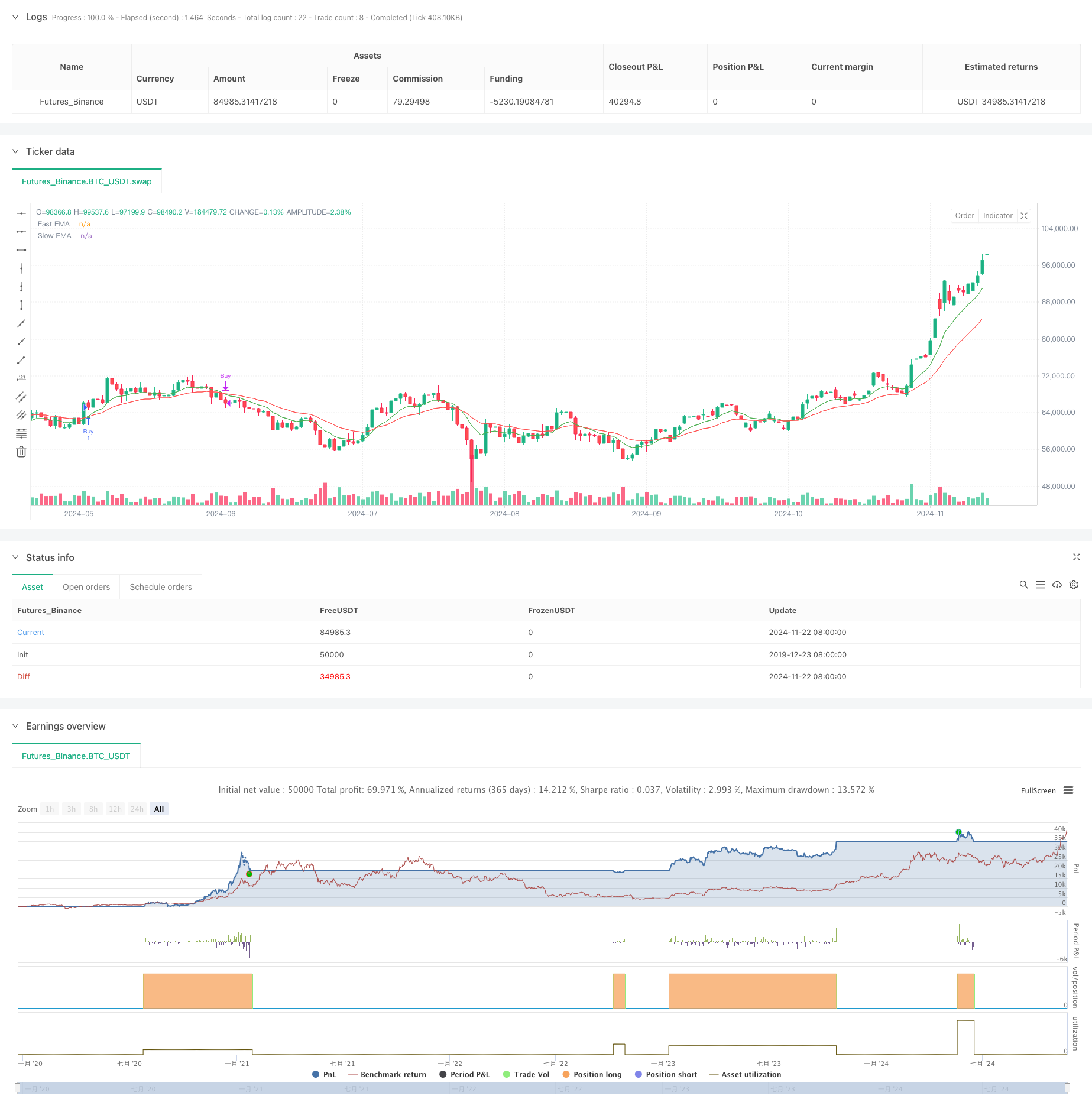

概述

该策略是一个结合了移动均线、相对强弱指标和趋势强度指标的综合交易系统。通过多重技术指标的协同配合,实现了对市场趋势的精确捕捉和风险的有效控制。系统采用了动态的止盈止损机制,确保了交易的风险收益比,同时通过指标参数的灵活调整来适应不同市场环境。

策略原理

策略主要基于三个核心指标:快速和慢速指数移动平均线(EMA)、相对强弱指标(RSI)和平均趋向指标(ADX)。当快速EMA上穿慢速EMA时,系统会检查RSI是否处于非超买区域(低于60),同时确认ADX显示趋势强度充分(大于15)。满足这些条件时,系统会发出做多信号。相反的条件组合则触发平仓信号。系统还设置了基于风险收益比的动态止盈止损点,通过参数化的方式实现对交易风险的精确控制。

策略优势

- 多重技术指标的协同确认提高了交易信号的可靠性

- 动态的止盈止损机制确保了每笔交易的风险可控

- 参数化的设计使策略具有较强的适应性

- 趋势强度确认机制有效降低了假突破带来的风险

- 系统自带警报功能,便于实时监控市场机会

策略风险

- 多重指标条件可能导致错过一些交易机会

- 在震荡市场中可能频繁产生虚假信号

- 固定的风险收益比可能不适合所有市场环境

- 参数优化过度可能导致过拟合问题

策略优化方向

- 引入自适应的参数调整机制,使系统能够根据市场波动性动态调整指标参数

- 增加成交量指标作为辅助确认信号

- 开发动态的风险收益比调整机制,根据市场环境自动调整止盈止损比例

- 加入市场波动率过滤机制,在高波动率环境下调整策略激进程度

- 考虑增加时间过滤器,避免在不利的交易时段进行操作

总结

该策略通过多重技术指标的综合运用,建立了一个相对完整的交易系统。其核心优势在于通过指标协同配合提高了交易信号的可靠性,同时通过动态的风险控制机制保障了交易的安全性。虽然存在一些固有的局限性,但通过建议的优化方向,策略仍有较大的改进空间。整体而言,这是一个具有实用价值的交易策略框架,适合进一步优化和实战应用。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-23 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Enhanced EMA + RSI + ADX Strategy (Focused on 70% Win Rate)", overlay=true)

// Input parameters

lenFast = input.int(9, title="Fast EMA Length", minval=1)

lenSlow = input.int(21, title="Slow EMA Length", minval=1)

rsiPeriod = input.int(14, title="RSI Period")

adxPeriod = input.int(14, title="ADX Period")

adxSmoothing = input.int(1, title="ADX Smoothing")

adxThreshold = input.int(15, title="ADX Threshold")

riskRewardRatio = input.float(1.5, title="Risk/Reward Ratio")

rsiOverbought = input.int(60, title="RSI Overbought Level") // Adjusted for flexibility

rsiOversold = input.int(40, title="RSI Oversold Level")

// EMA Calculations

fastEMA = ta.ema(close, lenFast)

slowEMA = ta.ema(close, lenSlow)

// RSI Calculation

rsiValue = ta.rsi(close, rsiPeriod)

// ADX Calculation

[plusDI, minusDI, adxValue] = ta.dmi(adxPeriod, adxSmoothing)

// Entry Conditions with Confirmation

buyCondition = ta.crossover(fastEMA, slowEMA) and rsiValue < rsiOverbought and adxValue > adxThreshold

sellCondition = ta.crossunder(fastEMA, slowEMA) and rsiValue > rsiOversold and adxValue > adxThreshold

// Dynamic Exit Conditions

takeProfit = strategy.position_avg_price + (close - strategy.position_avg_price) * riskRewardRatio

stopLoss = strategy.position_avg_price - (close - strategy.position_avg_price)

// Entry logic

if (buyCondition)

strategy.entry("Buy", strategy.long)

strategy.exit("Sell", from_entry="Buy", limit=takeProfit, stop=stopLoss)

if (sellCondition)

strategy.close("Buy")

// Plotting EMAs

plot(fastEMA, color=color.new(color.green, 0), title="Fast EMA", linewidth=1)

plot(slowEMA, color=color.new(color.red, 0), title="Slow EMA", linewidth=1)

// Entry and exit markers

plotshape(series=buyCondition, style=shape.triangleup, location=location.belowbar, color=color.new(color.green, 0), size=size.normal, title="Buy Signal")

plotshape(series=sellCondition, style=shape.triangledown, location=location.abovebar, color=color.new(color.red, 0), size=size.normal, title="Sell Signal")

// Alerts

alertcondition(buyCondition, title="Buy Alert", message="Buy signal triggered")

alertcondition(sellCondition, title="Sell Alert", message="Sell signal triggered")

相关推荐