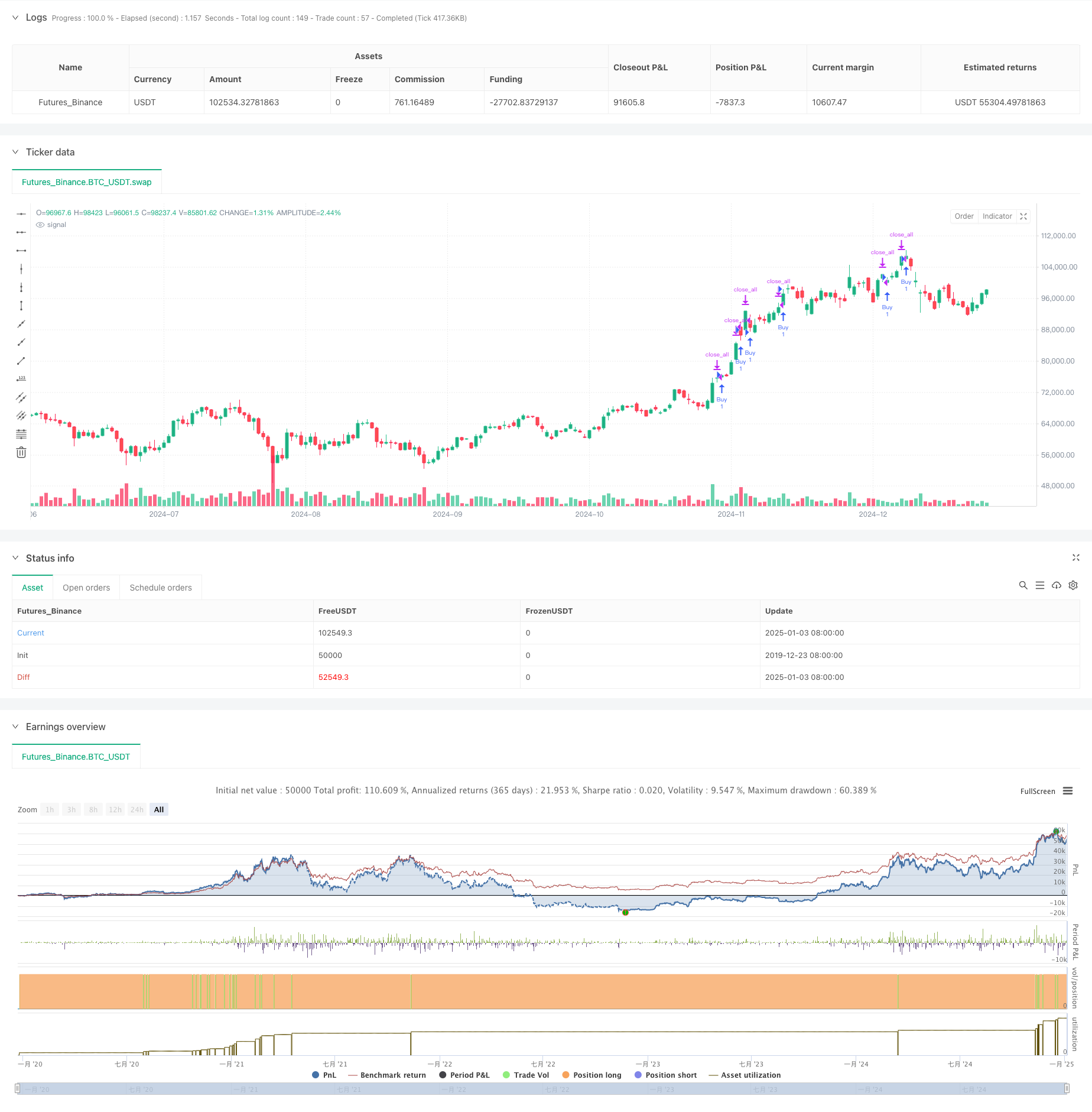

概述

该策略是一个基于价格下跌幅度进行加仓,并在达到固定盈利目标时平仓的网格交易策略。策略的核心逻辑是在市场下跌到预设幅度时进行买入,在价格反弹达到目标利润时进行整体平仓,通过不断重复这个过程来获取收益。这种策略特别适合在震荡市场中捕捉短期反弹机会。

策略原理

策略采用了网格交易和定向止盈的复合机制: 1. 初始建仓:在设定的开始时间后,系统会在第一次触发时以当前价格进行首次建仓。 2. 加仓机制:当价格相对于初始建仓价格下跌超过预设的跌幅(默认5%)时,进行追加买入。 3. 平仓机制:当价格相对于初始建仓价格上涨超过预设的盈利目标(默认5%)时,系统会对所有持仓进行平仓。 4. 统计跟踪:系统会实时统计交易次数和累计利润,并在图表上动态显示。

策略优势

- 自动化程度高:策略完全系统化,无需人工干预,能够24小时持续运行。

- 风险分散:通过分批建仓的方式,可以有效降低单次建仓的风险。

- 止盈明确:设定了固定的盈利目标,一旦达到目标立即落袋为安。

- 适应性强:通过参数调整,可以适应不同的市场环境和交易品种。

- 执行力强:策略逻辑清晰,不受主观情绪影响。

策略风险

- 趋势风险:在持续下跌行情中,可能会不断加仓导致亏损加大。

- 资金管理风险:如果不设置合理的仓位控制,可能会因过度加仓导致资金占用过大。

- 滑点风险:在行情剧烈波动时,可能会出现严重滑点,影响策略表现。

- 参数敏感性:策略效果对参数设置较为敏感,不同市场环境下需要及时调整参数。

策略优化方向

- 动态止损:建议增加基于ATR或波动率的动态止损机制,防止大幅下跌。

- 仓位管理:可以引入基于账户权益的动态仓位管理,确保资金使用更合理。

- 市场筛选:增加趋势判断指标,在趋势明显的市场中暂停策略运行。

- 盈利目标优化:可以设计动态盈利目标,根据市场波动情况自适应调整。

- 加仓优化:可以设计递进式加仓数量,避免前期过度建仓。

总结

这是一个结构简单但实用的网格交易策略,通过预设的下跌幅度进行分批建仓,在达到目标盈利时统一平仓。策略的核心优势在于其执行的确定性和风险的分散性,但在使用时需要注意市场环境的选择和参数的优化。通过增加动态止损、改进仓位管理等方式,策略还有较大的优化空间。在实盘使用时,建议先进行充分的回测,并结合市场实际情况进行参数调整。

策略源码

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Buy Down 5%, Sell at 5% Profit", overlay=true, default_qty_type=strategy.fixed, default_qty_value=1)

// Inputs

initial_date = input(timestamp("2024-01-01 00:00:00"), title="Initial Purchase Date")

profit_target = input.float(5.0, title="Profit Target (%)", minval=0.1) // Target profit percentage

rebuy_drop = input.float(5.0, title="Rebuy Drop (%)", minval=0.1) // Drop percentage to rebuy

// Variables

var float initial_price = na // Initial purchase price

var int entries = 0 // Count of entries

var float total_profit = 0 // Cumulative profit

var bool active_trade = false // Whether an active trade exists

// Entry Condition: Buy on or after the initial date

if not active_trade

initial_price := close

strategy.entry("Buy", strategy.long)

entries += 1

active_trade := true

// Rebuy Condition: Buy if price drops 5% or more from the initial price

rebuy_price = initial_price * (1 - rebuy_drop / 100)

if active_trade and close <= rebuy_price

strategy.entry("Rebuy", strategy.long)

entries += 1

// Exit Condition: Sell if the price gives a 5% profit on the initial investment

target_price = initial_price * (1 + profit_target / 100)

if active_trade and close >= target_price

strategy.close_all(comment="Profit Target Hit")

active_trade := false

total_profit += profit_target

// Display information on the chart

plotshape(series=close >= target_price, title="Target Hit", style=shape.labelup, location=location.absolute, color=color.green, text="Sell")

plotshape(series=close <= rebuy_price, title="Rebuy", style=shape.labeldown, location=location.absolute, color=color.red, text="Rebuy")

// Draw statistics on the chart

var label stats_label = na

if (na(stats_label))

stats_label := label.new(x=bar_index, y=close, text="", style=label.style_none, size=size.small)

label.set_xy(stats_label, bar_index, close)

label.set_text(stats_label, "Entries: " + str.tostring(entries) + "\nTotal Profit: " + str.tostring(total_profit, "#.##") + "%")

相关推荐