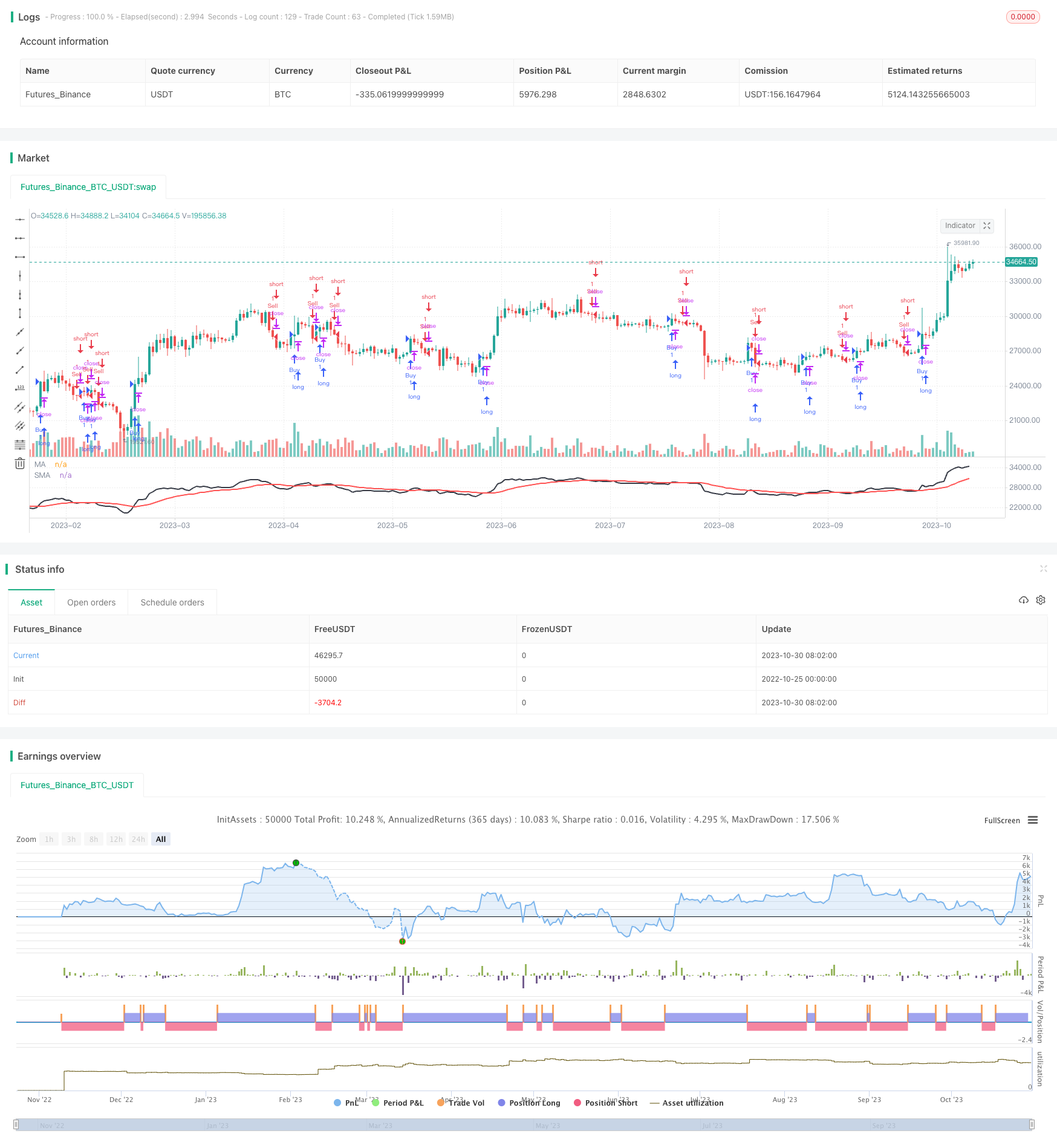

概述

本策略运用滑动平均线技术作为主要交易信号,结合海肯烛形指标检测市场趋势反转,捕捉短期价格动量的策略。策略优化自古斯塔沃·布拉努的海肯均线策略,通过去除重漆功能,实现无滞后信号输出。

策略原理

计算海肯收盘价nAMAn,作为价格主线。

计算海肯收盘价的快速移动平均线fma和慢速移动平均线sma。

当fma上穿sma时生成买入信号;当fma下穿sma时生成卖出信号。

该策略去除了原策略中的重漆功能,能够实时生成交易信号,避免回测数据失真。

优势分析

结合海肯烛形指标,能更准确判断市场趋势反转点。

应用双平均线组合,能有效过滤假突破。

无滞后信号输出,实盘表现可靠。

参数优化灵活,可针对不同品种进行调整。

策略逻辑简单清晰,容易理解实现。

可配置成全自动交易策略,降低人为操作风险。

风险分析

海肯均线对价格震荡市场表现不佳。

双均线交易策略容易产生较多虚假信号。

平均线参数设置不当,会错过趋势或者增大回撤。

实盘有交易费用,会对净利产生一定影响。

需要严格的止损方式,控制单笔亏损。

机械交易策略有回撤风险,需掌握好资金管理。

对应风险管理措施:

结合波动率指标,避开震荡区间。

增加过滤条件,确保交易信号质量。

参数测试优化,选择合适的均线组合。

调整交易频率,降低交易成本影响。

设置合理的止损位,控制单笔亏损。

优化资金管理,严格控制仓位规模。

策略优化方向

优化双均线参数组合,提高信号质量。

增加趋势过滤指标,避开震荡区间。

结合成交量指标,确保趋势可靠性。

设置动态止损和跟踪止盈,优化利润收集。

整合资金管理模块,控制仓位规模。

增加算法交易模块,实现全自动化。

总结

本策略整合海肯均线趋势判断和双均线组合过滤技术,实现了一个简单实用的短期趋势追踪策略。策略信号生成实时可靠,实盘表现良好。通过参数优化、风控措施设置以及算法交易模块扩展,可以将其优化为一个值得信赖的全自动交易策略。

策略源码

/*backtest

start: 2022-10-25 00:00:00

end: 2023-10-31 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

//Heikin/Kaufman by Gustavo v5

// strategy('Heikin Ashi EMA v5 no repaint ', shorttitle='Heikin Ashi EMA v5 no repaint', overlay=true, max_bars_back=500, default_qty_value=1000, initial_capital=100000, currency=currency.EUR)

// Settings - H/K

res1 = input.timeframe(title='Heikin Ashi EMA Time Frame', defval='D')

test = input(0, 'Heikin Ashi EMA Shift')

sloma = input(20, 'Slow EMA Period')

nAMA = hlc3

//Kaufman MA

Length = input.int(5, minval=1)

xPrice = input(hlc3)

xvnoise = math.abs(xPrice - xPrice[1])

Fastend = input.float(2.5, step=.5)

Slowend = input(20)

nfastend = 2 / (Fastend + 1)

nslowend = 2 / (Slowend + 1)

nsignal = math.abs(xPrice - xPrice[Length])

nnoise = math.sum(xvnoise, Length)

nefratio = nnoise != 0 ? nsignal / nnoise : 0

nsmooth = math.pow(nefratio * (nfastend - nslowend) + nslowend, 2)

nAMAn = nz(nAMA[1]) + nsmooth * (xPrice - nz(nAMA[1]))

//Heikin Ashi Open/Close Price

ha_t = ticker.heikinashi(syminfo.tickerid)

ha_close = request.security(ha_t, timeframe.period, nAMAn)

mha_close = request.security(ha_t, res1, hlc3)

//Moving Average

fma = ta.ema(mha_close[test], 1)

sma = ta.ema(ha_close, sloma)

plot(fma, title='MA', color=color.new(color.black, 0), linewidth=2, style=plot.style_line)

plot(sma, title='SMA', color=color.new(color.red, 0), linewidth=2, style=plot.style_line)

//Strategy

golong = ta.crossover(fma, sma)

goshort = ta.crossunder(fma, sma)

strategy.entry('Buy', strategy.long, when=golong)

strategy.entry('Sell', strategy.short,when=goshort)