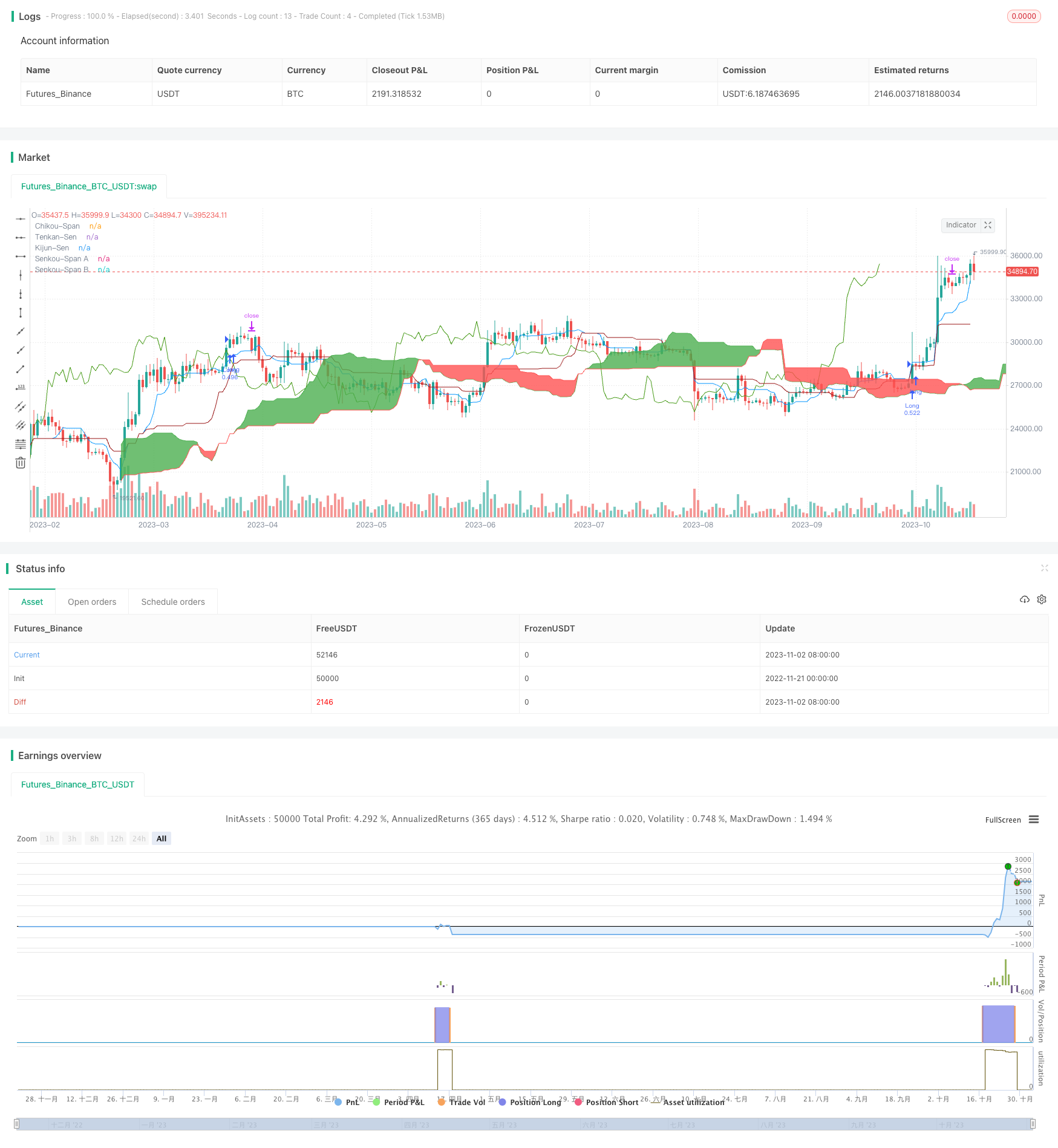

Overview

The Ichimoku Cloud and MACD Momentum Riding is a trend following strategy combining the Ichimoku Cloud indicator and the MACD momentum indicator. The strategy utilizes the Ichimoku Cloud to determine trend direction and support/resistance levels, as well as the MACD indicator to detect momentum reversal, and enters the market timed during a trend. Meanwhile, the strategy adopts a trailing stop loss to lock in profits and reduce drawdowns.

Strategy Logic

Ichimoku Cloud

The Ichimoku Cloud consists of the Turning Line (Tenkan-Sen), Base Line (Kijun-Sen), Leading Span A (Senkou-Span A), Leading Span B (Senkou-Span B) and Confirmation Line (Chikou-Span). The strategy uses the following signals to determine trend direction and support/resistance:

- Price above Cloud - Uptrend

- Price below Cloud - Downtrend

- Turning Line crosses above Base Line - Bullish signal

- Turning Line crosses below Base Line - Bearish signal

MACD Indicator

The Moving Average Convergence Divergence, or MACD, is a momentum indicator. In this strategy, when MACD’s fast line crosses above slow line it’s a buy signal, and when fast line crosses below slow line it’s a sell signal.

Entries and Exits

When Turning Line crosses above Base Line, Confirmation Line crosses above close price of 26 bars ago, close price breaks above top band of Cloud, and MACD’s fast line has bullish crossover over slow line, go long.

When price rises 3%, the strategy will move stop loss to 97% of current price to lock in profits and trail the upside move. If drawdown exceeds 3%, stop out with loss.

When Turning Line crosses below Base Line, Confirmation Line crosses below close price of 26 bars ago, close price breaks below bottom band of Cloud, and MACD’s fast line has bearish crossover below slow line, go short.

When price drops 3%, the strategy will move stop loss to 103% of current price to lock in profits and trail the downside move. If rise exceeds 3%, stop out with loss.

Advantage Analysis

This strategy combines trend identification and timing of entry, which can achieve good returns during trending markets.

Ichimoku Cloud can clearly identify trend direction. The strategy only enters aligning with Cloud direction, avoiding counter-trend trades.

MACD is effective in detecting short-term momentum reversals. Combining with Cloud it improves entry accuracy.

Trailing stop loss allows the strategy to keep running during a trend. Proper position sizing ensures controlled risk per trade.

Risk Analysis

There are also certain risks with this strategy:

Cloud needs relatively long lookback periods and may give inaccurate signals in the short term.

MACD oscillates with price and can generate false signals. More filters are needed to confirm signals.

Trailing stop loss only suits trending markets. Stop loss percentage needs to be adjusted accordingly, otherwise whipsaws may stop out too frequently during ranging markets.

The strategy itself does not manage risk. User needs to implement external risk management techniques to control losses.

Optimization Directions

The Ichimoku Cloud and MACD Momentum Riding strategy can be optimized in the following ways:

Parameter tuning - Adjust Turning Line, Base Line lookback periods, optimize MACD parameters for clearer signals.

Add filtration - Use other indicators like RSI, Bollinger Bands to filter out bad signals, reducing false signals.

Dynamic stops - Base stop loss percentage on market volatility and risk preference.

Incorporate position sizing - Limit max loss per trade to control overall drawdown.

Auto selecting contracts & rebalancing - Expand adaptability to more markets.

Conclusion

The Ichimoku Cloud and MACD Momentum Riding strategy considers both trend and timing, which can achieve good return when parameters are properly tuned and risk controls are in place. It suits investors with some programming skills as a trend following strategy, and serves as a reference to quant trading beginners for learning technical indicators and strategy development.

/*backtest

start: 2022-11-21 00:00:00

end: 2023-11-03 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy('Ichimoku Cloud with MACD and Trailing Stop Loss',

overlay=true,

initial_capital=1000,

process_orders_on_close=true,

default_qty_type=strategy.percent_of_equity,

default_qty_value=30,

commission_type=strategy.commission.percent,

commission_value=0.1)

showDate = input(defval=true, title='Show Date Range')

timePeriod = time >= timestamp(syminfo.timezone, 2022, 6, 1, 0, 0)

// Inputs

ts_bars = input.int(9, minval=1, title='Tenkan-Sen Bars')

ks_bars = input.int(26, minval=1, title='Kijun-Sen Bars')

ssb_bars = input.int(52, minval=1, title='Senkou-Span B Bars')

cs_offset = input.int(26, minval=1, title='Chikou-Span Offset')

ss_offset = input.int(26, minval=1, title='Senkou-Span Offset')

long_entry = input(true, title='Long Entry')

short_entry = input(true, title='Short Entry')

middle(len) => math.avg(ta.lowest(len), ta.highest(len))

// Ichimoku Components

tenkan = middle(ts_bars)

kijun = middle(ks_bars)

senkouA = math.avg(tenkan, kijun)

senkouB = middle(ssb_bars)

// Plot Ichimoku Kinko Hyo

plot(tenkan, color=color.new(#0496ff, 0), title='Tenkan-Sen')

plot(kijun, color=color.new(#991515, 0), title='Kijun-Sen')

plot(close, offset=-cs_offset + 1, color=color.new(#459915, 0), title='Chikou-Span')

sa = plot(senkouA, offset=ss_offset - 1, color=color.new(color.green, 0), title='Senkou-Span A')

sb = plot(senkouB, offset=ss_offset - 1, color=color.new(color.red, 0), title='Senkou-Span B')

fill(sa, sb, color=senkouA > senkouB ? color.green : color.red, title='Cloud color', transp=90)

ss_high = math.max(senkouA[ss_offset - 1], senkouB[ss_offset - 1])

ss_low = math.min(senkouA[ss_offset - 1], senkouB[ss_offset - 1])

// MACD

[macd, macd_signal, macd_histogram] = ta.macd(close, 12, 26, 9)

// Entry/Exit Signals

tk_cross_bull = tenkan > kijun

tk_cross_bear = tenkan < kijun

cs_cross_bull = ta.mom(close, cs_offset - 1) > 0

cs_cross_bear = ta.mom(close, cs_offset - 1) < 0

price_above_kumo = close > ss_high

price_below_kumo = close < ss_low

bullish = tk_cross_bull and cs_cross_bull and price_above_kumo and ta.crossover(macd, macd_signal)

bearish = tk_cross_bear and cs_cross_bear and price_below_kumo and ta.crossunder(macd, macd_signal)

// Configure trail stop level with input options

longTrailPerc = input.float(title='Trail Long Loss (%)', minval=0.0, step=0.1, defval=3) * 0.01

shortTrailPerc = input.float(title='Trail Short Loss (%)', minval=0.0, step=0.1, defval=3) * 0.01

// Determine trail stop loss prices

longStopPrice = 0.0

shortStopPrice = 0.0

longStopPrice := if strategy.position_size > 0

stopValue = close * (1 - longTrailPerc)

math.max(stopValue, longStopPrice[1])

else

0

shortStopPrice := if strategy.position_size < 0

stopValue = close * (1 + shortTrailPerc)

math.min(stopValue, shortStopPrice[1])

else

999999

strategy.entry('Long', strategy.long, when=bullish and long_entry and timePeriod)

strategy.exit('Exit', stop = longStopPrice, limit = shortStopPrice)

//strategy.close('Long', when=bearish and not short_entry)

//strategy.entry('Short', strategy.short, when=bearish and short_entry and timePeriod)

//strategy.close('Short', when=bullish and not long_entry)