Overview

The Leledec strategy identifies trend reversals by detecting exhaustion patterns in the Leledec indicator. It goes long when major Leledec exhaustion appears and goes short when minor Leledec exhaustion appears. The strategy is suitable for medium to long term trading.

Strategy Logic

The Leledec indicator identifies local extremum points of price. It does so by analyzing the relationship between close and open prices over several bars.

The core logic of the strategy is:

Calculate the major Leledec indicator (maj) using parameters bar count (maj_qual) and lookback period (maj_len).

When major Leledec breaks above maj_qual bars consecutively, and the high of the bar exceeds the highest high over the past maj_len bars, a major Leledec upside exhaustion is identified which generates a long signal.

Calculate the minor Leledec indicator (min) using parameters bar count (min_qual) and lookback period (min_len).

When minor Leledec breaks below min_qual bars consecutively, and the low of the bar is below the lowest low over the past min_len bars, a minor Leledec downside exhaustion is identified which generates a short signal.

According to the logic of the Leledec indicator, exhaustion patterns represent potential extremum points and trend reversals, hence the trading signals.

Advantage Analysis

The strategy has strong capabilities in trend identification. Leledec can effectively detect local extremum points.

Flexibility in adapting to different timeframes and market conditions through parameter tuning.

Can use major Leledec alone or incorporate minor Leledec for more comprehensive signals.

Customizable sensitivity through bar count and lookback period parameters.

Risk Analysis

Potential for false signals, requires validation using other indicators.

Parameter optimization needed for different products and timeframes. Improper parameters may cause over-trading or missed trades.

Mainly relies on candlestick patterns, may miss opportunities during short term price oscillations.

Need to watch real bodies of signal bars for failed trend reversals.

Optimization

Optimize parameter combinations for better adaptability. Consider dynamic optimization.

Incorporate other indicators like volume, moving averages etc. to filter signals.

Implement stop loss to control downside on single trades.

Incorporate short term indicators to catch opportunities from minor oscillations.

Test on different products to find optimal environment.

Optimize money management strategies like position sizing, risk per trade etc.

Conclusion

The Leledec strategy catches trend reversals by identifying extremum patterns in the Leledec indicator. It is an effective trend following methodology. While advantageous in assessing trends, further optimization, additional signal validation, and proper risk management is needed for long term profitability. Overall, the Leledec strategy provides a valuable addition to a trader’s toolkit.

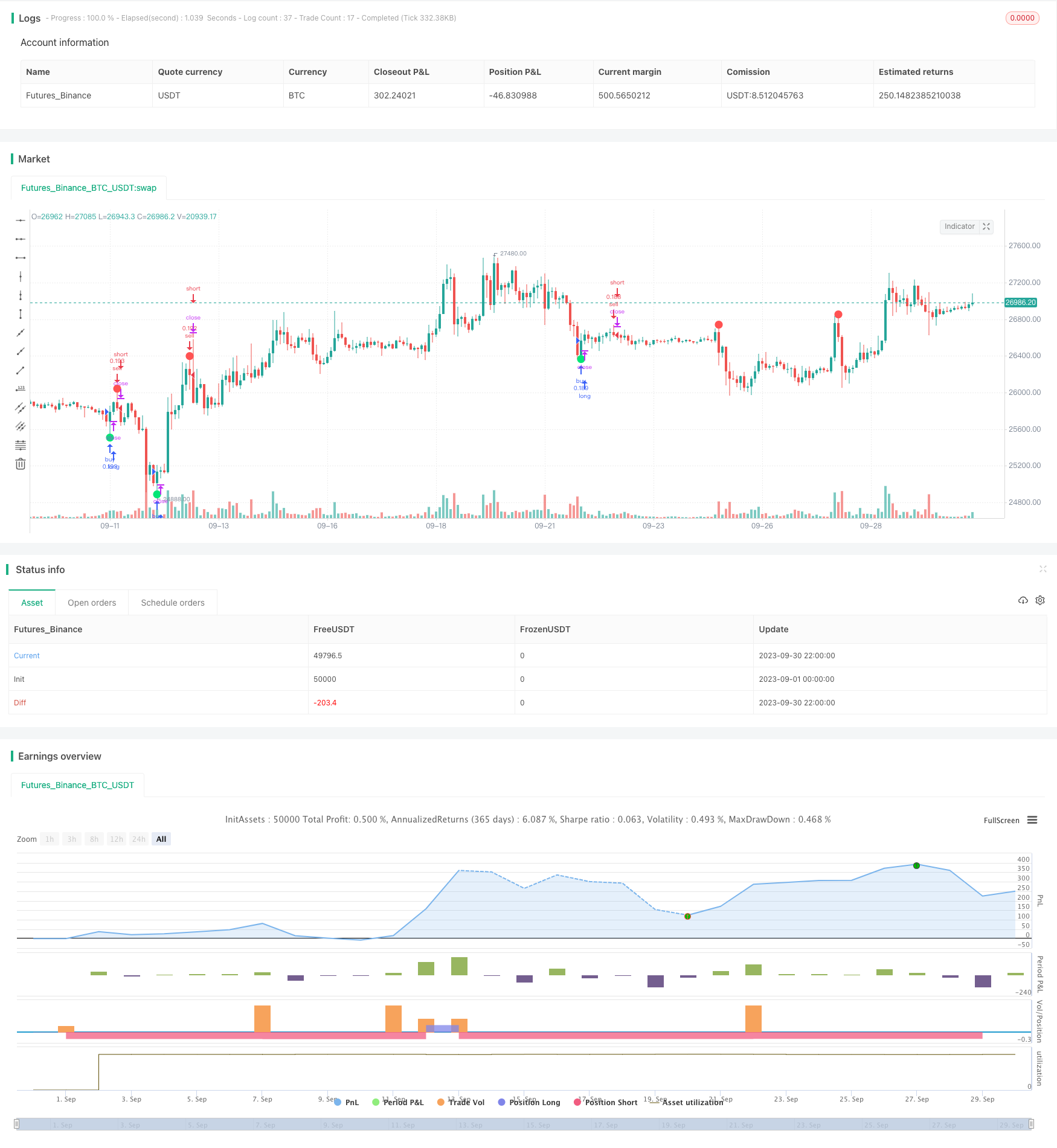

/*backtest

start: 2023-09-01 00:00:00

end: 2023-09-30 23:59:59

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Joy_Bangla

//@version=4

strategy("A Strategy for Leledec", shorttitle ="Leledec Strategy", overlay=true, commission_value=0.075, initial_capital=10000, default_qty_type = strategy.percent_of_equity, default_qty_value = 10)

maj = input(true, "Major Leledec Exhausion Bar :: Show")

min=input(false, "Minor Leledec Exhausion Bar :: Show")

leledcSrc = input(close, "Major Leledec Exhausion Bar :: Source")

maj_qual = input(6, "Major Leledec Exhausion Bar :: Bar count no")

maj_len = input(30, "Major Leledec Exhausion Bar :: Highest / Lowest")

min_qual=input(5, "Minor Leledec Exhausion Bar :: Bar count no")

min_len=input(5, "Minor Leledec Exhausion Bar :: Bar count no")

bindexSindex = input(1, "bindexSindex")

closeVal = input(4, "Close")

lele(qual, len) =>

bindex = 0

sindex = 0

bindex := nz(bindex[bindexSindex], 0)

sindex := nz(sindex[bindexSindex], 0)

ret = 0

if close > close[closeVal]

bindex := bindex + 1

bindex

if close < close[closeVal]

sindex := sindex + 1

sindex

if bindex > qual and close < open and high >= highest(high, len)

bindex := 0

ret := -1

ret

if sindex > qual and close > open and low <= lowest(low, len)

sindex := 0

ret := 1

ret

return = ret

return

major = lele(maj_qual, maj_len)

minor=lele(min_qual,min_len)

plotchar(maj ? major == -1 ? high : na : na, char='•', location=location.absolute, color=color.red, transp=0, size=size.large)

plotchar(maj ? major == 1 ? low : na : na, char='•', location=location.absolute, color=color.lime, transp=0, size=size.large)

plotchar(min ? (minor==1?high:na) : na, char='x', location=location.absolute, color=color.red, transp=0, size=size.small)

plotchar(min ? (minor==-1?low:na) : na, char='x', location=location.absolute, color=color.lime, transp=0, size=size.small)

leledecMajorBullish = major==1?low:na

leledecMajorBearish = major==-1?high:na

leledecMinorBullish = minor==1?low:na

leledecMinorBearish = minor==-1?high:na

buySignalBasedOnMajorLeledecOnly = major==1?low:na

sellSignalBasedOnMajorLeldecOnly = minor==-1?high:na

// === INPUT BACKTEST RANGE ===

fromMonth = input(defval = 1, title = "From Month", type = input.integer, minval = 1, maxval = 12)

fromDay = input(defval = 1, title = "From Day", type = input.integer, minval = 1, maxval = 31)

fromYear = input(defval = 2018, title = "From Year", type = input.integer, minval = 2017, maxval = 2030)

thruMonth = input(defval = 12, title = "Thru Month", type = input.integer, minval = 1, maxval = 11)

thruDay = input(defval = 1, title = "Thru Day", type = input.integer, minval = 1, maxval = 30)

thruYear = input(defval = 2030, title = "Thru Year", type = input.integer, minval = 2017, maxval = 2030)

// === INPUT SHOW PLOT ===

showDate = input(defval = true, title = "Show Date Range", type = input.bool)

// === FUNCTION EXAMPLE ===

start = timestamp(fromYear, fromMonth, fromDay, 00, 00) // backtest start window

finish = timestamp(thruYear, thruMonth, thruDay, 23, 59) // backtest finish window

window() => time >= start and time <= finish ? true : false // create function "within window of time"

if (window())

strategy.entry("buy", strategy.long, when=buySignalBasedOnMajorLeledecOnly)

strategy.entry("sell", strategy.short, when=sellSignalBasedOnMajorLeldecOnly)