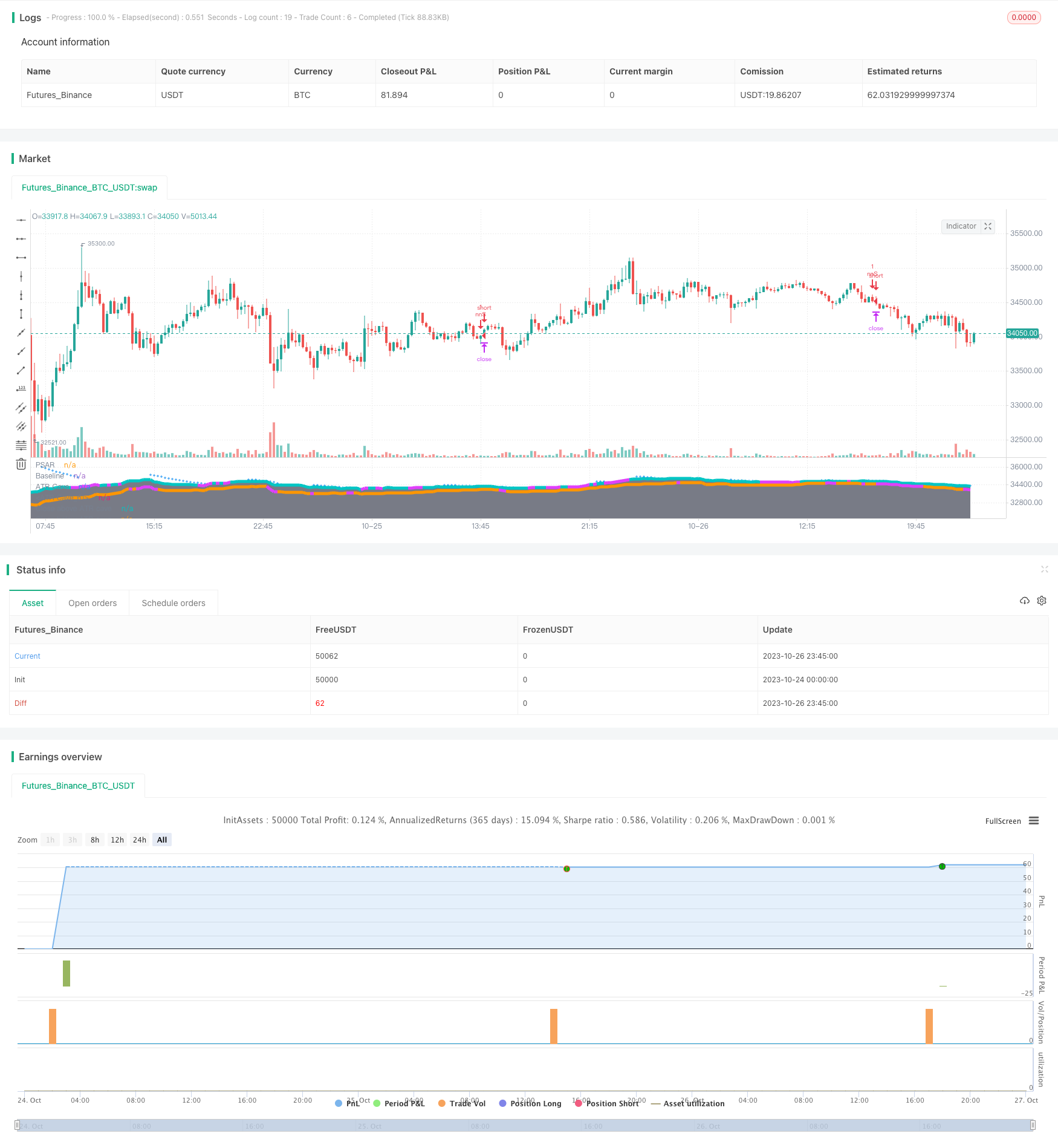

概述

双向ATR波浪交易策略是一种趋势跟踪策略,结合均线、ATR和多个技术指标,在趋势方向建立之后进行趋势跟踪交易。

策略原理

该策略使用Kijun线作为主要的均线指标,判断价格趋势方向。策略同时结合ATR通道,限制价格活动范围。当价格接近上轨时不做多,当价格接近下轨时不做空,避免追高杀跌。

当Kijun线发生向上突破时产生买入信号,当发生向下突破时产生卖出信号。为过滤误信号,策略还引入多个技术指标进行确认,包括Aroon指标、RSI指标、MACD指标和PSAR指标。满足所有指标的确认条件时,才生成买入和卖出信号。

入市后,策略采用止损和止盈方式管理仓位。止损点为0.5 ATR,止盈点为0.5%。当价格再次突破Kijun线反向时,选择立即止损退出。

策略优势

- 使用Kijun线判断趋势方向,避免被震荡市场套牢

- ATR通道限制价格活动范围,有利控制风险

- 多个技术指标确认,可大幅过滤误信号

- 结合止损止盈风险管理,有利锁定盈利

策略风险

- 多个指标确认造成信号延迟,可能错失趋势开始阶段

- 止损点过小可能频繁被止损出场

- Kijun线和ATR参数不合理可能导致频繁错误信号

- 依赖参数优化和历史数据拟合结果,实盘可能效果不佳

优化方向

- 尝试更先进的趋势判断指标,如Ichimoku云图等

- 调整止损止盈点,优化盈亏比

- 测试不同市场的最佳参数组合

- 增加自动调参功能,根据实时市场调整参数

- 测试不同Confirmation指标组合的效果

总结

双向ATR波浪交易策略综合使用均线、ATR通道以及多个辅助技术指标,在确定趋势方向后进行趋势跟踪操作。相比单一指标策略,可以大大提高信号质量和获利概率。同时止损止盈机制控制风险。通过参数优化和组合测试,该策略可望取得稳定的盈利。但需要注意过于依赖历史数据的问题,实盘效果仍需验证。持续优化是确保策略效果的关键。

策略源码

/*backtest

start: 2023-10-24 00:00:00

end: 2023-10-27 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// strategy(title="NoNonsense Forex", overlay=true, default_qty_value=100000, initial_capital=100)

//////////////////////

////// BASELINE //////

//////////////////////

ma_slow_type = input(title="Baseline Type", type=input.string, defval="Kijun", options=["ALMA", "EMA", "DEMA", "TEMA", "WMA", "VWMA", "SMA", "SMMA", "HMA", "LSMA", "Kijun", "McGinley"])

ma_slow_src = close //input(title="MA Source", type=input.source, defval=close)

ma_slow_len = input(title="Baseline Length", type=input.integer, defval=20)

ma_slow_len_fast = input(title="Baseline Length Fast", type=input.integer, defval=12)

lsma_offset = input(defval=0, title="* Least Squares (LSMA) Only - Offset Value", minval=0)

alma_offset = input(defval=0.85, title="* Arnaud Legoux (ALMA) Only - Offset Value", minval=0, step=0.01)

alma_sigma = input(defval=6, title="* Arnaud Legoux (ALMA) Only - Sigma Value", minval=0)

ma(type, src, len) =>

float result = 0

if type=="SMA" // Simple

result := sma(src, len)

if type=="EMA" // Exponential

result := ema(src, len)

if type=="DEMA" // Double Exponential

e = ema(src, len)

result := 2 * e - ema(e, len)

if type=="TEMA" // Triple Exponential

e = ema(src, len)

result := 3 * (e - ema(e, len)) + ema(ema(e, len), len)

if type=="WMA" // Weighted

result := wma(src, len)

if type=="VWMA" // Volume Weighted

result := vwma(src, len)

if type=="SMMA" // Smoothed

w = wma(src, len)

result := na(w[1]) ? sma(src, len) : (w[1] * (len - 1) + src) / len

if type=="HMA" // Hull

result := wma(2 * wma(src, len / 2) - wma(src, len), round(sqrt(len)))

if type=="LSMA" // Least Squares

result := linreg(src, len, lsma_offset)

if type=="ALMA" // Arnaud Legoux

result := alma(src, len, alma_offset, alma_sigma)

if type=="Kijun" //Kijun-sen

kijun = avg(lowest(len), highest(len))

result :=kijun

if type=="McGinley"

mg = 0.0

mg := na(mg[1]) ? ema(src, len) : mg[1] + (src - mg[1]) / (len * pow(src/mg[1], 4))

result :=mg

result

baseline = ma(ma_slow_type, ma_slow_src, ma_slow_len)

plot(baseline, title='Baseline', color=rising(baseline,1) ? color.green : falling(baseline,1) ? color.maroon : na, linewidth=3)

//////////////////

////// ATR ///////

//////////////////

atrlength=input(14, title="ATR Length")

one_atr=rma(tr(true), atrlength)

upper_atr_band=baseline+one_atr

lower_atr_band=baseline-one_atr

plot(upper_atr_band, color=color.gray, style=plot.style_areabr, transp=95, histbase=50000, title='ATR Cave')

plot(lower_atr_band, color=color.gray, style=plot.style_areabr, transp=95, histbase=0, title='ATR Cave')

plot(upper_atr_band, color=close>upper_atr_band ? color.fuchsia : na, style=plot.style_line, linewidth=5, transp=50, title='Close above ATR cave')

plot(lower_atr_band, color=close<lower_atr_band ? color.fuchsia : na, style=plot.style_line, linewidth=5, transp=50, title='Close below ATR cave')

donttradeoutside_atrcave=input(true)

too_high = close>upper_atr_band and donttradeoutside_atrcave

too_low = close<lower_atr_band and donttradeoutside_atrcave

////////////////////////////

////// CONFIRMATION 1 ////// the trigger actually

////////////////////////////

lenaroon = input(8, minval=1, title="Length Aroon")

c1upper = 100 * (highestbars(high, lenaroon+1) + lenaroon)/lenaroon

c1lower = 100 * (lowestbars(low, lenaroon+1) + lenaroon)/lenaroon

c1CrossUp=crossover(c1upper,c1lower)

c1CrossDown=crossunder(c1upper,c1lower)

////////////////////////////////

////// CONFIRMATION: MACD //////

////////////////////////////////

dont_use_macd=input(false)

macd_fast_length = input(title="Fast Length", type=input.integer, defval=13)

macd_slow_length = input(title="Slow Length", type=input.integer, defval=26)

macd_signal_length = input(title="Signal Smoothing", type=input.integer, minval = 1, maxval = 50, defval = 9)

macd_fast_ma = ema(close, macd_fast_length)

macd_slow_ma = ema(close, macd_slow_length)

macd = macd_fast_ma - macd_slow_ma

macd_signal = ema(macd, macd_signal_length)

macd_hist = macd - macd_signal

macdLong=macd_hist>0 or dont_use_macd

macdShort=macd_hist<0 or dont_use_macd

/////////////////////////////

///// CONFIRMATION: RSI /////

/////////////////////////////

dont_use_rsi=input(false)

lenrsi = input(14, minval=1, title="RSI Length") //14

up = rma(max(change(close), 0), lenrsi)

down = rma(-min(change(close), 0), lenrsi)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

rsiLong=rsi>50 or dont_use_rsi

rsiShort=rsi<50 or dont_use_rsi

//////////////////////////////

///// CONFIRMATION: PSAR /////

//////////////////////////////

dont_use_psar=input(false)

psar_start = input(0.03, step=0.01)

psar_increment = input(0.018, step=0.001)

psar_maximum = input(0.11, step=0.01) //default 0.08

psar = sar(psar_start, psar_increment, psar_maximum)

plot(psar, style=plot.style_cross, color=color.blue, title='PSAR')

psarLong=close>psar or dont_use_psar

psarShort=close<psar or dont_use_psar

/////////////////////////

///// CONFIRMATIONS /////

/////////////////////////

Long_Confirmations=psarLong and rsiLong and macdLong

Short_Confirmations=psarShort and rsiShort and macdShort

GoLong=c1CrossUp and Long_Confirmations and not too_high

GoShort=c1CrossDown and Short_Confirmations and not too_low

////////////////////

///// STRATEGY /////

////////////////////

use_exit=input(false)

KillLong=c1CrossDown and use_exit

KillShort=c1CrossUp and use_exit

SL=input(0.5, step=0.1)/syminfo.mintick

TP=input(0.005, step=0.001)/syminfo.mintick

strategy.entry("nnL", strategy.long, when = GoLong)

strategy.entry("nnS", strategy.short, when = GoShort)

strategy.exit("XL-nn", from_entry = "nnL", loss = SL, profit=TP)

strategy.exit("XS-nn", from_entry = "nnS", loss = SL, profit=TP)

strategy.close("nnL", when = KillLong)

strategy.close("nnS", when = KillShort)