ডাবল মুভিং এভারেজ ক্রস টাইম ফ্রেম ট্রেডিং কৌশল

ওভারভিউ

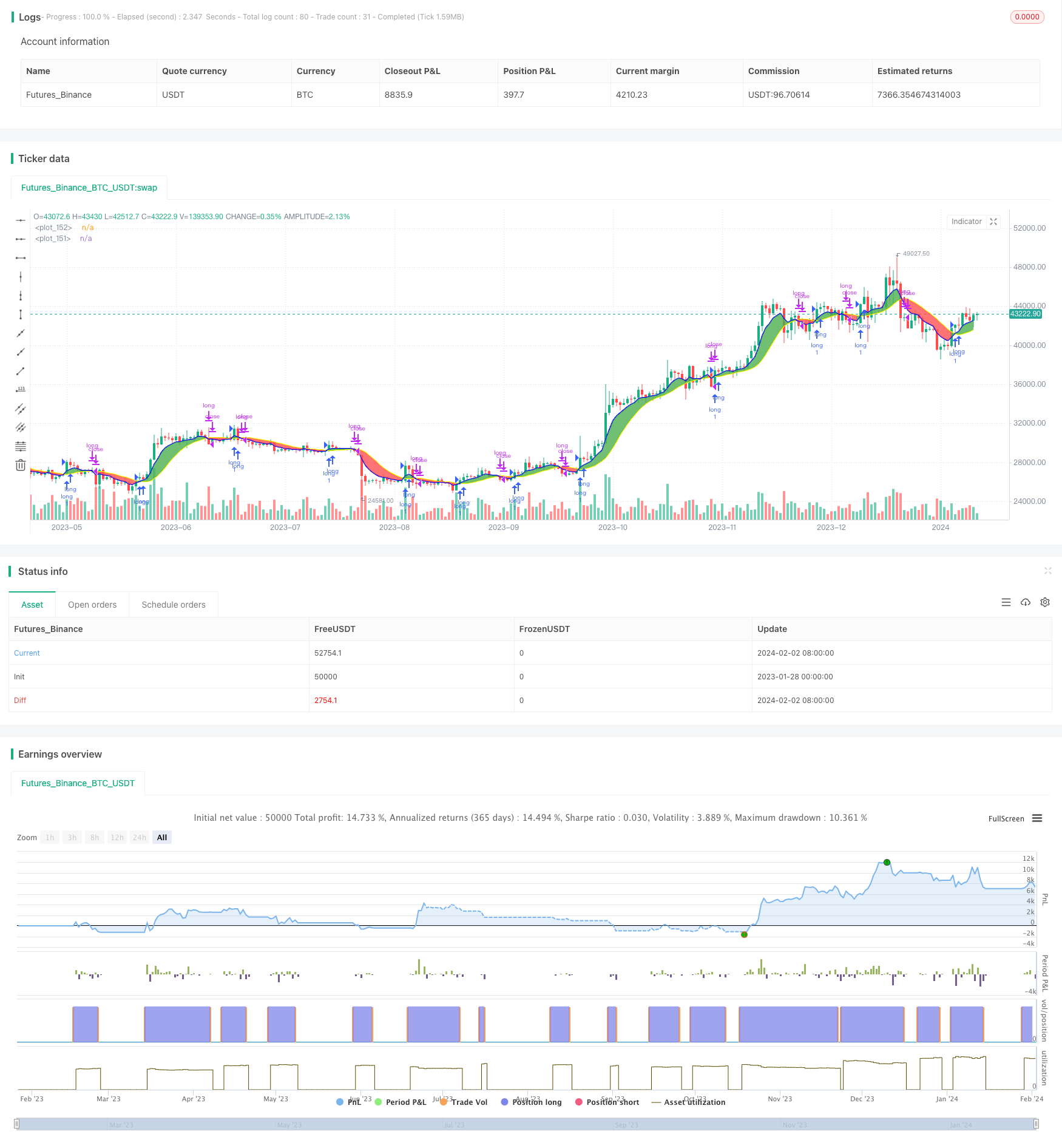

এই কৌশলটি দুটি ভিন্ন টাইপ মুভিং এভারেজ গণনা করে দুটি ভিন্ন টাইম ফ্রেমে ক্রয় এবং বিক্রয় সংকেত তৈরি করে। এটি একটি খুব ভাল স্যান্ডবক্স কৌশল যা বিভিন্ন টাইপ মুভিং এভারেজ এবং বিভিন্ন টাইম ফ্রেম সমন্বয় পরীক্ষা করার জন্য ব্যবহার করা যেতে পারে।

কৌশল নীতি

এই কৌশলটি দুটি চলমান গড় ব্যবহার করে, একটি দ্রুত চলমান গড় এবং একটি ধীর চলমান গড়। দ্রুত চলমান গড়ের সময় ফ্রেমটি চার্টের সময় ফ্রেমের চেয়ে বড় বা সমান। যখন দ্রুত চলমান গড়টি ধীর চলমান গড়কে অতিক্রম করে তখন একটি কেনার সংকেত উত্পন্ন হয়; যখন দ্রুত চলমান গড়টি ধীর চলমান গড়কে অতিক্রম করে তখন একটি বিক্রয় সংকেত উত্পন্ন হয়।

ব্যবহারকারীরা বিভিন্ন ধরণের মুভিং এভারেজ যেমন এসএমএ, ইএমএ, কামা ইত্যাদি বেছে নিতে পারেন, সময় ফ্রেমগুলি বিভিন্ন হতে পারে, যাতে সমন্বয় পরীক্ষার মাধ্যমে সর্বোত্তম প্যারামিটারগুলি খুঁজে পাওয়া যায়।

সামর্থ্য বিশ্লেষণ

এই কৌশলটির সবচেয়ে বড় সুবিধা হল যে এটি সর্বোত্তম প্যারামিটার সেটিং খুঁজতে প্যারামিটার পরীক্ষার বিভিন্ন সমন্বয়কে খুব সহজেই সামঞ্জস্য করতে পারে।

ব্যবহারকারীরা তাদের পছন্দমত দুই ধরনের মুভিং এভারেজ টাইপ, টাইম লেংথ এবং টাইম ফ্রেম বেছে নিতে পারেন। সিস্টেমটি রিয়েল টাইমে তাদের গণনা করে এবং ফলাফলগুলি প্রদর্শন করে। এটি একটি একক প্যারামিটার পরীক্ষা করার চেয়ে অনেক সহজ।

এবং এই কৌশলটি একটি স্টপ লস স্টপ ফাংশন রয়েছে যা ঝুঁকি হ্রাস করে এবং মুনাফার সম্ভাবনা বাড়ায়।

ঝুঁকি বিশ্লেষণ

এই কৌশলটির সবচেয়ে বড় ঝুঁকি হল যে, প্যারামিটার সেটিং ভুল হলে ট্রেডিং সিগন্যাল খুব বেশি ঘন ঘন হতে পারে, যার ফলে ট্রেডিং খরচ এবং স্লাইড পয়েন্টের ক্ষতি হয়।

এছাড়াও, ডাবল মুভিং এভারেজ নিজেই একটি মিথ্যা সংকেত তৈরি করতে পারে, এবং যদি প্যারামিটারগুলি ভুলভাবে নির্বাচিত হয়, তবে একটি ক্রয়-বিক্রয় সংকেত অবিশ্বস্ত হতে পারে।

এই ঝুঁকিগুলি অপ্টিমাইজেশান প্যারামিটার এবং অন্যান্য সূচকগুলির সমন্বয় দ্বারা হ্রাস করা যেতে পারে।

অপ্টিমাইজেশান দিক

ডাবল মুভিং এভারেজের উপর ভিত্তি করে অন্যান্য সূচক সমন্বয় যুক্ত করার বিষয়টি বিবেচনা করা যেতে পারে, যেমন RSI সূচকগুলিকে ক্রয়-বিক্রয় সংকেত নিশ্চিত করার জন্য ফিল্টার করা যায়, যার ফলে ভুয়া সংকেত হ্রাস করা যায়।

অন্যদিকে, চলমান গড়ের প্যারামিটার প্রশিক্ষণের অপ্টিমাইজেশনের চেষ্টা করা যেতে পারে, যাতে সর্বোত্তম প্যারামিটার সমন্বয় খুঁজে পাওয়া যায়। প্যারামিটারগুলিকে গতিশীলভাবে অপ্টিমাইজ করার জন্য মেশিন লার্নিং পদ্ধতি ব্যবহার করাও বিবেচনা করা যেতে পারে।

সারসংক্ষেপ

এই কৌশলটি একটি খুব ভাল ডাবল মুভিং এভারেজ এক্সপেরিমেন্টাল স্যান্ডবক্স। এর সুবিধা হল যে এটি দ্রুত সর্বোত্তম ট্রেডিং কৌশল খুঁজে পেতে বিভিন্ন প্যারামিটার সমন্বয়কে পুনরাবৃত্তি করতে পারে। অবশ্যই, কিছু প্যারামিটার সেট করার ঝুঁকিও রয়েছে, যা অন্য সূচক সমন্বয় যোগ করে ঝুঁকি কমাতে ফিল্টার করা প্রয়োজন। যদি এই কৌশলটি অপ্টিমাইজ করতে থাকে তবে সম্ভবত আরও ভাল ট্রেডিং ফলাফল পাওয়া যাবে।

/*backtest

start: 2023-01-28 00:00:00

end: 2024-02-03 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License https://creativecommons.org/licenses/by-sa/4.0/

// © dman103

// A moving averages SandBox strategy where you can experiment using two different moving averages (like KAMA, ALMA, HMA, JMA, VAMA and more) on different time frames to generate BUY and SELL signals, when they cross.

// Great sandbox for experimenting with different moving averages and different time frames.

//

// == How to use ==

// We select two types of moving averages on two different time frames:

//

// First is the FAST moving average that should be at the same time frame or higher.

// Second is the SLOW moving average that should be on the same time frame or higher.

// When FAST moving average cross over the SLOW moving average we have a BUY signal (for LONG)

// When FAST moving average cross under the SLOW moving average we have a SELL signal (for SHORT)

// WARNING: Using a lower time frame than your chart time frame will result in unrealistic results in your backtesting and bar replay.

// == NOTES ==

// You can select BOTH, LONG, SHORT or NONE in the strategy settings.

// You can also enable Stop Loss and Take Profit.

// More sandboxes to come, Follow to get notified.

// Can also act as indicator by settings 'What trades should be taken' to 'NONE'

//@version=4

strategy("Multi MA MTF SandBox Strategy","Multi MA SandBox",overlay=true)

tradeType = input("LONG", title="What trades should be taken:", options=["LONG", "SHORT", "BOTH", "NONE"])

fast_title = input(true, title='---------------- Fast Moving Average (BLUE)----------------', type=input.bool)

ma_select1 = input(title="First Slow moving average", defval="EMA", options=["SMA", "EMA", "WMA", "HMA", "JMA", "KAMA", "TMA", "VAMA", "SMMA", "DEMA" , "VMA", "WWMA", "EMA_NO_LAG", "TSF","ALMA"])

resma_fast = input(title="First Time Frame", type=input.resolution, defval="")

lenma_fast = input(title="First MA Length", type=input.integer, defval=6)

slow_title = input(true, title='---------------- Slow Moving Average (YELLOW)----------------', type=input.bool)

ma_select2 = input(title="Second Fast moving average", defval="JMA", options=["SMA", "EMA", "WMA", "HMA", "JMA", "KAMA", "TMA", "VAMA", "SMMA", "DEMA" , "VMA", "WWMA", "EMA_NO_LAG", "TSF","ALMA"])

resma_slow = input(title="Second time frame", type=input.resolution, defval="")

lenma_slow = input(title="Second MA length", type=input.integer, defval=14)

settings = input(true, title='---------------- Other Settings ----------------', type=input.bool)

lineWidth = input(2,title="Line Width")

colorTransparency=input(50,title="Color Transparency",step=10,minval=0,maxval=100)

color_fast=input(color.blue,type=input.color)

color_slow=input(color.yellow,type=input.color)

fillColor = input(title="Fill Color", type=input.bool, defval=true)

IndicatorSettings = input(true, title='---------------- Indicators Settings ----------------', type=input.bool)

offset=input(title="Alma Offset (only for ALMA)",defval=0.85, step=0.05)

volatility_lookback =input(title="Volatility lookback (only for VAMA)",defval=12)

i_fastAlpha = input(1.25,"KAMA's alpha (only for KAMA)", minval=1,step=0.25)

fastAlpha = 2.0 / (i_fastAlpha + 1)

slowAlpha = 2.0 / (31)

///////Moving Averages

MA_selector(src, length,ma_select) =>

ma = 0.0

if ma_select == "SMA"

ma := sma(src, length)

ma

if ma_select == "EMA"

ma := ema(src, length)

ma

if ma_select == "WMA"

ma := wma(src, length)

ma

if ma_select == "HMA"

ma := hma(src,length)

ma

if ma_select == "JMA"

beta = 0.45*(length-1)/(0.45*(length-1)+2)

alpha = beta

tmp0 = 0.0, tmp1 = 0.0, tmp2 = 0.0, tmp3 = 0.0, tmp4 = 0.0

tmp0 := (1-alpha)*src + alpha*nz(tmp0[1])

tmp1 := (src - tmp0[0])*(1-beta) + beta*nz(tmp1[1])

tmp2 := tmp0[0] + tmp1[0]

tmp3 := (tmp2[0] - nz(tmp4[1]))*((1-alpha)*(1-alpha)) + (alpha*alpha)*nz(tmp3[1])

tmp4 := nz(tmp4[1]) + tmp3[0]

ma := tmp4

ma

if ma_select == "KAMA"

momentum = abs(change(src, length))

volatility = sum(abs(change(src)), length)

efficiencyRatio = volatility != 0 ? momentum / volatility : 0

smoothingConstant = pow((efficiencyRatio * (fastAlpha - slowAlpha)) + slowAlpha, 2)

var kama = 0.0

kama := nz(kama[1], src) + smoothingConstant * (src - nz(kama[1], src))

ma:=kama

ma

if ma_select == "TMA"

ma := sma(sma(src, ceil(length / 2)), floor(length / 2) + 1)

ma

if ma_select == "VMA"

valpha=2/(length+1)

vud1=src>src[1] ? src-src[1] : 0

vdd1=src<src[1] ? src[1]-src : 0

vUD=sum(vud1,9)

vDD=sum(vdd1,9)

vCMO=nz((vUD-vDD)/(vUD+vDD))

VAR=0.0

VAR:=nz(valpha*abs(vCMO)*src)+(1-valpha*abs(vCMO))*nz(VAR[1])

ma := VAR

ma

if ma_select == "WWMA"

wwalpha = 1/ length

WWMA = 0.0

WWMA := wwalpha*src + (1-wwalpha)*nz(WWMA[1])

ma := WWMA

ma

if ma_select == "EMA_NO_LAG"

EMA1= ema(src,length)

EMA2= ema(EMA1,length)

Difference= EMA1 - EMA2

ma := EMA1 + Difference

ma

if ma_select == "TSF"

lrc = linreg(src, length, 0)

lrc1 = linreg(src,length,1)

lrs = (lrc-lrc1)

TSF = linreg(src, length, 0)+lrs

ma := TSF

ma

if ma_select =="VAMA" // Volatility Adjusted from @fractured

mid=ema(src,length)

dev=src-mid

vol_up=highest(dev,volatility_lookback)

vol_down=lowest(dev,volatility_lookback)

ma := mid+avg(vol_up,vol_down)

ma

if ma_select == "SMMA"

smma = float (0.0)

smaval=sma(src, length)

smma := na(smma[1]) ? smaval : (smma[1] * (length - 1) + src) / length

ma := smma

if ma_select == "DEMA"

e1 = ema(src, length)

e2 = ema(e1, length)

ma := 2 * e1 - e2

ma

if ma_select == "ALMA"

ma := alma(src, length,offset, 6)

ma

ma

// Calculate EMA

ma_fast = MA_selector(close, lenma_fast,ma_select1)

ma_slow = MA_selector(close, lenma_slow,ma_select2)

maFastStep = security(syminfo.tickerid, resma_fast, ma_fast)

maSlowStep = security(syminfo.tickerid, resma_slow, ma_slow)

ma1_plot=plot(maFastStep, color=color_fast,linewidth=lineWidth,transp=colorTransparency)

ma2_plot=plot(maSlowStep, color=color_slow,linewidth=lineWidth,transp=colorTransparency)

colors=ma_fast>ma_slow ? color.green : color.red

fill(ma1_plot,ma2_plot, color=fillColor? colors: na,transp=colorTransparency+15)

closeStatus = strategy.openprofit > 0 ? "win" : "lose"

////////Long Rules

long = crossover(maFastStep,maSlowStep) and (tradeType == "LONG" or tradeType == "BOTH")

longClose =crossunder(maFastStep,maSlowStep)//and falling(maSlowStep,1)

///////Short Rules

short =crossunder(maFastStep,maSlowStep) and (tradeType == "SHORT" or tradeType == "BOTH")

shortClose = crossover(maFastStep,maSlowStep)

longShape= crossover(maFastStep,maSlowStep) and tradeType == "NONE"

shortShape = crossunder(maFastStep,maSlowStep) and tradeType == "NONE"

plotshape(longShape, style=shape.triangleup,location=location.belowbar, color=color.lime,size=size.small)

plotshape(shortShape,style=shape.triangledown,location=location.abovebar, color=color.red,size=size.small)

// === Stop LOSS ===

useStopLoss = input(false, title='----- Add Stop Loss / Take profit -----', type=input.bool)

sl_inp = input(2.5, title='Stop Loss %', type=input.float, step=0.1)/100

tp_inp = input(5, title='Take Profit %', type=input.float, step=0.1)/100

stop_level = strategy.position_avg_price * (1 - sl_inp)

take_level = strategy.position_avg_price * (1 + tp_inp)

stop_level_short = strategy.position_avg_price * (1 + sl_inp)

take_level_short = strategy.position_avg_price * (1 - tp_inp)

if (long)

strategy.entry("long", strategy.long)

if (short)

strategy.entry("short", strategy.short)

strategy.close ("long", when = longClose, comment=closeStatus)

strategy.close ("short", when = shortClose, comment=closeStatus)

if (useStopLoss)

strategy.exit("Stop Loss/Profit Long","long", stop=stop_level, limit=take_level,comment =closeStatus )

strategy.exit("Stop Loss/Profit Short","short", stop=stop_level_short, limit=take_level_short, comment = closeStatus)