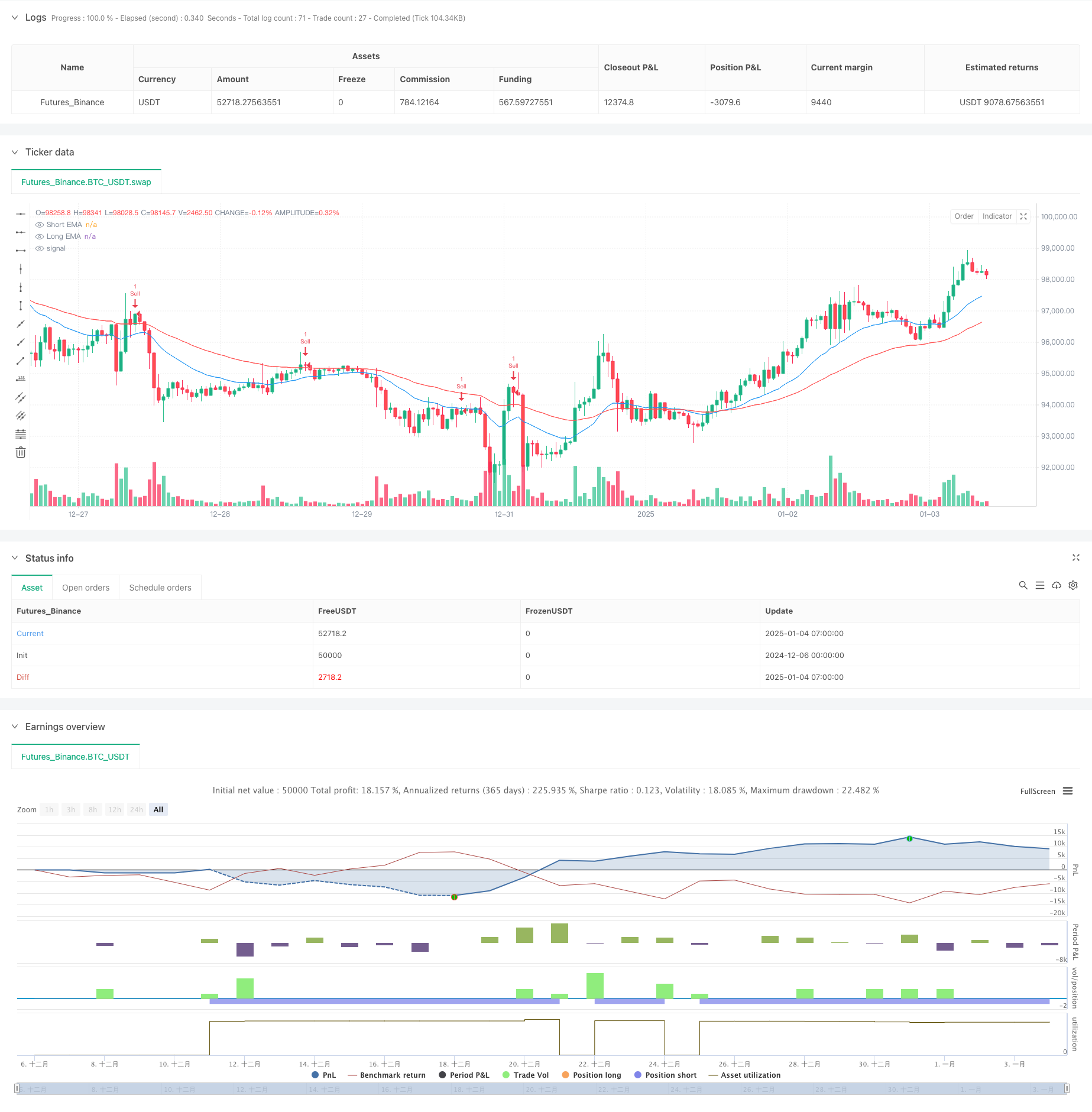

概述

该策略是一个结合了双指数移动平均线(EMA)和随机震荡指标(Stochastic Oscillator)的量化交易系统。通过20周期和50周期EMA判断市场趋势,利用随机震荡指标在超买超卖区域寻找交易机会,实现趋势与动量的完美结合。策略采用了严格的风险管理措施,包括固定的止损和利润目标设置。

策略原理

策略的核心逻辑分为三个部分:趋势判断、入场时机和风险控制。趋势判断主要依靠快速EMA(20周期)和慢速EMA(50周期)的相对位置,当快线位于慢线上方时判断为上升趋势,反之为下降趋势。入场信号由随机震荡指标的交叉确认,在超买超卖区域寻找高胜率的交易机会。风险控制采用了固定百分比止损和2倍止盈比例的设置,确保每笔交易都有明确的风险收益比。

策略优势

- 结合趋势跟踪和动量指标,能够在趋势市场中获得稳定收益

- 采用了科学的资金管理方法,通过固定风险比例来控制每笔交易的损失

- 指标参数可根据不同市场特点灵活调整

- 策略逻辑清晰,易于理解和执行

- 适用于多个时间周期的交易

策略风险

- 在震荡市场中可能产生频繁的假信号

- EMA参数的选择会影响策略表现

- 随机震荡指标的超买超卖设置需要针对具体市场调整

- 在快速波动市场中止损位可能过宽

- 需要考虑交易成本对策略收益的影响

策略优化方向

- 增加成交量指标作为辅助确认

- 引入ATR指标动态调整止损位置

- 根据市场波动率自适应调整指标参数

- 加入趋势强度过滤器减少假信号

- 开发自适应的利润目标计算方法

总结

该策略通过结合趋势和动量指标,建立了一个完整的交易系统。策略的核心优势在于其清晰的逻辑框架和严格的风险控制,但在实际应用中仍需要根据具体市场情况进行参数优化。通过持续改进和优化,策略有望在各种市场环境下都能保持稳定的表现。

策略源码

/*backtest

start: 2024-12-06 00:00:00

end: 2025-01-04 08:00:00

period: 1h

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=6

strategy("EMA + Stochastic Strategy", overlay=true)

// Inputs for EMA

emaShortLength = input.int(20, title="Short EMA Length")

emaLongLength = input.int(50, title="Long EMA Length")

// Inputs for Stochastic

stochK = input.int(14, title="Stochastic %K Length")

stochD = input.int(3, title="Stochastic %D Smoothing")

stochOverbought = input.int(85, title="Stochastic Overbought Level")

stochOversold = input.int(15, title="Stochastic Oversold Level")

// Inputs for Risk Management

riskRewardRatio = input.float(2.0, title="Risk-Reward Ratio")

stopLossPercent = input.float(1.0, title="Stop Loss (%)")

// EMA Calculation

emaShort = ta.ema(close, emaShortLength)

emaLong = ta.ema(close, emaLongLength)

// Stochastic Calculation

k = ta.stoch(high, low, close, stochK)

d = ta.sma(k, stochD)

// Trend Condition

isUptrend = emaShort > emaLong

isDowntrend = emaShort < emaLong

// Stochastic Signals

stochBuyCrossover = ta.crossover(k, d)

stochBuySignal = k < stochOversold and stochBuyCrossover

stochSellCrossunder = ta.crossunder(k, d)

stochSellSignal = k > stochOverbought and stochSellCrossunder

// Entry Signals

buySignal = isUptrend and stochBuySignal

sellSignal = isDowntrend and stochSellSignal

// Strategy Execution

if buySignal

strategy.entry("Buy", strategy.long)

stopLoss = close * (1 - stopLossPercent / 100)

takeProfit = close * (1 + stopLossPercent * riskRewardRatio / 100)

strategy.exit("Take Profit/Stop Loss", from_entry="Buy", stop=stopLoss, limit=takeProfit)

if sellSignal

strategy.entry("Sell", strategy.short)

stopLoss = close * (1 + stopLossPercent / 100)

takeProfit = close * (1 - stopLossPercent * riskRewardRatio / 100)

strategy.exit("Take Profit/Stop Loss", from_entry="Sell", stop=stopLoss, limit=takeProfit)

// Plotting

plot(emaShort, color=color.blue, title="Short EMA")

plot(emaLong, color=color.red, title="Long EMA")

相关推荐