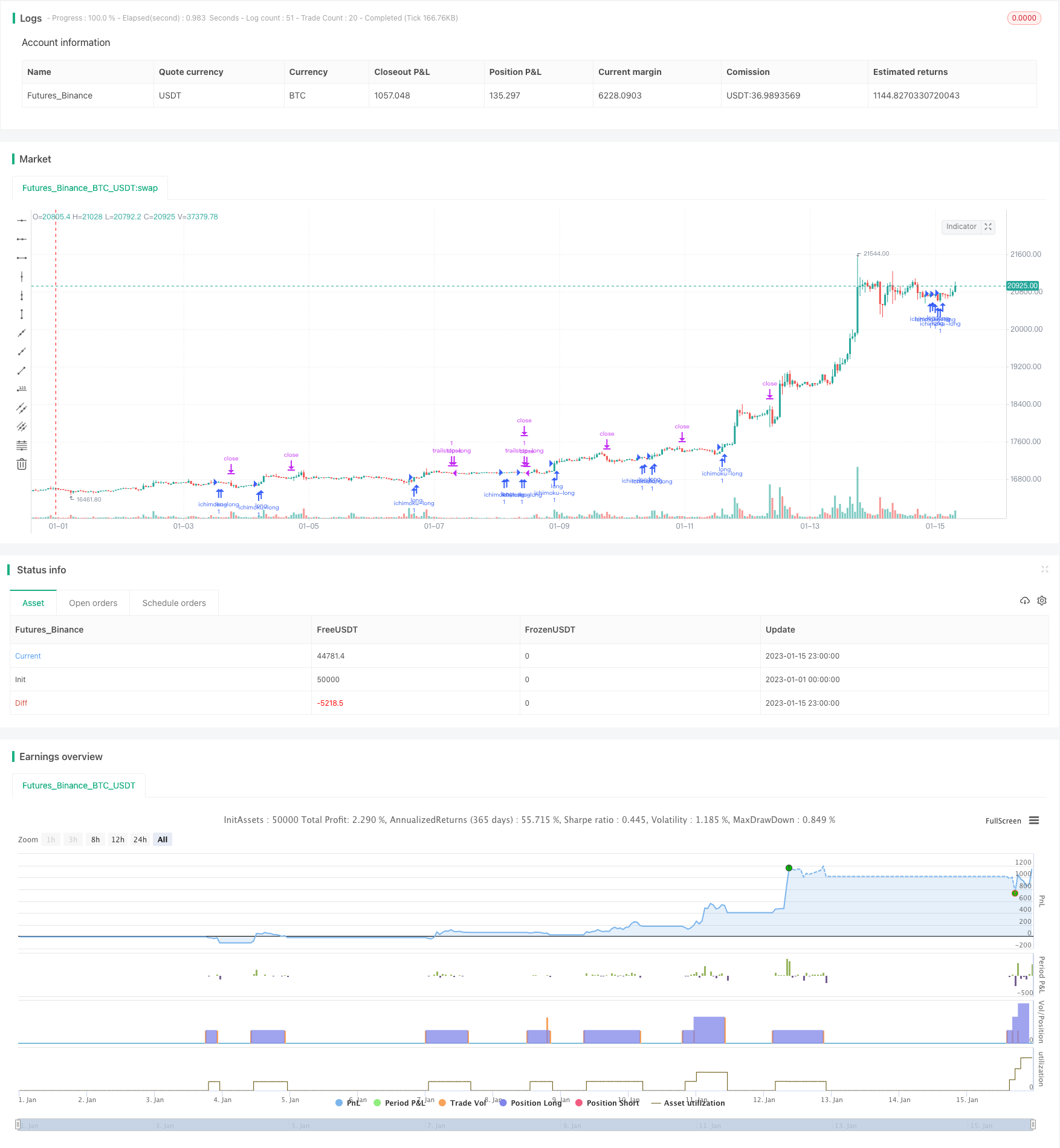

概述

该策略运用一目均衡线实现日内股票交易,属于短线交易策略。它利用一目均衡线的转换线、基准线以及先行线组合进行买卖信号判断,并辅以抛物线SAR进行止损追踪,实现双重保护。

原理

一目均衡线由转换线、基准线、先行1线和先行2线组成。转换线为当日收盘价和过去9日的最高价最低价均价的平均值,反映最近一段时间内的股价均衡态势。基准线为过去26日的最高价最低价均价,代表中长期的均衡态势。先行1线为基准线和转换线的均价,反映未来走势的态势。先行2线为过去52日的最高价最低价均价。这些均衡线组合起来,形成买卖讯号。

当收盘价从下方突破基准线且高于先行2线时,产生买进讯号。当收盘价从上方跌破基准线且低于先行1线时,产生卖出讯号。抛物线SAR用于追踪止损,当价格低于SAR时发出止损信号。

该策略利用均衡线的组合,判断股价的未来趋势和目前趋势的持续性,属于典型的趋势跟踪策略。当出现买进和卖出讯号时,及时追随趋势进行交易。同时,SAR止损让利机制可避免亏损扩大。

优势

- 利用均衡线判断未来趋势,提高判断准确性

均衡线包含不同周期价格信息,能提前反映趋势变化,利用组合判断增加准确性。相比单一指标,能更准确判断买卖点。

- SAR止损追踪,双重保护

SAR能灵活跟踪股票运行,进行止损。与均衡线组合,能在获利后及时止损,避免亏损扩大。

- 简单参数设定,容易实施

该策略只有少量参数,不依赖曲线拟合等复杂技术指标,简单实用,容易实施。参数默认值就可达到不错效果。

- 适用于日内短线交易

利用日内价格变化判断买卖点,属于短线交易策略。可充分利用股票日内波动获利。

风险

- 回撤风险

跟踪趋势买卖带来较高回撤。需要合理设置止损点,控制单次亏损。

- 震荡行情风险

震荡行情中,均衡线产生的讯号可能频繁,不利于获利。可适当调整参数,过滤掉一些讯号。

- 过优化风险

简单的参数容易过优化,实盘效果可能不理想。应进行稳健性测试,防止过拟合。

- 效果因标的不同有所区别

效果与选股标的有关,应选择趋势明显的股票进行交易,使策略发挥最大效果。

优化方向

- 结合其他指标过滤信号

可以结合移动平均线等其他指标,过滤掉一些不确定信号,避免虚拟交易。

- 动态调整止损点

可以根据市场波动程度,动态调整SAR的参数,使止损更灵活。

- 优化参数组合

可以通过更系统的优化和组合测试,寻找更佳的参数组合,提高策略效果。

- 根据市场环境调整持仓

可以根据大盘走势等市场环境,动态调整策略的仓位和头寸,控制风险。

总结

该策略利用均衡线的买卖信号,配合抛物线SAR实现止损追踪,是一种较为简单实用的短线交易策略。有效利用均衡线预测未来趋势的功能,对突破进行买卖操作。同时止损机制避免亏损加大。实施时需要注意回撤控制,选股以及参数优化等问题。如果解决了这些问题,它是一个易于实施且效果不俗的日内交易策略。

/*backtest

start: 2023-01-01 00:00:00

end: 2023-01-16 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

//

// Based on the trading strategy described at

// http://stockcharts.com/school/doku.php?id=chart_school:trading_strategies:ichimoku_cloud

//

// See Also:

// - Backtesting and forwardtesting (of TradingView Strategies) <https://www.tradingview.com/wiki/Strategies#Backtesting_and_forwardtesting>

// - 9 Mistakes Quants Make that Cause Backtests to Lie <https://blog.quantopian.com/9-mistakes-quants-make-that-cause-backtests-to-lie-by-tucker-balch-ph-d/>

// - When Backtests Meet Reality <http://financial-hacker.com/Backtest.pdf>

// - Why MT4 backtesting does not work <http://www.stevehopwoodforex.com/phpBB3/viewtopic.php?f=28&t=4020>

//

//

// -----------------------------------------------------------------------------

// Copyright 2018 sherwind

//

// This program is free software: you can redistribute it and/or modify

// it under the terms of the GNU General Public License as published by

// the Free Software Foundation, either version 3 of the License, or

// any later version.

//

// This program is distributed in the hope that it will be useful,

// but WITHOUT ANY WARRANTY; without even the implied warranty of

// MERCHANTABILITY or FITNESS FOR A PARTICULAR PURPOSE. See the

// GNU General Public License for more details.

//

// The GNU General Public License can be found here

// <http://www.gnu.org/licenses/>.

//

// -----------------------------------------------------------------------------

//

strategy(title="Ichimoku Cloud Strategy", shorttitle="Ichimoku Strategy", overlay=true, pyramiding=3)

conversionPeriods = input(9, minval=1, title="Conversion Line Periods"),

basePeriods = input(26, minval=1, title="Base Line Periods")

laggingSpan2Periods = input(52, minval=1, title="Lagging Span 2 Periods"),

displacement = input(26, minval=1, title="Displacement")

usePSARTrailStop = input(true, title="Use Parabolic SAR for Trailing Stop")

psarStart = input(0.02, title="Parabolic SAR Start")

psarIncrement = input(0.02, title="Parabolic SAR Increment")

psarMaximum = input(0.2, title="Parabolic SAR Maximum")

donchian(len) => avg(lowest(len), highest(len))

conversionLine = donchian(conversionPeriods)

baseLine = donchian(basePeriods)

leadLine1 = avg(conversionLine, baseLine)

leadLine2 = donchian(laggingSpan2Periods)

leadLineDisp1 = leadLine1[displacement]

leadLineDisp2 = leadLine2[displacement]

psar = sar(psarStart, psarIncrement, psarMaximum)

// BUY Signal:

// close > leading span b and

// leading span a > leading span b and

// close crosses over base line and

// close > parabolic sar

buySignal = close > leadLineDisp2 and

leadLineDisp1 > leadLineDisp2 and

crossover(close, baseLine) and

(usePSARTrailStop ? close > psar : not usePSARTrailStop)

// Sell Signal:

// close < leading span a and

// leading span a < leading span b and

// close crosses under base line and

// close < psar

sellSignal = close < leadLineDisp1 and

leadLineDisp1 < leadLineDisp2 and

crossunder(close, baseLine) and

(usePSARTrailStop ? close < psar : not usePSARTrailStop)

hasLong = strategy.position_size > 0

hasShort = strategy.position_size < 0

strategy.entry("ichimoku-long", strategy.long, when = buySignal)

strategy.entry("ichimoku-short", strategy.short, when = sellSignal)

strategy.exit("trailstop-long", "ichimoku-long", stop = psar, when = hasLong and usePSARTrailStop)

strategy.exit("trailstop-short", "ichimoku-short", stop = psar, when = hasShort and usePSARTrailStop)