к огромным потерям.

- Риск перенастройки: если оптимизация параметров слишком зависит от исторических данных, это может привести к тому, что стратегия будет плохо работать в реальных сделках.

Направление оптимизации стратегии

- Динамическая оптимизация параметров: динамическая корректировка параметров стратегии в зависимости от изменения состояния рынка, повышение адаптивности.

- Подтверждение тренда: после создания торгового сигнала, ввод других индикаторов или моделей поведения цен для подтверждения тренда, повышения надежности сигнала.

- Стоп-стоп: внедрение разумных стоп-стоп механизмов для дальнейшего контроля рискового порога для отдельных сделок.

- Управление позициями: методы оптимизации корректировки позиций, например, введение показателей волатильности, динамическая корректировка позиций в соответствии с уровнем волатильности рынка.

- Оценка множественной воздушной силы: оценка соотношения между многоголовной и воздушной силой, вмешательство в начале тренда, повышение точности захвата тренда.

Подвести итог

Стратегия движущихся средних, основанная на скрещивании двух равновесных линий, является простым и практичным методом дневного торговли, который определяет направление рыночной тенденции путем сравнения позиционных отношений между различными циклическими равновесными линиями и генерирует торговые сигналы. Логика стратегии ясна, адаптивна, эффективно улавливает рыночные тенденции, в то же время вводит меры по управлению рисками и контролирует потенциальные потери.

Overview

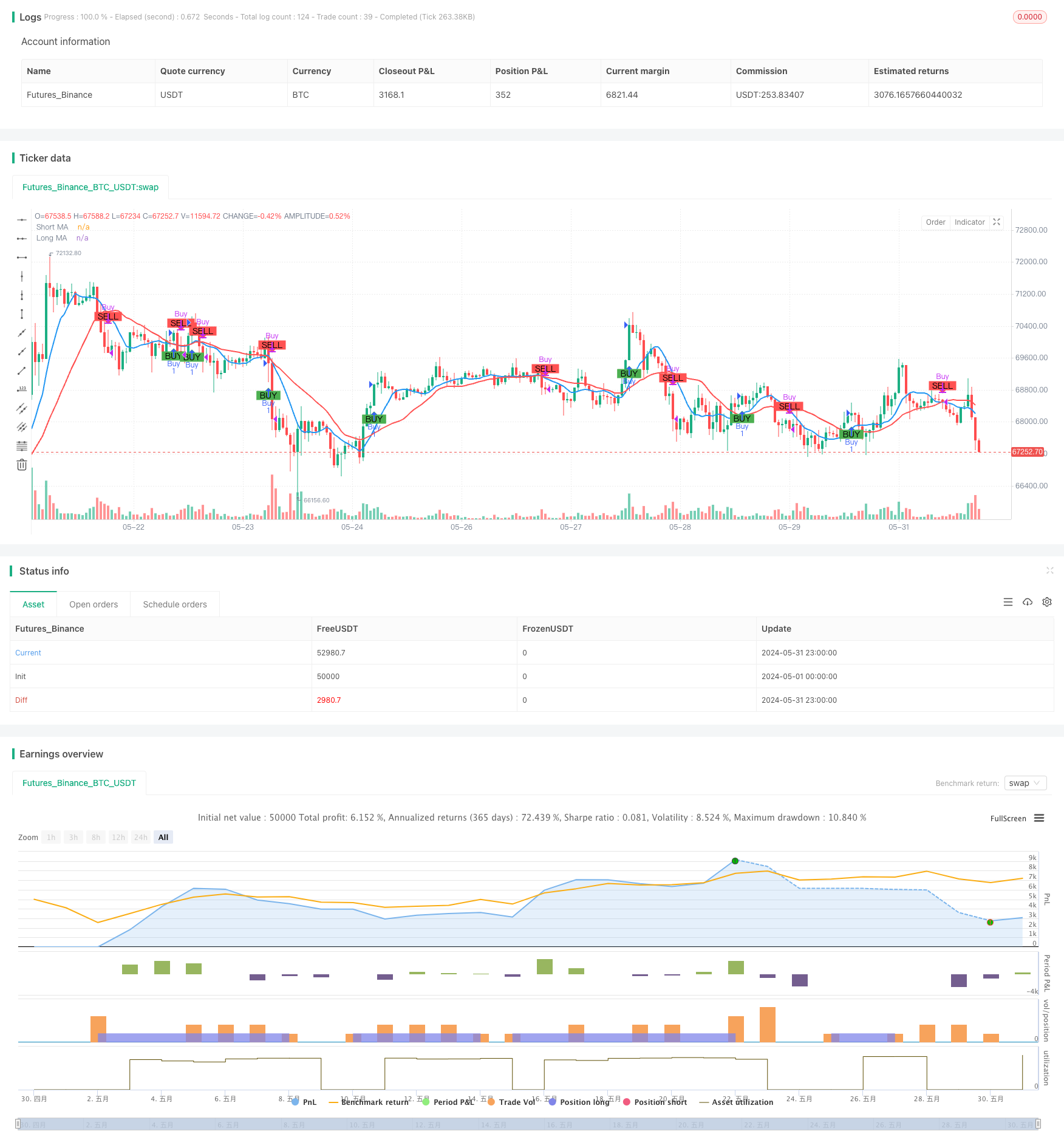

The Moving Average Crossover Strategy based on dual moving averages is a straightforward and effective intraday trading approach designed to identify potential buy and sell opportunities in the market by analyzing the relationship between two moving averages of different periods. This strategy utilizes a short-term simple moving average (SMA) and a long-term simple moving average. When the short-term moving average crosses above the long-term moving average, it indicates a bullish signal, suggesting a potential buying opportunity. Conversely, when the short-term moving average crosses below the long-term moving average, it indicates a bearish signal, suggesting a potential selling opportunity. This crossover method helps traders capture trending moves in the market while minimizing market noise interference.

Strategy Principle

The core principle of this strategy is to utilize the trend characteristics and lag of moving averages with different periods. By comparing the relative position relationship between the short-term moving average and the long-term moving average, it determines the current market trend direction and makes corresponding trading decisions. When an upward trend emerges in the market, the price will first break through the long-term moving average, and the short-term moving average will subsequently cross above the long-term moving average, forming a golden cross and generating a buy signal. When a downward trend emerges in the market, the price will first break below the long-term moving average, and the short-term moving average will subsequently cross below the long-term moving average, forming a death cross and generating a sell signal. In the parameter settings of this strategy, the period of the short-term moving average is set to 9, and the period of the long-term moving average is set to 21. These two parameters can be adjusted based on market characteristics and personal preferences. Additionally, this strategy introduces the concept of money management by setting the initial capital and risk percentage per trade, using position sizing to control the risk exposure of each trade.

Strategy Advantages

- Simplicity: This strategy is based on the classic moving average theory, with clear logic and easy to understand and implement.

- Adaptability: This strategy can be applied to multiple markets and different trading instruments. By adjusting parameter settings, it can flexibly adapt to different market characteristics.

- Trend Capture: By using the dual moving average crossover to determine the trend direction, it helps traders timely follow the mainstream trend and increase profit opportunities.

- Risk Control: This strategy introduces the concept of risk management, using position sizing to control the risk exposure of each trade, effectively managing potential losses.

- Noise Reduction: By utilizing the lag characteristic of moving averages, it effectively filters out random noise in the market, improving the reliability of trading signals.

Strategy Risks

- Parameter Selection: Different parameter settings can have a significant impact on strategy performance. Improper selection may lead to strategy failure or poor performance.

- Market Trend: In ranging markets or trend turning points, this strategy may experience consecutive losses.

- Slippage Costs: Frequent trading may result in higher slippage costs, affecting the overall profitability of the strategy.

- Black Swan Events: This strategy has poor adaptability to extreme market conditions, and black swan events may cause significant losses to the strategy.

- Overfitting Risk: If parameter optimization relies too heavily on historical data, it may lead to poor performance of the strategy in actual trading.

Strategy Optimization Directions

- Dynamic Parameter Optimization: Dynamically adjust strategy parameters based on changes in market conditions to improve adaptability.

- Trend Confirmation: After generating trading signals, introduce other indicators or price behavior patterns to confirm the trend, improving signal reliability.

- Stop-Loss and Take-Profit: Introduce reasonable stop-loss and take-profit mechanisms to further control the risk exposure of each trade.

- Position Management: Optimize the position sizing method, such as introducing volatility indicators to dynamically adjust positions based on market volatility levels.

- Long-Short Strength Assessment: Assess the comparative relationship between bullish and bearish strengths, entering at the early stage of a trend to improve the accuracy of trend capture.

Summary

The Moving Average Crossover Strategy based on dual moving averages is a simple and practical intraday trading method. By comparing the position relationship of moving averages with different periods, it determines the market trend direction and generates trading signals. This strategy has clear logic, strong adaptability, and can effectively capture market trends while introducing risk management measures to control potential losses. However, this strategy also has potential risks such as parameter selection, trend reversal, frequent trading, etc. It needs to be further improved through dynamic optimization, signal confirmation, position management, and other methods to enhance the robustness and profitability of the strategy. In general, as a classic technical analysis indicator, the basic principles and practical application value of moving averages have been widely verified by the market. It is a trading strategy worthy of in-depth research and continuous optimization.

/*backtest

start: 2024-05-01 00:00:00

end: 2024-05-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Moving Average Crossover Strategy", overlay=true)

// Input parameters

shortLength = input.int(9, title="Short Moving Average Length")

longLength = input.int(21, title="Long Moving Average Length")

capital = input.float(100000, title="Initial Capital")

risk_per_trade = input.float(1.0, title="Risk Per Trade (%)")

// Calculate Moving Averages

shortMA = ta.sma(close, shortLength)

longMA = ta.sma(close, longLength)

// Plot Moving Averages

plot(shortMA, title="Short MA", color=color.blue, linewidth=2)

plot(longMA, title="Long MA", color=color.red, linewidth=2)

// Generate Buy/Sell signals

longCondition = ta.crossover(shortMA, longMA)

shortCondition = ta.crossunder(shortMA, longMA)

// Plot Buy/Sell signals

plotshape(series=longCondition, title="Buy Signal", location=location.belowbar, color=color.green, style=shape.labelup, text="BUY")

plotshape(series=shortCondition, title="Sell Signal", location=location.abovebar, color=color.red, style=shape.labeldown, text="SELL")

// Risk management: calculate position size

risk_amount = capital * (risk_per_trade / 100)

position_size = risk_amount / close

// Execute Buy/Sell orders with position size

if (longCondition)

strategy.entry("Buy", strategy.long, qty=1, comment="Buy")

if (shortCondition)

strategy.close("Buy", comment="Sell")

// Display the initial capital and risk per trade on the chart

var label initialLabel = na

if (na(initialLabel))

initialLabel := label.new(x=bar_index, y=high, text="Initial Capital: " + str.tostring(capital) + "\nRisk Per Trade: " + str.tostring(risk_per_trade) + "%", style=label.style_label_down, color=color.white, textcolor=color.black)

else

label.set_xy(initialLabel, x=bar_index, y=high)