概述

双重反转动量指数策略是一种结合了123反转策略和相对动量指数(RMI)策略的组合策略。它旨在通过利用双重信号提高交易决策的准确性。

策略原理

该策略由两部分组成:

123反转策略

- 当昨日收盘价低于前日,今日收盘价高于前日,且9日Slow K线低于50时,做多

- 当昨日收盘价高于前日,今日收盘价低于前日,且9日Fast K线高于50时,做空

相对动量指数(RMI)策略

- RMI是在RSI的基础上加入了动量因素的变种。它计算公式为:RMI = (上行动量SMA)/(下行动量SMA) * 100

- 当RMI低于超买线时,做多;当RMI高于超卖线时,做空

该组合策略只有当123反转和RMI双重信号同向发出时,才会产生交易信号。这可以有效减少错误交易的机会。

策略优势分析

该策略具有以下优势:

- 结合双重指标,提高信号准确性

- 利用反转策略,适合震荡行情

- RMI指标灵敏,可以识别强势趋势的转折点

策略风险分析

该策略也存在一些风险:

- 双重过滤会错过部分交易机会

- 反转信号可能出现误判

- RMI参数设置不当会影响效果

可以通过调整参数组合、优化指标计算方式来降低这些风险。

策略优化方向

该策略还可以从以下几个方面进行优化:

- 测试不同的参数组合,找到最佳参数

- 尝试不同的反转指标组合,如KDJ、MACD等

- 对RMI公式进行调整,使其更灵敏

- 添加止损机制,控制单笔损失

- 结合交易量,避免虚假信号

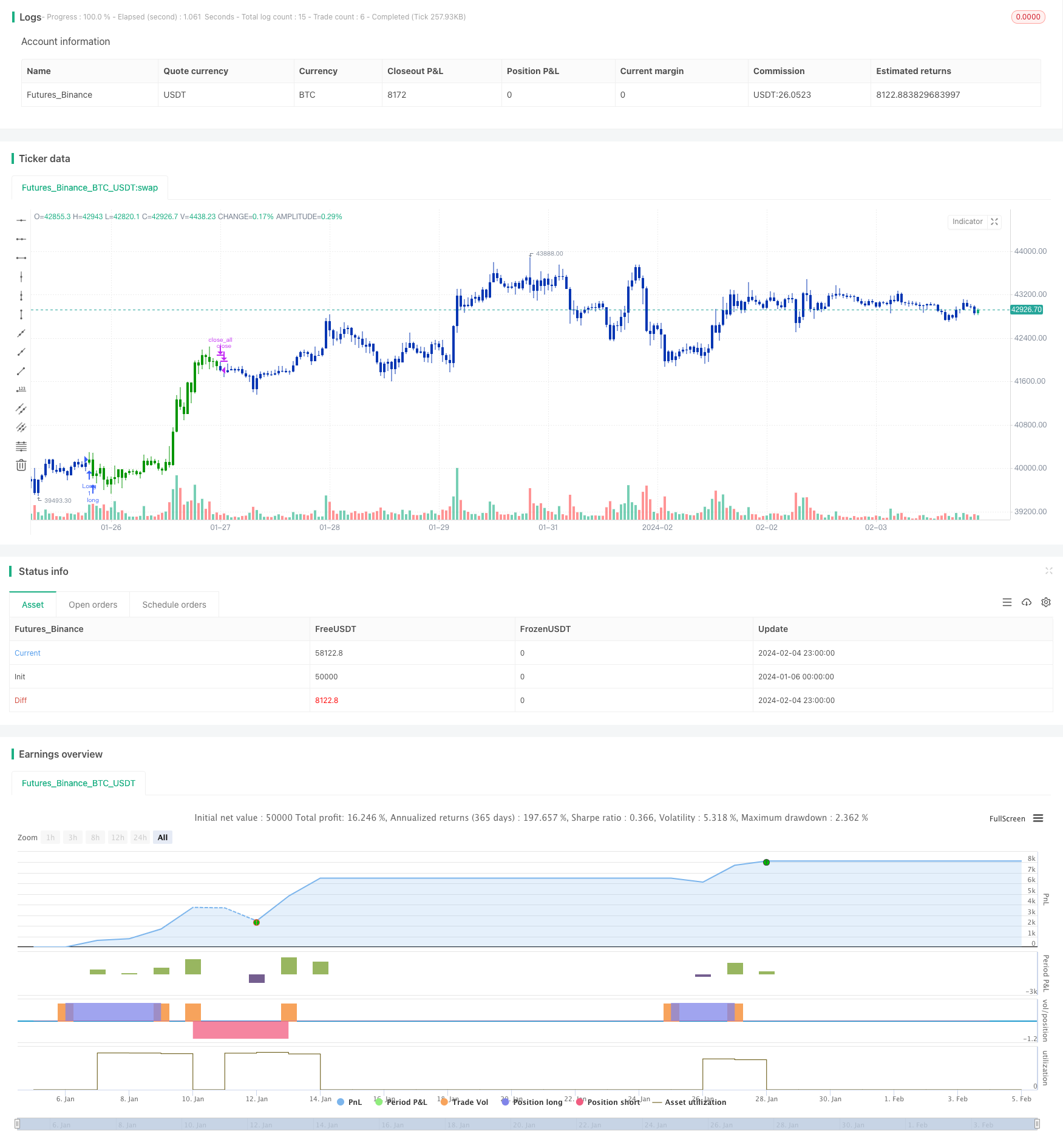

总结

双重反转动量指数策略通过双重信号过滤和参数优化,能够有效地提高交易决策的准确性,降低错误信号的概率。它适用于震荡行情,能挖掘反转机会。该策略可以通过调整参数和优化指标计算方式来进一步增强效果和 laps 风险。

策略源码

/*backtest

start: 2024-01-06 00:00:00

end: 2024-02-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/06/2021

// This is combo strategies for get a cumulative signal.

//

// First strategy

// This System was created from the Book "How I Tripled My Money In The

// Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

// The strategy buys at market, if close price is higher than the previous close

// during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

// The strategy sells at market, if close price is lower than the previous close price

// during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

//

// Second strategy

// The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

// with the Relative Strength Index's sensitivity to the number of look-back

// periods, yet frustrated with it's inconsistent oscillation between defined

// overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

// As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

// up and down days from close to close as the RSI does, the RMI counts up and down

// days from the close relative to the close x-days ago where x is not necessarily

// 1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

// substituted for "strength".

//

// WARNING:

// - For purpose educate only

// - This script to change bars colors.

////////////////////////////////////////////////////////////

Reversal123(Length, KSmoothing, DLength, Level) =>

vFast = sma(stoch(close, high, low, Length), KSmoothing)

vSlow = sma(vFast, DLength)

pos = 0.0

pos := iff(close[2] < close[1] and close > close[1] and vFast < vSlow and vFast > Level, 1,

iff(close[2] > close[1] and close < close[1] and vFast > vSlow and vFast < Level, -1, nz(pos[1], 0)))

pos

RMI(Length,BuyZone, SellZone) =>

pos = 0.0

xMU = 0.0

xMD = 0.0

xPrice = close

xMom = xPrice - xPrice[Length]

xMU := iff(xMom >= 0, nz(xMU[1], 1) - (nz(xMU[1],1) / Length) + xMom, nz(xMU[1], 1))

xMD := iff(xMom <= 0, nz(xMD[1], 1) - (nz(xMD[1],1) / Length) + abs(xMom), nz(xMD[1], 0))

RM = xMU / xMD

nRes = 100 * (RM / (1+RM))

pos:= iff(nRes < BuyZone, 1,

iff(nRes > SellZone, -1, nz(pos[1], 0)))

pos

strategy(title="Combo Backtest 123 Reversal & Relative Momentum Index", shorttitle="Combo", overlay = true)

line1 = input(true, "---- 123 Reversal ----")

Length = input(14, minval=1)

KSmoothing = input(1, minval=1)

DLength = input(3, minval=1)

Level = input(50, minval=1)

//-------------------------

line2 = input(true, "---- Relative Momentum Index ----")

LengthRMI = input(20, minval=1)

BuyZone = input(40, minval=1)

SellZone = input(70, minval=1)

reverse = input(false, title="Trade reverse")

posReversal123 = Reversal123(Length, KSmoothing, DLength, Level)

posRMI = RMI(LengthRMI,BuyZone, SellZone)

pos = iff(posReversal123 == 1 and posRMI == 1 , 1,

iff(posReversal123 == -1 and posRMI == -1, -1, 0))

possig = iff(reverse and pos == 1, -1,

iff(reverse and pos == -1 , 1, pos))

if (possig == 1 )

strategy.entry("Long", strategy.long)

if (possig == -1 )

strategy.entry("Short", strategy.short)

if (possig == 0)

strategy.close_all()

barcolor(possig == -1 ? #b50404: possig == 1 ? #079605 : #0536b3 )