Mengajarkan Anda untuk menulis fungsi sintesis K-line dalam versi Python

Penulis:FMZ~Lydia, Dibuat: 2022-12-26 09:28:58, Diperbarui: 2024-12-15 16:36:45

Mengajarkan Anda untuk menulis fungsi sintesis K-line dalam versi Python

Ketika menulis dan menggunakan strategi, kita sering menggunakan beberapa data periode K-line yang jarang digunakan. Namun, pertukaran dan sumber data tidak memberikan data tentang periode ini. Hal ini hanya dapat disintesis dengan menggunakan data dengan periode yang ada. Algoritma yang disintesis sudah memiliki versi JavaScript (linkPada kenyataannya, mudah untuk mentransplantasikan sepotong kode JavaScript ke Python. Selanjutnya, mari kita tulis versi Python dari algoritma sintesis K-line.

Versi JavaScript

function GetNewCycleRecords (sourceRecords, targetCycle) { // K-line synthesis function

var ret = []

// Obtain the period of the source K-line data first

if (!sourceRecords || sourceRecords.length < 2) {

return null

}

var sourceLen = sourceRecords.length

var sourceCycle = sourceRecords[sourceLen - 1].Time - sourceRecords[sourceLen - 2].Time

if (targetCycle % sourceCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

throw "targetCycle is not an integral multiple of sourceCycle."

}

if ((1000 * 60 * 60) % targetCycle != 0 && (1000 * 60 * 60 * 24) % targetCycle != 0) {

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

throw "targetCycle cannot complete the cycle."

}

var multiple = targetCycle / sourceCycle

var isBegin = false

var count = 0

var high = 0

var low = 0

var open = 0

var close = 0

var time = 0

var vol = 0

for (var i = 0 ; i < sourceLen ; i++) {

// Get the time zone offset value

var d = new Date()

var n = d.getTimezoneOffset()

if (((1000 * 60 * 60 * 24) - sourceRecords[i].Time % (1000 * 60 * 60 * 24) + (n * 1000 * 60)) % targetCycle == 0) {

isBegin = true

}

if (isBegin) {

if (count == 0) {

high = sourceRecords[i].High

low = sourceRecords[i].Low

open = sourceRecords[i].Open

close = sourceRecords[i].Close

time = sourceRecords[i].Time

vol = sourceRecords[i].Volume

count++

} else if (count < multiple) {

high = Math.max(high, sourceRecords[i].High)

low = Math.min(low, sourceRecords[i].Low)

close = sourceRecords[i].Close

vol += sourceRecords[i].Volume

count++

}

if (count == multiple || i == sourceLen - 1) {

ret.push({

High : high,

Low : low,

Open : open,

Close : close,

Time : time,

Volume : vol,

})

count = 0

}

}

}

return ret

}

Ada algoritma JavaScript. Python dapat diterjemahkan dan ditransplantasikan baris demi baris. Jika Anda menemukan fungsi built-in JavaScript atau metode inheren, Anda dapat pergi ke Python untuk menemukan metode yang sesuai. Oleh karena itu, migrasi mudah.

Logika algoritma adalah persis sama, kecuali bahwa panggilan fungsi JavaScriptvar n=d.getTimezoneOffset()Saat bermigrasi ke Python,n=time.altzonePerbedaan lain hanya dalam hal tata bahasa bahasa (seperti penggunaan for loop, nilai Boolean, logical AND, logical NOT, logical OR, dll.).

Migrasi kode Python:

import time

def GetNewCycleRecords(sourceRecords, targetCycle):

ret = []

# Obtain the period of the source K-line data first

if not sourceRecords or len(sourceRecords) < 2 :

return None

sourceLen = len(sourceRecords)

sourceCycle = sourceRecords[-1]["Time"] - sourceRecords[-2]["Time"]

if targetCycle % sourceCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

raise "targetCycle is not an integral multiple of sourceCycle."

if (1000 * 60 * 60) % targetCycle != 0 and (1000 * 60 * 60 * 24) % targetCycle != 0 :

Log("targetCycle:", targetCycle)

Log("sourceCycle:", sourceCycle)

Log((1000 * 60 * 60) % targetCycle, (1000 * 60 * 60 * 24) % targetCycle)

raise "targetCycle cannot complete the cycle."

multiple = targetCycle / sourceCycle

isBegin = False

count = 0

barHigh = 0

barLow = 0

barOpen = 0

barClose = 0

barTime = 0

barVol = 0

for i in range(sourceLen) :

# Get the time zone offset value

n = time.altzone

if ((1000 * 60 * 60 * 24) - (sourceRecords[i]["Time"] * 1000) % (1000 * 60 * 60 * 24) + (n * 1000)) % targetCycle == 0 :

isBegin = True

if isBegin :

if count == 0 :

barHigh = sourceRecords[i]["High"]

barLow = sourceRecords[i]["Low"]

barOpen = sourceRecords[i]["Open"]

barClose = sourceRecords[i]["Close"]

barTime = sourceRecords[i]["Time"]

barVol = sourceRecords[i]["Volume"]

count += 1

elif count < multiple :

barHigh = max(barHigh, sourceRecords[i]["High"])

barLow = min(barLow, sourceRecords[i]["Low"])

barClose = sourceRecords[i]["Close"]

barVol += sourceRecords[i]["Volume"]

count += 1

if count == multiple or i == sourceLen - 1 :

ret.append({

"High" : barHigh,

"Low" : barLow,

"Open" : barOpen,

"Close" : barClose,

"Time" : barTime,

"Volume" : barVol,

})

count = 0

return ret

# Test

def main():

while True:

r = exchange.GetRecords()

r2 = GetNewCycleRecords(r, 1000 * 60 * 60 * 4)

ext.PlotRecords(r2, "r2")

Sleep(1000)

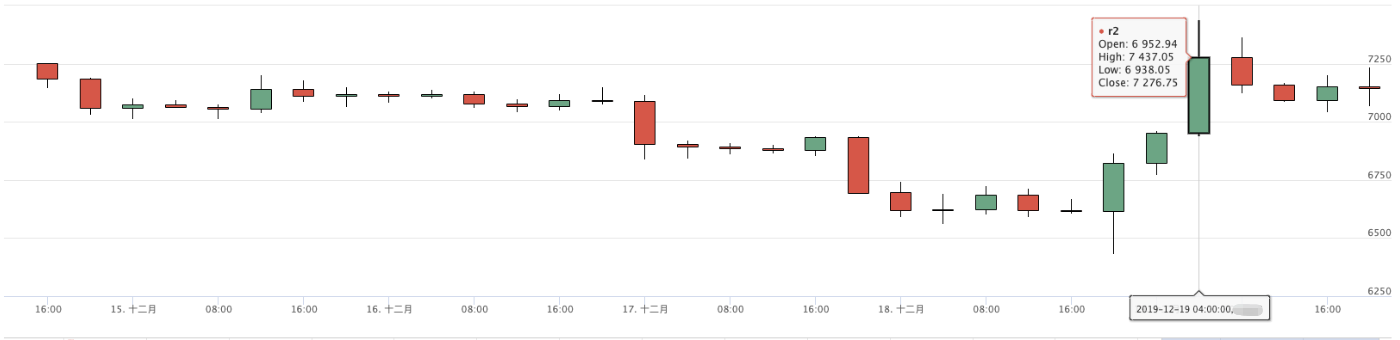

Tes

Grafik pasar Huobi

Bagan 4 jam sintesis backtest

Kode di atas hanya untuk referensi. Jika digunakan dalam strategi khusus, silahkan modifikasi dan uji sesuai dengan persyaratan khusus. Jika ada bug atau saran perbaikan, silakan tinggalkan pesan. Terima kasih banyak. o^_^ o

- Pengantar ke Lead-Lag Arbitrage dalam Cryptocurrency (2)

- Penjelasan tentang suite Lead-Lag dalam mata uang digital (2)

- Pembahasan Penerimaan Sinyal Eksternal Platform FMZ: Solusi Lengkap untuk Penerimaan Sinyal dengan Layanan Http Terbina dalam Strategi

- FMZ platform eksplorasi penerimaan sinyal eksternal: strategi built-in https layanan solusi lengkap untuk penerimaan sinyal

- Pengantar ke Lead-Lag Arbitrage dalam Cryptocurrency (1)

- Penjelasan tentang suite Lead-Lag dalam mata uang digital (1)

- Diskusi tentang Penerimaan Sinyal Eksternal dari Platform FMZ: API Terluas VS Strategi Layanan HTTP Terintegrasi

- FMZ Platform Eksternal Signal Reception: Extension API vs Strategi Layanan HTTP Terbentuk

- Diskusi tentang Metode Pengujian Strategi Berdasarkan Generator Random Ticker

- Metode pengujian strategi berdasarkan generator pasar acak

- Fitur Baru FMZ Quant: Gunakan Fungsi _Serve untuk Membuat Layanan HTTP dengan Mudah

- Perdagangan pasangan berdasarkan teknologi berbasis data

- Aplikasi Teknologi Pembelajaran Mesin dalam Perdagangan

- Menggunakan lingkungan penelitian untuk menganalisis rincian lindung nilai segitiga dan dampak biaya penanganan pada perbedaan harga lindung nilai

- Reformasi Deribit API berjangka untuk beradaptasi dengan perdagangan kuantitatif opsi

- Alat yang lebih baik membuat pekerjaan yang baik - belajar menggunakan lingkungan penelitian untuk menganalisis prinsip perdagangan

- Strategi lindung nilai lintas mata uang dalam perdagangan kuantitatif aset blockchain

- Dapatkan panduan strategi mata uang digital FMex di FMZ Quant

- Mengajarkan Anda untuk menulis strategi -- transplantasi strategi MyLanguage (Advanced)

- Mengajarkan Anda untuk menulis strategi -- menanam strategi MyLanguage

- Mengajarkan Anda untuk menambahkan dukungan multi-chart untuk strategi

- Analisis Strategi Saluran Donchian dalam Lingkungan Penelitian

- Ketika FMZ menemukan ChatGPT, ingatlah percobaan menggunakan AI untuk membantu belajar transaksi kuantitatif

- Alat perdagangan kuantitatif untuk opsi mata uang digital

- Strategi grid sederhana dalam versi Python

- Strategi aliran pesanan yang menunggu linier yang dikembangkan berdasarkan fungsi pemutaran data

- Strategi untuk membeli pemenang versi Python

- Perjalanan FMZ -- dengan Strategi Transisi

- Mengajarkan Anda untuk mengubah strategi Python satu spesies menjadi strategi multi spesies

- Mengimplementasikan robot perdagangan kuantitatif dimulai atau berhenti waktu gadget dengan menggunakan Python

- Oak mengajarkan Anda untuk menggunakan JS untuk antarmuka dengan FMZ diperluas API