Momentum 2.0

Author: ChaoZhang, Date: 2022-05-10 10:24:44Tags: The trend

Momentum 2.0 is a normalized Momentum oscillator with a moving base-level. The oscillator value is normalized by its standard deviation, similar to the z-score technique. Instead of the zero level, the indicator uses the base-level calculated as the inverted long-term average value of the oscillator. Similar to the zero-level crossing signal used for the Momentum oscillator, our oscillator calculates the base level crossing signal. The moving base-level helps to reduce the number of false signals. In an uptrend the base-level is below zero, in a downtrend it is above it. This allows us to take into account the trend stability effect. In this case, to form a reversal signal, the oscillator must cross a lower value in an uptrend and a higher value in a downtrend.

HOW TO USE When the oscillator crosses above the base-level, it gives a bullish signal, when below it gives a bearish signal. The signals are displayed as green and red labels, respectively. The color of the histogram shows the current direction of the price momentum. Green indicates an upward move and red indicates a downward move. The blue line represents the base-level.

SETTINGS Oscillator Period - determines the period of the Momentum oscillator Base Level Period - determines the period used for long-term averaging when calculating the base-level and normalizing the oscillator

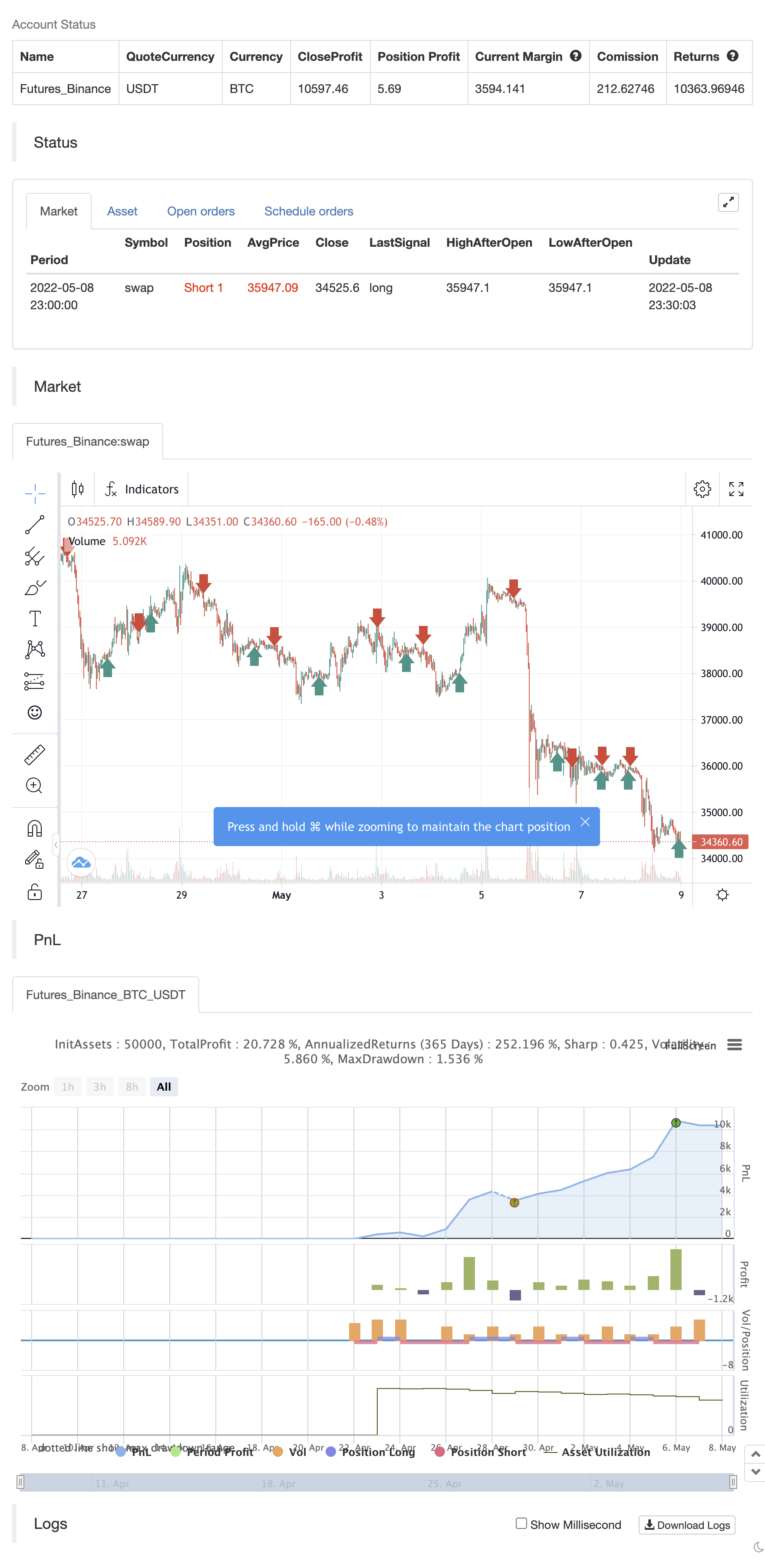

backtest

/*backtest

start: 2022-04-09 00:00:00

end: 2022-05-08 23:59:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © AstrideUnicorn

//@version=5

indicator("Momentum 2.0", overlay = false)

source = close

// Script Inputs

window = input(defval=15, title="Oscillator Period")

base_level_window = input.int(defval=450, title="Base Level Period", minval=300)

// Calculate normalized and smoothed momentum oscillator

momentum = ta.mom(source, window)

momentum_normalized = ( momentum ) / ta.stdev(momentum, base_level_window)

momentum_smoothed = ta.linreg(momentum_normalized, 30,0)

// Calculated the base-level

momentum_base = -ta.ema(momentum_normalized,base_level_window)

// Calculate base-level cross signals

bullish = ta.crossover(momentum_smoothed, momentum_base)

bearish = ta.crossunder(momentum_smoothed, momentum_base)

if bullish

strategy.entry("Enter Long", strategy.long)

else if bearish

strategy.entry("Enter Short", strategy.short)

- Linear trend

- Fibonacci Timing Pattern

- Pivot Trend

- Super trend B

- KijunSen Line With Cross

- Diamond Trend

- Heikin-Ashi Trend

- Tom DeMark Sequential Heat Map

- Demark Reversal Points

- A straight line of trends

- Hull-4ema

- Angle Attack Follow Line Indicator

- KijunSen Line With Cross

- AMACD - All Moving Average Convergence Divergence

- MA HYBRID BY RAJ

- Diamond Trend

- Nik Stoch

- stoch supertrd atr 200ma

- MTF RSI & STOCH Strategy

- EMA + AROON + ASH

- EHMA Range Strategy

- Moving Average Buy-Sell

- Midas Mk. II - Ultimate Crypto Swing

- TMA-Legacy

- TV highs and lows

- Best TradingView Strategy

- Big Snapper Alerts R3.0 + Chaiking Volatility condition + TP RSI

- Chande Kroll Stop

- CCI + EMA with RSI Cross Strategy

- EMA bands + leledc + bollinger bands trend catching strategy