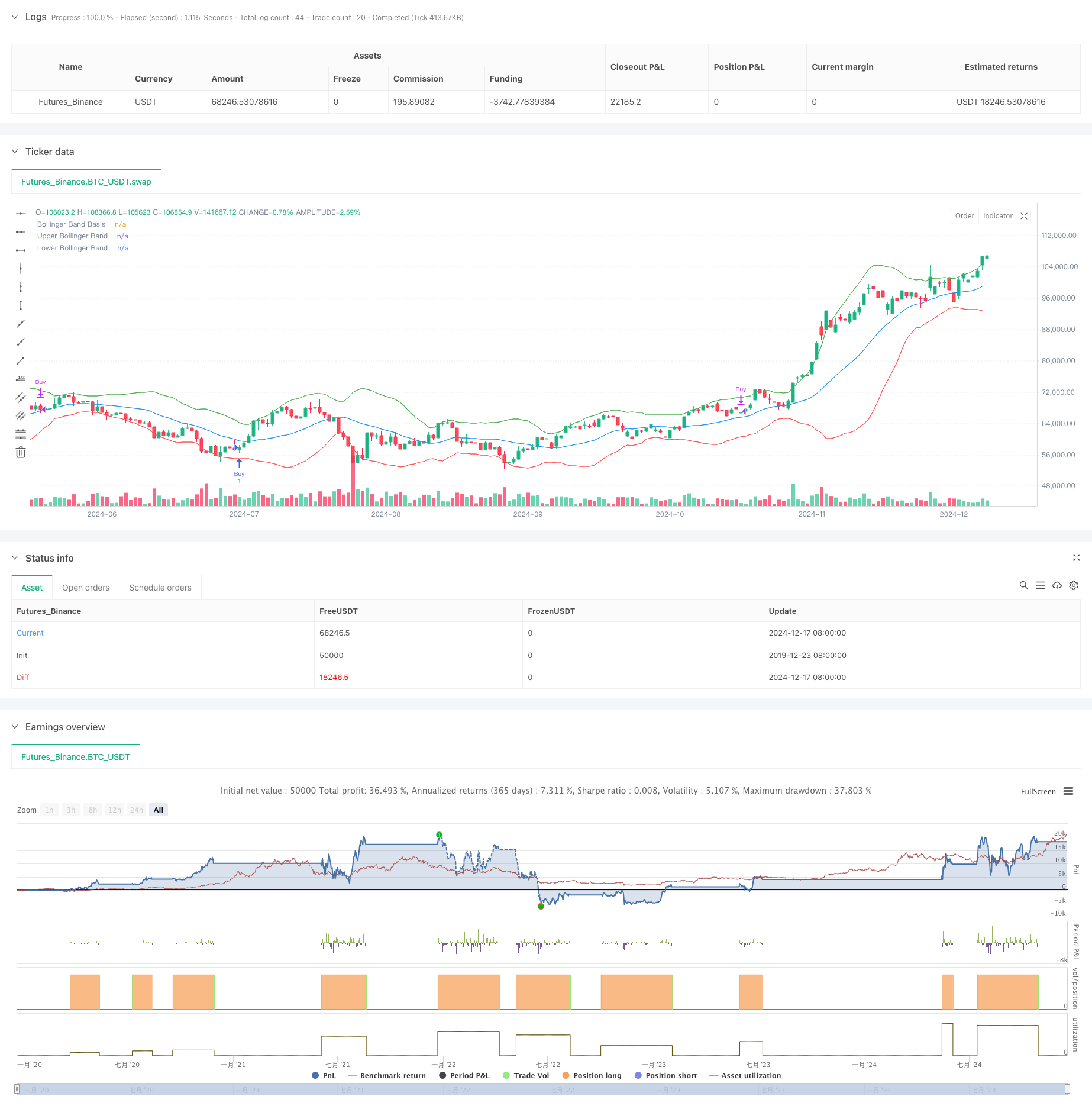

概述

该策略是一个基于MACD和RSI指标交叉信号的趋势跟踪系统,并结合布林带进行市场波动分析。策略核心是通过MACD金叉死叉与RSI超买超卖区域的配合来捕捉趋势转折点,同时利用布林带来确认价格波动区间,从而提供更稳健的交易信号。

策略原理

策略采用了三重技术指标过滤机制: 1. MACD指标(12,26,9)用于捕捉趋势动量,当MACD线从下方突破信号线时产生做多信号。 2. RSI指标(14)用于确认超买超卖状态,RSI低于50时支持做多信号。 3. 布林带(20,2)用于界定价格波动范围,并为交易决策提供参考。

入场条件要求MACD金叉且RSI处于低位(< 50),这表明市场可能从超卖区域开始反弹。 出场条件需要MACD死叉且RSI处于高位(> 50),说明上升动能减弱,可能开始回调。

策略优势

- 多重技术指标互相验证,能有效降低虚假信号。

- MACD和RSI的组合既能捕捉趋势又能识别超买超卖。

- 布林带的引入帮助判断市场波动状态,提供更好的风险控制。

- 策略逻辑清晰,参数可调整性强。

- 适合中长期趋势交易,避免频繁交易。

策略风险

- 横盘市场可能产生频繁假突破信号。

- 快速震荡市场中可能出现滞后性。

- 多重指标可能造成信号冲突。

- 固定的RSI阈值在不同市场环境下可能需要调整。

- 缺乏止损机制可能导致较大回撤。

策略优化方向

- 引入自适应的RSI阈值,根据市场波动度动态调整。

- 添加ATR止损机制,提供更好的风险控制。

- 考虑将布林带突破作为信号确认机制。

- 增加成交量指标作为辅助确认。

- 引入市场环境过滤机制,如趋势强度指标。

- 优化MACD参数,可考虑使用自适应周期。

总结

该策略通过MACD、RSI和布林带的组合应用,构建了一个相对完整的趋势跟踪交易系统。策略具有良好的理论基础和实践可行性,但仍需要根据具体市场特征进行参数优化和风险控制的改进。通过建议的优化方向,策略有望获得更好的稳定性和盈利能力。该系统适合追求中长期趋势机会的投资者,但使用时需要充分认识其局限性并做好风险管理。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2024-12-18 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("MACD, RSI, Bollinger Bands Strategy", overlay=true)

// Input parameters for MACD

fastLength = input.int(12, title="MACD Fast Length")

slowLength = input.int(26, title="MACD Slow Length")

signalLength = input.int(9, title="MACD Signal Length")

// Input parameters for RSI

rsiLength = input.int(14, title="RSI Length")

// Input parameters for Bollinger Bands

bbLength = input.int(20, title="Bollinger Band Length")

bbMult = input.float(2.0, title="Bollinger Band Multiplier")

// MACD calculation

[macdLine, signalLine, _] = ta.macd(close, fastLength, slowLength, signalLength)

macdCrossUp = ta.crossover(macdLine, signalLine)

macdCrossDown = ta.crossunder(macdLine, signalLine)

// RSI calculation

rsi = ta.rsi(close, rsiLength)

// Bollinger Bands calculation

bbBasis = ta.sma(close, bbLength)

bbUpper = bbBasis + bbMult * ta.stdev(close, bbLength)

bbLower = bbBasis - bbMult * ta.stdev(close, bbLength)

// Plot Bollinger Bands

plot(bbBasis, color=color.blue, title="Bollinger Band Basis")

plot(bbUpper, color=color.green, title="Upper Bollinger Band")

plot(bbLower, color=color.red, title="Lower Bollinger Band")

// Entry condition: MACD crosses signal line from below and RSI < 50

enterLong = macdCrossUp and rsi < 50

// Exit condition: MACD crosses signal line from above and close touches the Bollinger Band middle line

exitLong = macdCrossDown and rsi> 50

// Strategy logic

if (enterLong and strategy.position_size == 0)

strategy.entry("Buy", strategy.long)

if (exitLong and strategy.position_size > 0)

strategy.close("Buy")

相关推荐