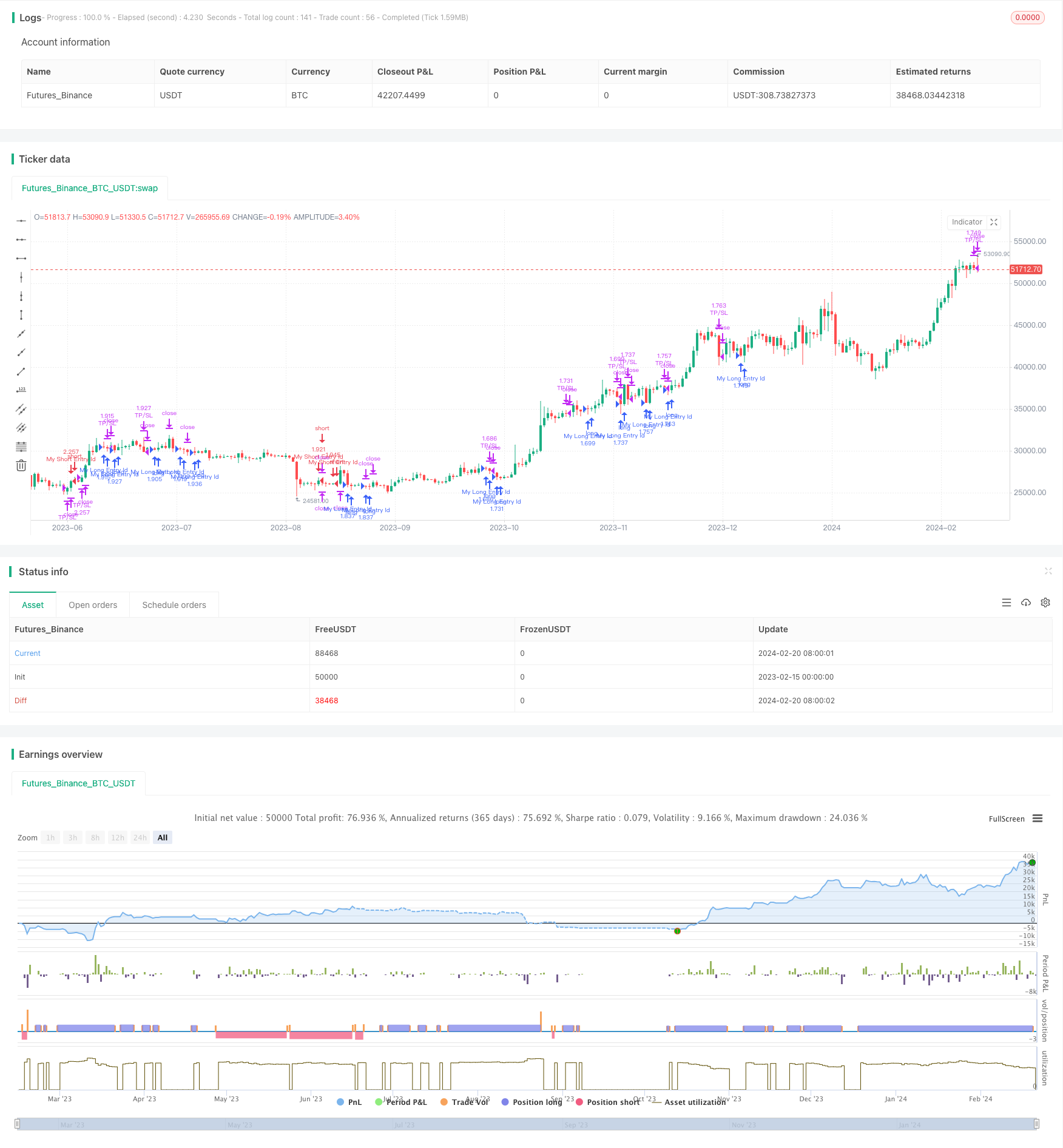

概述

本策略的核心思路是结合超级趋势指标和平均趋向指标(ADX),实现对趋势的判断和追踪。超级趋势指标用于辨别当前价格趋势方向,ADX用于判断趋势力度,只有在强势趋势下才进行交易。此外,策略还利用K线实体颜色、交易量指标等进行确认,形成比较完整的交易规则。

总体来说,该策略属于趋势追踪策略,旨在捕捉中长线明确趋势,而避免受到盘整和震荡的干扰。

策略原理

使用超级趋势指标判断价格趋势方向。当价格站上超级趋势时为多头信号,站下超级趋势时为空头信号。

使用ADX判断趋势力度。仅在ADX大于设置门槛时才产生交易信号,这样可以过滤掉盘整不明朗的时期。

K线实体颜色判断当前为上涨格局或下跌格局,与超级趋势指标进行组合,形成確認。

交易量放大作为确認信号。仅在交易量上涨时才进行建仓。

设置止损位和止盈位,以锁定利润和控制风险。

在设置的盘中时间结束前平掉所有仓位。

策略优势

追踪中长线明确趋势,避开震荡,可获得较高的盈利率。

策略参数较少,容易理解和实施。

风险控制到位,设置了止损和止盈。

利用多个指标进行确认,可减少虚假信号。

策略风险

大盘深度调整时可能遭遇较大亏损。

个股业绩变化时可能产生剧烈反转。

政策面发生重大变化的黑天鹅事件。

对应风险的解决方法:

适当调整ADX参数,确保只在强势趋势下交易。

加大止损幅度,控制单笔损失。

密切关注政策和重要事件,必要时主动止损。

策略优化方向

可以测试不同的超级趋势参数组合,选择产生信号较稳定的参数。

可以测试ADX的不同参数,确定最佳的参数组合。

可以增加其他指标进行确认,如波动率、布林带等,进一步减少假信号。

可以结合突破等策略,在趋势破裂时及时止损。

总结

本策略总体思路清晰,以超级趋势判断价格趋势方向,以ADX判断趋势力度,在强势趋势下进行趋势追踪。同时设置止损止盈来控制风险。策略参数较少,易于优化。可作为学习简单有效趋势策略的良好示例。后续可通过参数优化、信号过滤等方法进一步完善。

/*backtest

start: 2023-02-15 00:00:00

end: 2024-02-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Intraday Strategy Template

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © vikris

//@version=4

strategy("[VJ]Hulk Smash Intra", overlay=true, calc_on_every_tick = false, pyramiding=0,default_qty_type=strategy.percent_of_equity, default_qty_value=100,initial_capital=2000)

// ********** Strategy inputs - Start **********

// Used for intraday handling

// Session value should be from market start to the time you want to square-off

// your intraday strategy

// Important: The end time should be at least 2 minutes before the intraday

// square-off time set by your broker

var i_marketSession = input(title="Market session", type=input.session,

defval="0915-1455", confirm=true)

// Make inputs that set the take profit % (optional)

longProfitPerc = input(title="Long Take Profit (%)",

type=input.float, minval=0.0, step=0.1, defval=1) * 0.01

shortProfitPerc = input(title="Short Take Profit (%)",

type=input.float, minval=0.0, step=0.1, defval=1) * 0.01

// Set stop loss level with input options (optional)

longLossPerc = input(title="Long Stop Loss (%)",

type=input.float, minval=0.0, step=0.1, defval=0.5) * 0.01

shortLossPerc = input(title="Short Stop Loss (%)",

type=input.float, minval=0.0, step=0.1, defval=0.5) * 0.01

var float i_multiplier = input(title = "ST Multiplier", type = input.float,

defval = 2, step = 0.1, confirm=true)

var int i_atrPeriod = input(title = "ST ATR Period", type = input.integer,

defval = 10, confirm=true)

len = input(title="ADX Length", type=input.integer, defval=14)

th = input(title="ADX Threshold", type=input.integer, defval=20)

adxval = input(title="ADX Momemtum Value", type=input.integer, defval=25)

// ********** Strategy inputs - End **********

// ********** Supporting functions - Start **********

// A function to check whether the bar or period is in intraday session

barInSession(sess) => time(timeframe.period, sess) != 0

// ********** Supporting functions - End **********

// ********** Strategy - Start **********

[superTrend, dir] = supertrend(i_multiplier, i_atrPeriod)

colResistance = dir == 1 and dir == dir[1] ? color.new(color.red, 0) : color.new(color.red, 100)

colSupport = dir == -1 and dir == dir[1] ? color.new(color.green, 0) : color.new(color.green, 100)

// Super Trend Long/short condition

stlong = close > superTrend

stshort = close < superTrend

// Figure out take profit price

longExitPrice = strategy.position_avg_price * (1 + longProfitPerc)

shortExitPrice = strategy.position_avg_price * (1 - shortProfitPerc)

// Determine stop loss price

longStopPrice = strategy.position_avg_price * (1 - longLossPerc)

shortStopPrice = strategy.position_avg_price * (1 + shortLossPerc)

//Vol Confirmation

vol = volume > volume[1]

//Candles colors

greenCandle = (close > open)

redCandle = (close < open)

// See if intraday session is active

bool intradaySession = barInSession(i_marketSession)

// Trade only if intraday session is active

TrueRange = max(max(high - low, abs(high - nz(close[1]))), abs(low - nz(close[1])))

DirectionalMovementPlus = high - nz(high[1]) > nz(low[1]) - low ? max(high - nz(high[1]), 0) : 0

DirectionalMovementMinus = nz(low[1]) - low > high - nz(high[1]) ? max(nz(low[1]) - low, 0) : 0

SmoothedTrueRange = 0.0

SmoothedTrueRange := nz(SmoothedTrueRange[1]) - nz(SmoothedTrueRange[1]) / len + TrueRange

SmoothedDirectionalMovementPlus = 0.0

SmoothedDirectionalMovementPlus := nz(SmoothedDirectionalMovementPlus[1]) -

nz(SmoothedDirectionalMovementPlus[1]) / len + DirectionalMovementPlus

SmoothedDirectionalMovementMinus = 0.0

SmoothedDirectionalMovementMinus := nz(SmoothedDirectionalMovementMinus[1]) -

nz(SmoothedDirectionalMovementMinus[1]) / len + DirectionalMovementMinus

DIPlus = SmoothedDirectionalMovementPlus / SmoothedTrueRange * 100

DIMinus = SmoothedDirectionalMovementMinus / SmoothedTrueRange * 100

DX = abs(DIPlus - DIMinus) / (DIPlus + DIMinus) * 100

ADX = sma(DX, len)

// a = plot(DIPlus, color=color.green, title="DI+", transp=100)

// b = plot(DIMinus, color=color.red, title="DI-", transp=100)

//Final Long/Short Condition

longCondition = stlong and redCandle and vol and ADX>adxval

shortCondition = stshort and greenCandle and vol and ADX >adxval

//Long Strategy - buy condition and exits with Take profit and SL

if (longCondition and intradaySession)

stop_level = longStopPrice

profit_level = longExitPrice

strategy.entry("My Long Entry Id", strategy.long)

strategy.exit("TP/SL", "My Long Entry Id",stop=stop_level, limit=profit_level)

//Short Strategy - sell condition and exits with Take profit and SL

if (shortCondition and intradaySession)

stop_level = shortStopPrice

profit_level = shortExitPrice

strategy.entry("My Short Entry Id", strategy.short)

strategy.exit("TP/SL", "My Short Entry Id", stop=stop_level, limit=profit_level)

// Square-off position (when session is over and position is open)

squareOff = (not intradaySession) and (strategy.position_size != 0)

strategy.close_all(when = squareOff, comment = "Square-off")

// ********** Strategy - End **********