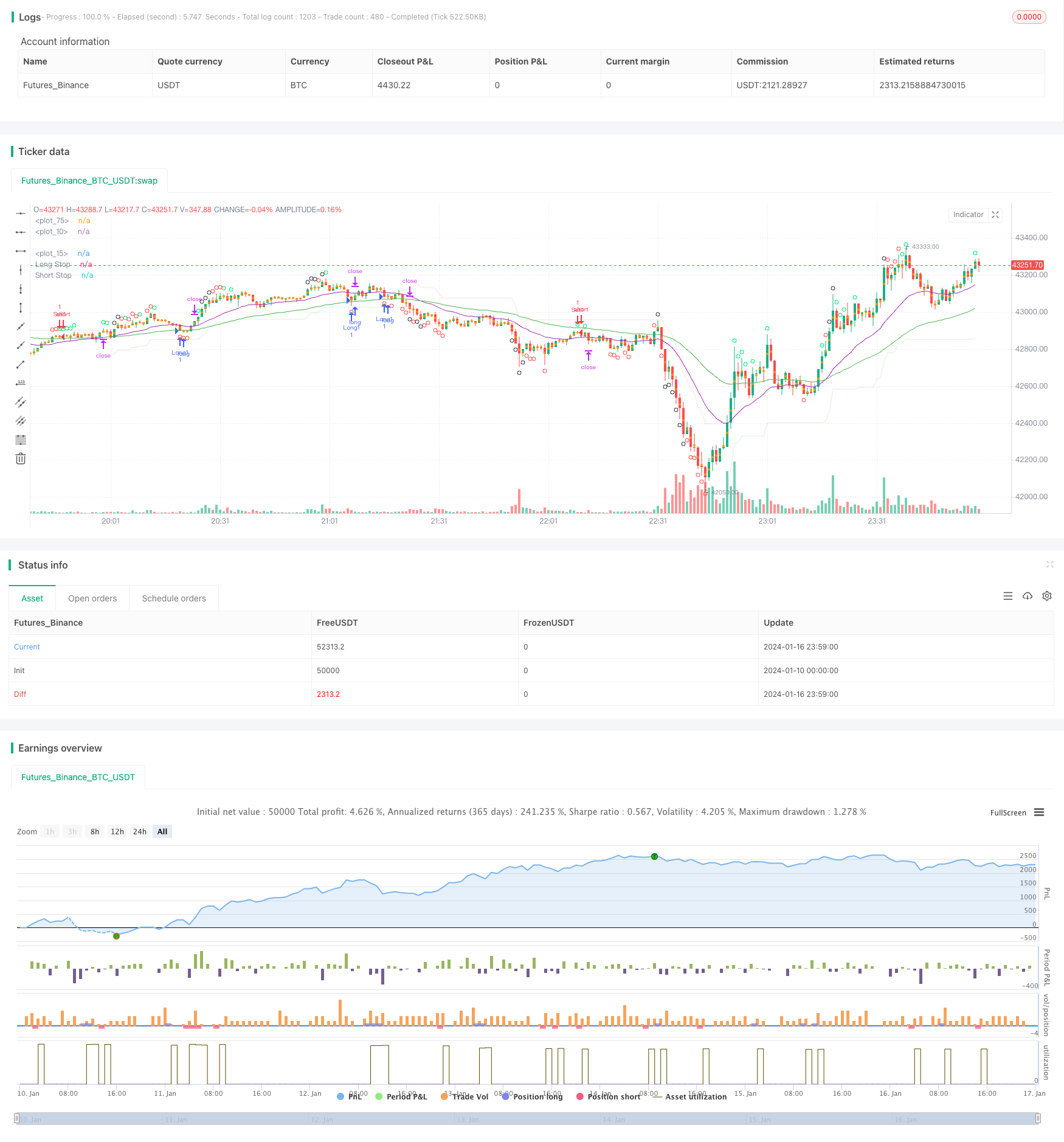

概述

耐心追踪趋势策略是一种趋势跟随型策略。它利用移动平均线的指标组合判断趋势方向,并结合超买超卖指标CCI发出交易信号。该策略追求大趋势,在震荡行情中可以有效避免被套。

策略原理

该策略使用21周期和55周期的EMA组合判断趋势方向。当短期EMA在长期EMA上方时定义为上升趋势,当短期EMA在长期EMA下方时定义为下降趋势。

CCI指标用于判断超买超卖情况。CCI上穿-100线为底部超卖讯号,下穿100线为顶部超买讯号。根据CCI指标的不同超买超卖线,策略分为三个交易信号强度级别。

在判断为上升趋势时,如果CCI指标发出强烈的底部超卖信号,就进行多头入场。判断为下降趋势时,如果CCI指标发出强烈的顶部超买信号,就进行空头入场。

止损线设置为SuperTrend指标,目标利润设置为固定的点数。

优势分析

该策略主要有以下优势:

- 追踪大趋势,避免被套

- CCI指标可以有效判断反转点位

- SuperTrend止损线设置合理

- 固定止损与固定止盈,风险可控

风险分析

该策略主要存在以下风险:

- 大趋势判断失误的概率

- CCI指标发出假信号的概率

- 止损点过浅或过深造成不必要止损的概率

- 固定止盈无法持续追踪趋势获利的概率

针对这些风险,我们可以通过调整EMA周期参数,CCI参数以及止损止盈点位来优化。同时引入更多指标进行策略信号验证也很有必要。

优化方向

该策略的优化方向主要有:

1.测试更多指标的组合,寻找更优趋势判断以及信号验证指标。

2.利用ATR动态止损止盈,以更好地跟踪趋势和控制风险。

3.引入基于历史数据训练的机器学习模型来判断趋势概率。

4.针对不同品种参数进行调整优化。

总结

耐心追踪趋势策略整体是一个非常实用的趋势跟随策略。它利用移动平均线判断大趋势方向,CCI指标发现反转点位信号,超级趋势止损线设定合理。通过参数调整与多指标组合验证,该策略可以进一步优化,值得长期实盘跟踪验证。

策略源码

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © greenmask9

//@version=4

strategy("Patient Trendfollower (7) Strategy", overlay=true)

// 21 EMA

emalength = input(21, title="Short EMA")

emashort = ema(close, emalength)

plot(emashort, color = color.purple, linewidth=1)

// 55 EMA

emalength2 = input(55, title="Long EMA")

ema = ema(close, emalength2)

plot(ema, color = color.green, linewidth=1)

//CCI calculation and inputs

lengthcci = input(20, minval=1, title="Overbought/sold detector period")

src = input(close, title="Overbought/sold detector source")

ma = sma(src, lengthcci)

ccivalue = (src - ma) / (0.015 * dev(src, lengthcci))

//CCI plotting

ccioverbought = input(defval=100, title="Overbought level 1")

ccioverbought2 = input(defval=140, title="Overbought level 2")

ccioverbought3 = input(defval=180, title="Overbought level 3")

ccioversold = input(defval=-100, title="Oversold level 1")

ccioversold2 = input(defval=-140, title="Oversold level 2")

ccioversold3 = input(defval=-180, title="Oversold level 3")

cciOB = (ccivalue >= ccioverbought and ccivalue < ccioverbought2)

plotshape(cciOB, title= "Overbought", location=location.abovebar, color=color.lime, transp=0, style=shape.circle)

cciOS = (ccivalue <= ccioversold and ccivalue > ccioversold2)

plotshape(cciOS, title= "Oversold", location=location.belowbar, color=color.lime, transp=0, style=shape.circle)

cciOB2 = (ccivalue >= ccioverbought2 and ccivalue < ccioverbought3)

plotshape(cciOB2, title= "Overbought", location=location.abovebar, color=color.red, transp=0, style=shape.circle)

cciOS2 = (ccivalue <= ccioversold and ccivalue > ccioversold3)

plotshape(cciOS2, title= "Oversold", location=location.belowbar, color=color.red, transp=0, style=shape.circle)

cciOB3 = (ccivalue >= ccioverbought3)

plotshape(cciOB3, title= "Overbought", location=location.abovebar, color=color.black, transp=0, style=shape.circle)

cciOS3 = (ccivalue <= ccioversold3)

plotshape(cciOS3, title= "Oversold", location=location.belowbar, color=color.black, transp=0, style=shape.circle)

//Supertrend

length = input(title="ATR Period", type=input.integer, defval=55)

mult = input(title="ATR Multiplier", type=input.float, step=0.1, defval=5.0)

wicks = input(title="Take Wicks into Account ?", type=input.bool, defval=true)

illuminate = input(title="Illuminate Trend", type=input.bool, defval=true)

atr = mult * atr(length)

longStop = hl2 - atr

longStopPrev = nz(longStop[1], longStop)

longStop := (wicks ? low[1] : close[1]) > longStopPrev ? max(longStop, longStopPrev) : longStop

shortStop = hl2 + atr

shortStopPrev = nz(shortStop[1], shortStop)

shortStop := (wicks ? high[1] : close[1]) < shortStopPrev ? min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir[1], dir)

dir := dir == -1 and (wicks ? high : close) > shortStopPrev ? 1 : dir == 1 and (wicks ? low : close) < longStopPrev ? -1 : dir

longColor = color.new(color.green, 90)

shortColor = color.new(color.red, 90)

noneColor = color.new(color.white, 100)

longStopPlot = plot(dir == 1 ? longStop : na, title="Long Stop", style=plot.style_linebr, linewidth=2, color=longColor)

shortStopPlot = plot(dir == 1 ? na : shortStop, title="Short Stop", style=plot.style_linebr, linewidth=2, color=shortColor)

midPricePlot = plot(ohlc4, title="", style=plot.style_circles, linewidth=0)

longFillColor = illuminate ? (dir == 1 ? longColor : noneColor) : noneColor

shortFillColor = illuminate ? (dir == -1 ? shortColor : noneColor) : noneColor

fill(midPricePlot, longStopPlot, title="Long State Filling", color=longFillColor)

fill(midPricePlot, shortStopPlot, title="Short State Filling", color=shortFillColor)

//entries

uptrend = emashort>ema and dir == 1

upsignal = ccivalue<=ccioversold and ccivalue>ccioversold2

upsignal2 = ccivalue<=ccioversold2 and ccivalue>ccioversold3

upsignal3 = ccivalue<=ccioversold3

downtrend = emashort<ema and dir == -1

downsignal = ccivalue>=ccioverbought and ccivalue<ccioverbought2

downsignal2 = ccivalue>=ccioverbought2 and ccivalue<ccioverbought3

downsignal3 = ccivalue>=ccioverbought3

//adapts to the current bar, I need to save the bars number when the condition for buy was true, static number is spread

spread = input (0.00020, title="Spread")

upstoploss = longStop - spread

downstoploss = shortStop + spread

strategy.initial_capital = 50000

ordersize=floor(strategy.initial_capital/close)

testlong = input(title="Test longs", type=input.bool, defval=true)

testshort = input(title="Test shorts", type=input.bool, defval=true)

//new

degree = input(title="Test level 1 overbought/sold levels", type=input.bool, defval=true)

degree2 = input(title="Test level 2 overbought/sold levels", type=input.bool, defval=false)

degree3 = input(title="Test level 3 overbought/sold levels", type=input.bool, defval=false)

statictarget = input(title="Use static target", type=input.bool, defval=true)

statictargetvalue = input(title="Static target in pips", type=input.integer, defval=400)

//timetrade = input(title="Open trades only withing specified time", type=input.bool, defval=true)

//timtrade = input()

//přidat možnost TP podle ATR a sl podle ATR

buy1 = uptrend and upsignal and strategy.opentrades==0 and testlong and degree

x1 = barssince (buy1)

if (buy1)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long1", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long1" , profit=statictargetvalue,stop=upstoploss[x1])

buy2 = uptrend and upsignal2 and strategy.opentrades==0 and testlong and degree2

x2 = barssince (buy2)

if (buy2)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long2", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long2" , profit=statictargetvalue,stop=upstoploss[x2])

buy3 = uptrend and upsignal3 and strategy.opentrades==0 and testlong and degree3

x3 = barssince (buy3)

if (buy3)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long3", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long3" , profit=statictargetvalue,stop=upstoploss[x3])

sell1 = downtrend and downsignal and strategy.opentrades==0 and testshort and degree

y1 = barssince (sell1)

if (sell1)

if (statictarget)

strategy.entry("Sell1", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell1" , profit=statictargetvalue,stop=downstoploss[y1])

sell2 = downtrend and downsignal2 and strategy.opentrades==0 and testshort and degree2

y2 = barssince (sell2)

if (sell2)

if (statictarget)

strategy.entry("Sell2", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell2" , profit=statictargetvalue,stop=downstoploss[y2])

sell3 = downtrend and downsignal3 and strategy.opentrades==0 and testshort and degree3

y3 = barssince (sell3)

if (sell3)

if (statictarget)

strategy.entry("Sell3", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell3" , profit=statictargetvalue,stop=downstoploss[y3])