FMZ Quant: 암호화폐 시장에서 공통 요구 사항 디자인 예의 분석 (I)

저자:FMZ~리디아, 창작: 2023-12-19 16:02:58, 업데이트: 2024-11-06 21:19:16

암호화폐 자산 거래 공간에서 시장 데이터를 얻고 분석하고, 쿼리율을 조사하고, 계정 자산 움직임을 모니터링하는 것은 모두 중요한 작업입니다. 아래는 몇 가지 일반적인 요구 사항에 대한 구현의 코드 예입니다.

1. 바이낸스 스팟에서 4시간 동안 가장 높은 상승률을 보이는 화폐를 얻는 코드를 어떻게 작성해야 할까요?

FMZ 플랫폼에서 양적 거래 전략 프로그램을 작성할 때, 요구 사항에 직면했을 때 가장 먼저 해야 할 일은 그것을 분석하는 것입니다. 그래서 요구 사항에 따라 우리는 다음과 같은 내용을 분석했습니다:

- 어떤 프로그래밍 언어를 사용해야 할까요? 자바스크립트를 사용하여 구현할 계획입니다.

- 모든 통화에서 실시간 스팟 코팅을 요구합니다.

요구사항을 봤을 때 첫 번째로 한 일은 Binance API 문서를 검색해서 집계된 코트가 있는지 확인하는 것이었습니다. 집계된 코트가 있는 것이 좋습니다. 하나씩 검색하는 것은 많은 작업입니다.

우리는 집계된 인용구 인터페이스를 찾았습니다.

GET https://api.binance.com/api/v3/ticker/price- 그래요 FMZ 플랫폼에서,HttpQuery교환 틱어 인터페이스 (서명 없이 공개된 인터페이스) 를 액세스하는 기능 - 4시간의 롤링 윈도우 기간 동안 데이터를 계산해야 합니다. 통계 프로그램의 구조를 설계하는 방법을 개념화하십시오.

- 가격 변동을 계산하고 분류

가격 변동 알고리즘을 생각해보면,

price fluctuations (%) = (current price - initial price) / initial price * 100%

문제를 해결하고 프로그램을 정의한 후 우리는 프로그램을 설계하는 일을 시작했습니다.

코드 설계

var dictSymbolsPrice = {}

function main() {

while (true) {

// GET https://api.binance.com/api/v3/ticker/price

try {

var arr = JSON.parse(HttpQuery("https://api.binance.com/api/v3/ticker/price"))

if (!Array.isArray(arr)) {

Sleep(5000)

continue

}

var ts = new Date().getTime()

for (var i = 0; i < arr.length; i++) {

var symbolPriceInfo = arr[i]

var symbol = symbolPriceInfo.symbol

var price = symbolPriceInfo.price

if (typeof(dictSymbolsPrice[symbol]) == "undefined") {

dictSymbolsPrice[symbol] = {name: symbol, data: []}

}

dictSymbolsPrice[symbol].data.push({ts: ts, price: price})

}

} catch(e) {

Log("e.name:", e.name, "e.stack:", e.stack, "e.message:", e.message)

}

// Calculate price fluctuations

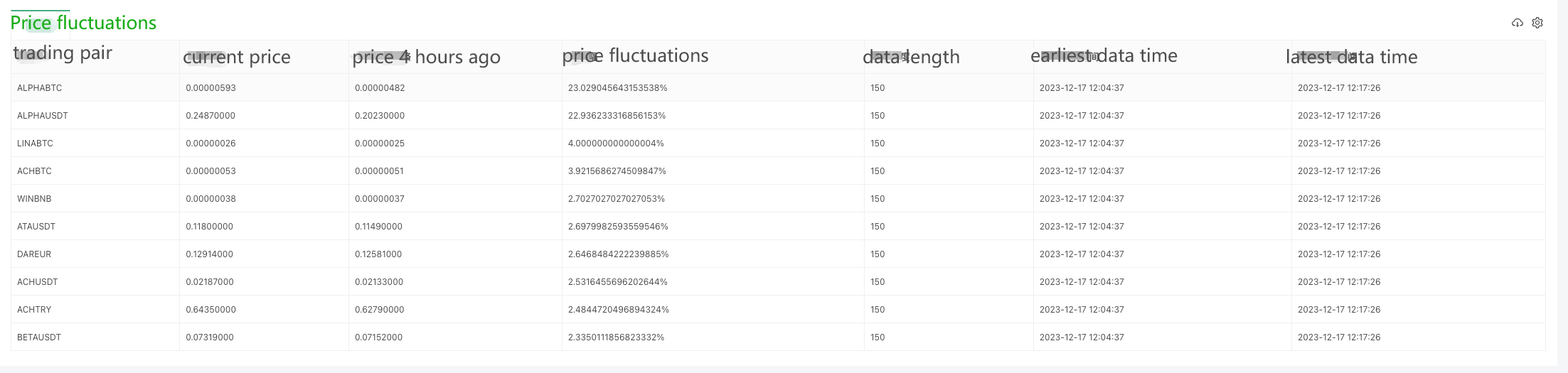

var tbl = {

type : "table",

title : "Price fluctuations",

cols : ["trading pair", "current price", "price 4 hours ago", "price fluctuations", "data length", "earliest data time", "latest data time"],

rows : []

}

for (var symbol in dictSymbolsPrice) {

var data = dictSymbolsPrice[symbol].data

if (data[data.length - 1].ts - data[0].ts > 1000 * 60 * 60 * 4) {

dictSymbolsPrice[symbol].data.shift()

}

data = dictSymbolsPrice[symbol].data

dictSymbolsPrice[symbol].percentageChange = (data[data.length - 1].price - data[0].price) / data[0].price * 100

}

var entries = Object.entries(dictSymbolsPrice)

entries.sort((a, b) => b[1].percentageChange - a[1].percentageChange)

for (var i = 0; i < entries.length; i++) {

if (i > 9) {

break

}

var name = entries[i][1].name

var data = entries[i][1].data

var percentageChange = entries[i][1].percentageChange

var currPrice = data[data.length - 1].price

var currTs = _D(data[data.length - 1].ts)

var prePrice = data[0].price

var preTs = _D(data[0].ts)

var dataLen = data.length

tbl.rows.push([name, currPrice, prePrice, percentageChange + "%", dataLen, preTs, currTs])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

Sleep(5000)

}

}

코드 분석

- 1. 데이터 구조

- 2. Main function main()

2.1. Infinite loop

while (true) { / / }

The program continuously monitors the Binance API trading pair prices through an infinite loop.

2.2. Get price information

var arr = JSON.parse ((HttpQuery))https://api.binance.com/api/v3/ticker/price”))

Get the current price information of the trading pair via Binance API. If the return is not an array, wait for 5 seconds and retry.

2.3. Update price data

for (var i = 0; i < arr.length; i++) { / / }

Iterate through the array of obtained price information and update the data in dictSymbolsPrice. For each trading pair, add the current timestamp and price to the corresponding data array.

2.4. Exception processing

잡으세요

로그 (

Catch exceptions and log the exception information to ensure that the program can continue to execute.

2.5. Calculate the price fluctuations

(DictSymbolsPrice에 있는 var 기호) / / }

Iterate through dictSymbolsPrice, calculate the price fluctuations of each trading pair, and remove the earliest data if it is longer than 4 hours.

2.6. Sort and generate tables

var entries = Object.entries ((dictSymbolsPrice) entries.sort (((a, b) => b[1].percentage변경 - a[1].percentage변경)

for (var i = 0; i < entries.length; i++) { / / }

Sort the trading pairs in descending order of their price fluctuations and generate a table containing information about the trading pairs.

2.7. Log output and delay

로그 상태 (LogStatus)" + JSON.stringify(tbl) + "

Output the table and the current time in the form of a log and wait for 5 seconds to continue the next round of the loop.

The program obtains the real-time price information of the trading pair through Binance API, then calculates the price fluctuations, and outputs it to the log in the form of a table. The program is executed in a continuous loop to realize the function of real-time monitoring of the prices of trading pairs. Note that the program includes exception processing to ensure that the execution is not interrupted by exceptions when obtaining price information.

### Live Trading Running Test

Since data can only be collected bit by bit at the beginning, it is not possible to calculate the price fluctuations on a rolling basis without collecting enough data for a 4-hour window. Therefore, the initial price is used as the base for calculation, and after collecting enough data for 4 hours, the oldest data will be eliminated in order to maintain the 4-hour window for calculating the price fluctuations.

## 2. Check the full variety of funding rates for Binance U-denominated contracts

Checking the funding rate is similar to the above code, first of all, we need to check the Binance API documentation to find the funding rate related interface. Binance has several interfaces that allow us to query the rate of funds, here we take the interface of the U-denominated contract as an example:

GEThttps://fapi.binance.com/fapi/v1/premiumIndex

### Code Implementation

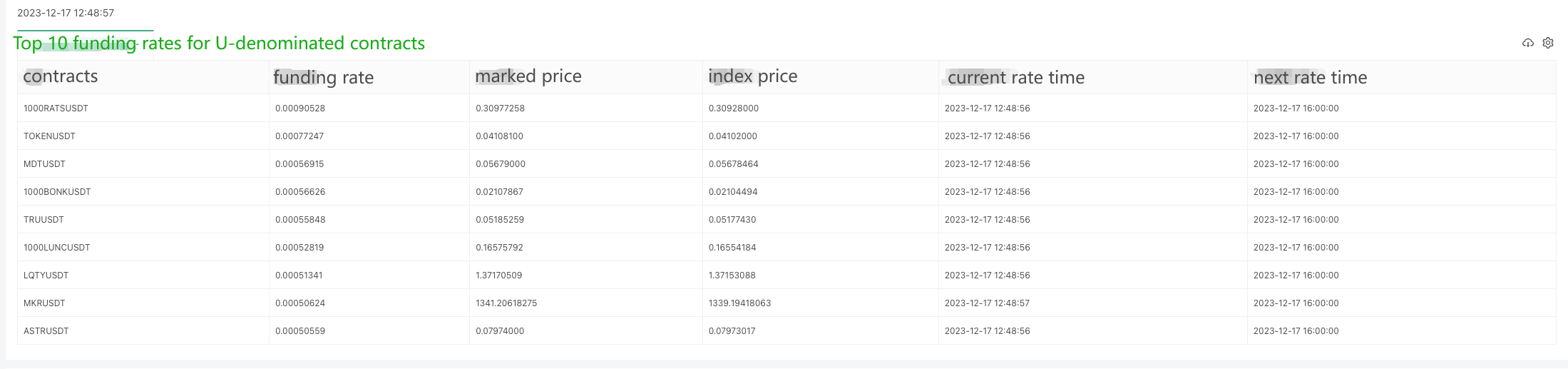

Since there are so many contracts, we're exporting the top 10 largest funding rates here.

함수 main() { while (true) { // GEThttps://fapi.binance.com/fapi/v1/premiumIndex시도해봐 var arr = JSON.parse ((HttpQuery))https://fapi.binance.com/fapi/v1/premiumIndex”)) if (!Array.isArray(arr)) { 수면 (5000) 계속해 }

arr.sort((a, b) => parseFloat(b.lastFundingRate) - parseFloat(a.lastFundingRate))

var tbl = {

type: "table",

title: "Top 10 funding rates for U-denominated contracts",

cols: ["contracts", "funding rate", "marked price", "index price", "current rate time", "next rate time"],

rows: []

}

for (var i = 0; i < 9; i++) {

var obj = arr[i]

tbl.rows.push([obj.symbol, obj.lastFundingRate, obj.markPrice, obj.indexPrice, _D(obj.time), _D(obj.nextFundingTime)])

}

LogStatus(_D(), "\n", "`" + JSON.stringify(tbl) + "`")

} catch(e) {

Log("e.name:", e.name, "e.stack:", e.stack, "e.message:", e.message)

}

Sleep(1000 * 10)

}

}

The returned data structure is as follows, and check the Binance documentation, it shows that lastFundingRate is the funding rate we want.

♪

Live trading running test:

### Getting OKX exchange contract funding rates of Python version

A user has asked for a Python version of the example, and it's for the OKX exchange. Here is an example:

The data returned by the interface ```https://www.okx.com/priapi/v5/public/funding-rate-all?currencyType=1```:

♪

Specific code:

수입 요청 json를 가져오기 시간 수입 수면 날짜 시간부터 수입 시간

def main (():

while True: while True: while True:

#https://www.okx.com/priapi/v5/public/funding-rate-all?currencyType=1시도해보세요:

응답 = 요청.get(

arr.sort(key=lambda x: float(x["fundingRate"]), reverse=True)

tbl = {

"type": "table",

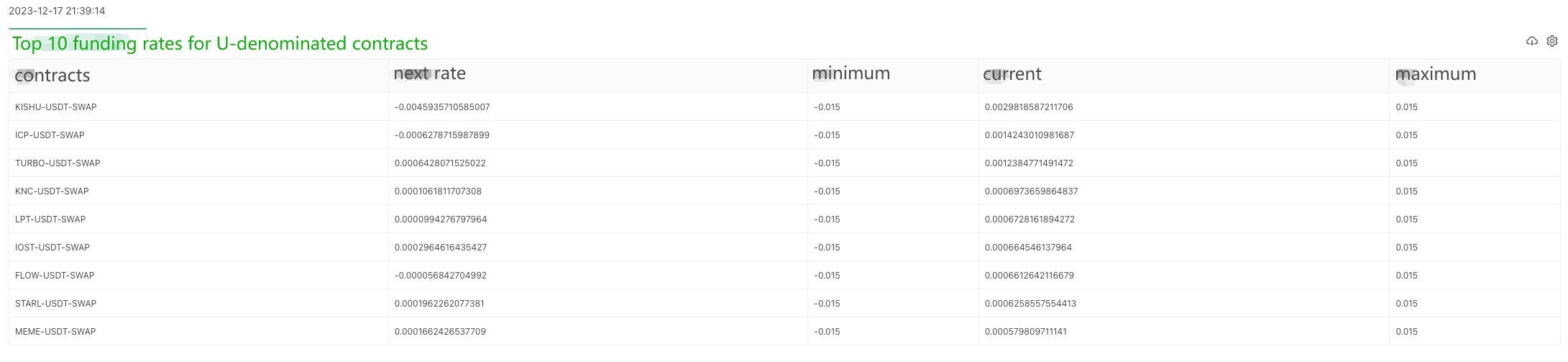

"title": "Top 10 funding rates for U-denominated contracts",

"cols": ["contracts", "next rate", "minimum", "current", "maximum"],

"rows": []

}

for i in range(min(9, len(arr))):

obj = arr[i]

row = [

obj["instId"],

obj["nextFundingRate"],

obj["minFundingRate"],

obj["fundingRate"],

obj["maxFundingRate"]

]

tbl["rows"].append(row)

LogStatus(_D(), "\n", '`' + json.dumps(tbl) + '`')

except Exception as e:

Log(f"Error: {str(e)}")

sleep(10)

END

이 예제들은 기본적인 디자인 아이디어와 호출 방법을 제공하는데, 실제 프로젝트는 특정 필요에 따라 적절한 변경 및 확장 작업을 수행해야 할 수 있습니다. 이러한 코드가 암호화폐 디지털 자산 거래의 다양한 요구를 더 잘 충족시키는 데 도움이 될 수 있기를 바랍니다.

- 암호화폐 시장의 근본 분석을 정량화: 데이터를 스스로 이야기하도록!

- 동전圈의 기초적인 양적 연구 - 더 이상 모든

선생님들을 믿지 말고, 데이터를 객관적으로 이야기하십시오! - 양적 거래 분야에서 필수 도구 - FMZ 양적 데이터 탐구 모듈

- 양적 거래의 필수 도구 - 발명자 양적 데이터 탐색 모듈

- 모든 것을 마스터 - FMZ에 대한 소개 트레이딩 터미널의 새로운 버전 (TRB 중재 소스 코드)

- FMZ의 새로운 거래 단말기 소개 (TRB 리비트 소스 추가)

- FMZ 퀀트: 암호화폐 시장에서 공통 요구 사항 설계 예제 분석 (II)

- 80 줄의 코드에서 고주파 전략으로 뇌 없는 판매봇을 이용하는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (II)

- 80줄의 코드의 고주파 전략으로 뇌 없는 로봇을 파는 방법

- FMZ 정량화: 암호화폐 시장의 일반적인 요구 디자인 사례 분석 (1)

- FMZ 퀀트 암호화폐 데모 거래소 WexApp가 새로 출시되었습니다.

- 영구 계약 그리드 전략 매개 변수 최적화의 자세한 설명

- 보트의 매개 변수를 배치 수정 하려면 FMZ 확장 API를 사용 하는 법을 가르쳐

- FMZ 확장 API를 사용하여 대량으로 디스크 변수를 변경하는 방법을 알려줍니다.

- 영구 계약 격자 전략 매개 변수 최적화 세부 사항

- 리눅스 바시에서 인터랙티브 브로커 IB 게이트웨이를 설치하는 지침

- 리눅스 바시에서 설치 침투보증 IB GATEWAY 설명

- 바닥 낚시, 낮은 시장 가치 또는 낮은 가격에 더 적합한?

- 저시장 가치와 낮은 가격, 어떤 것이 더 적합합니까?