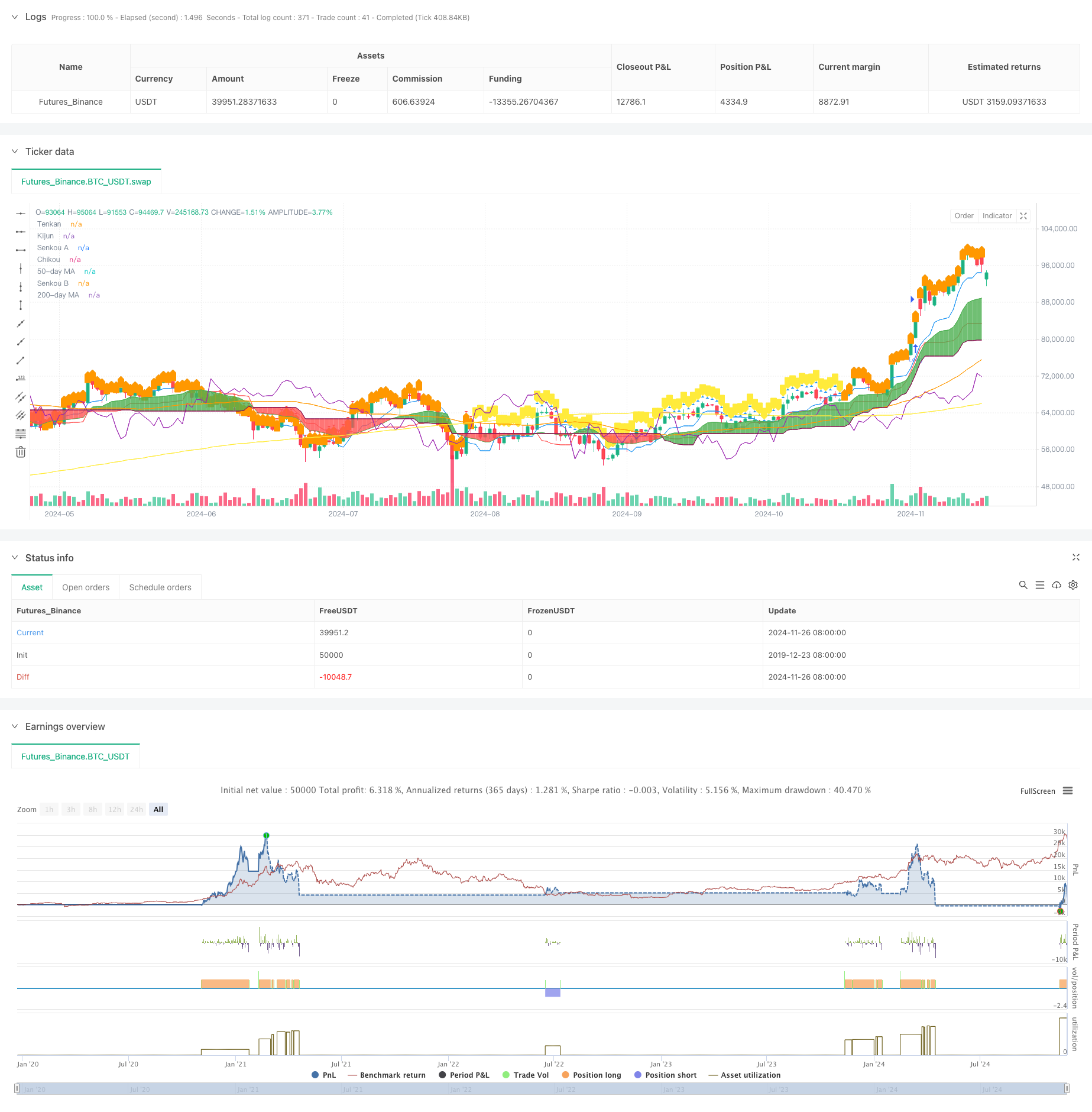

Descripción general

La estrategia es un sistema de negociación completo que combina una serie de indicadores técnicos para tomar decisiones de negociación basadas principalmente en los indicadores de la nube a primera vista. El sistema determina el momento de entrada a través de la intersección de la antena Tenkan con la línea de referencia Kijun, mientras que combina el índice RSI y la media móvil como condiciones de filtración auxiliares. La estrategia utiliza el componente de la nube como punto de parada dinámico para formar un sistema completo de control de riesgo.

Principio de estrategia

La lógica central de la estrategia se basa en los siguientes elementos clave:

- La señal de entrada es generada por la intersección de la antena con la línea de referencia, formando una señal múltiple y una señal de vacío.

- La relación de la posición del precio con respecto a la nube (Kumo) como confirmación de tendencia, el precio hace más por encima de la nube, el precio hace menos por debajo de la nube

- La relación de posición entre las medias móviles de 50 y 200 días como condición de filtro de tendencia

- El indicador RSI en el círculo sirve como confirmación de la fortaleza del mercado y filtra las falsas señales

- Utiliza el límite superior y inferior de la nube como una posición de parada dinámica para lograr la gestión dinámica del riesgo

Ventajas estratégicas

- La combinación de múltiples indicadores técnicos proporciona señales de negociación más fiables y reduce significativamente el impacto de las falsas señales

- El uso de gráficos en la nube como un punto de parada dinámico, que puede ajustar automáticamente la posición de parada en función de las fluctuaciones del mercado, tanto para proteger las ganancias y dar suficiente espacio para los precios de fluctuación

- El filtro del RSI en la curva evita las operaciones desfavorables en las zonas de sobrecompra y sobreventa

- El cruce de las medias móviles proporciona confirmación de tendencias adicionales y mejora la tasa de éxito de las operaciones

- Sistema completo de control de riesgos, incluidos todos los aspectos de la entrada, la tenencia y la salida

Riesgo estratégico

- El filtrado de múltiples indicadores puede hacer que se pierdan oportunidades potenciales

- En un mercado volátil pueden producirse frecuentes señales de ruptura falsas

- El índice de gráficos en la nube tiene un cierto retraso que puede afectar el tiempo de entrada

- En un mercado con rápidas fluctuaciones, el stop loss dinámico puede ser demasiado relajado

- El exceso de condiciones de filtración puede reducir las oportunidades de negociación y afectar los beneficios generales de la estrategia.

Dirección de optimización de la estrategia

- Introducción de un indicador de volatilidad para ajustar los parámetros de la estrategia a las fluctuaciones del mercado

- Optimización de la configuración de los parámetros de los diagramas de la nube para adaptarlos mejor a diferentes entornos de mercado

- Aumentar el análisis de volumen de transacciones y mejorar la fiabilidad de las señales

- Introducción de un mecanismo de filtro de tiempo para evitar períodos de gran fluctuación

- Desarrollar sistemas de optimización de parámetros adaptativos para el ajuste dinámico de la estrategia

Resumir

La estrategia combina varios indicadores técnicos para construir un sistema de negociación completo. La estrategia no solo se centra en la generación de señales, sino que también incluye un mecanismo de control de riesgo completo.

/*backtest

start: 2019-12-23 08:00:00

end: 2024-11-27 00:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Ichimoku Strategy with Optional RSI, MA Filters and Alerts", overlay=true)

// Input for date and time filter

startDate = input(timestamp("2020-01-01 00:00"), title="Start Date")

endDate = input(timestamp("2023-01-01 00:00"), title="End Date")

// Inputs for Ichimoku settings

tenkanPeriod = input.int(9, title="Tenkan Period")

kijunPeriod = input.int(26, title="Kijun Period")

senkouBPeriod = input.int(52, title="Senkou B Period")

// Inputs for Moving Average settings

useMAFilter = input.bool(true, title="Enable Moving Average Filter?")

ma50Period = input.int(50, title="50-day MA Period")

ma200Period = input.int(200, title="200-day MA Period")

// Inputs for RSI settings

useRSIFilter = input.bool(true, title="Enable RSI Filter?")

rsiPeriod = input.int(14, title="RSI Period")

rsiOverbought = input.int(70, title="RSI Overbought Level")

rsiOversold = input.int(30, title="RSI Oversold Level")

// Ichimoku Cloud components

tenkan = (ta.highest(high, tenkanPeriod) + ta.lowest(low, tenkanPeriod)) / 2

kijun = (ta.highest(high, kijunPeriod) + ta.lowest(low, kijunPeriod)) / 2

senkouA = ta.sma(tenkan + kijun, 2) / 2

senkouB = (ta.highest(high, senkouBPeriod) + ta.lowest(low, senkouBPeriod)) / 2

chikou = close[26]

// Moving Averages

ma50 = ta.sma(close, ma50Period)

ma200 = ta.sma(close, ma200Period)

// Weekly RSI

rsiSource = request.security(syminfo.tickerid, "W", ta.rsi(close, rsiPeriod))

// Plotting the Ichimoku Cloud components

pTenkan = plot(tenkan, color=color.blue, title="Tenkan")

pKijun = plot(kijun, color=color.red, title="Kijun")

pSenkouA = plot(senkouA, color=color.green, title="Senkou A")

pSenkouB = plot(senkouB, color=color.maroon, title="Senkou B")

plot(chikou, color=color.purple, title="Chikou")

plot(ma50, color=color.orange, title="50-day MA")

plot(ma200, color=color.yellow, title="200-day MA")

// Corrected fill function

fill(pSenkouA, pSenkouB, color=senkouA > senkouB ? color.green : color.red, transp=90)

// Debugging: Output values on the chart to see if conditions are ever met

plotshape(series=(tenkan > kijun), color=color.blue, style=shape.triangleup, title="Tenkan > Kijun")

plotshape(series=(tenkan < kijun), color=color.red, style=shape.triangledown, title="Tenkan < Kijun")

plotshape(series=(ma50 > ma200), color=color.orange, style=shape.labelup, title="MA 50 > MA 200")

plotshape(series=(ma50 < ma200), color=color.yellow, style=shape.labeldown, title="MA 50 < MA 200")

// Define the trailing stop loss using Kumo

var float trailingStopLoss = na

// Check for MA conditions (apply only if enabled)

maConditionLong = not useMAFilter or (useMAFilter and ma50 > ma200)

maConditionShort = not useMAFilter or (useMAFilter and ma50 < ma200)

// Check for Ichimoku Cloud conditions

ichimokuLongCondition = close > math.max(senkouA, senkouB)

ichimokuShortCondition = close < math.min(senkouA, senkouB)

// Check for RSI conditions (apply only if enabled)

rsiConditionLong = not useRSIFilter or (useRSIFilter and rsiSource > rsiOverbought)

rsiConditionShort = not useRSIFilter or (useRSIFilter and rsiSource < rsiOversold)

// Combine conditions for entry

longCondition = maConditionLong and tenkan > kijun and ichimokuLongCondition and rsiConditionLong

shortCondition = maConditionShort and tenkan < kijun and ichimokuShortCondition and rsiConditionShort

// Date and time filter

withinDateRange = true

// Check for Long Condition

if (longCondition and withinDateRange)

strategy.entry("Long", strategy.long)

trailingStopLoss := math.min(senkouA, senkouB)

alert("Buy Signal: Entering Long Position", alert.freq_once_per_bar_close)

// Check for Short Condition

if (shortCondition and withinDateRange)

strategy.entry("Short", strategy.short)

trailingStopLoss := math.max(senkouA, senkouB)

alert("Sell Signal: Entering Short Position", alert.freq_once_per_bar_close)

// Exit conditions

exitLongCondition = close < kijun or tenkan < kijun

exitShortCondition = close > kijun or tenkan > kijun

if (exitLongCondition and strategy.position_size > 0)

strategy.close("Long")

alert("Exit Signal: Closing Long Position", alert.freq_once_per_bar_close)

if (exitShortCondition and strategy.position_size < 0)

strategy.close("Short")

alert("Exit Signal: Closing Short Position", alert.freq_once_per_bar_close)

// Apply trailing stop loss

if (strategy.position_size > 0)

strategy.exit("Trailing Stop Long", stop=trailingStopLoss)

else if (strategy.position_size < 0)

strategy.exit("Trailing Stop Short", stop=trailingStopLoss)