Hybride quantitative Handelsstrategie mit zwei Indikatoren

Überblick

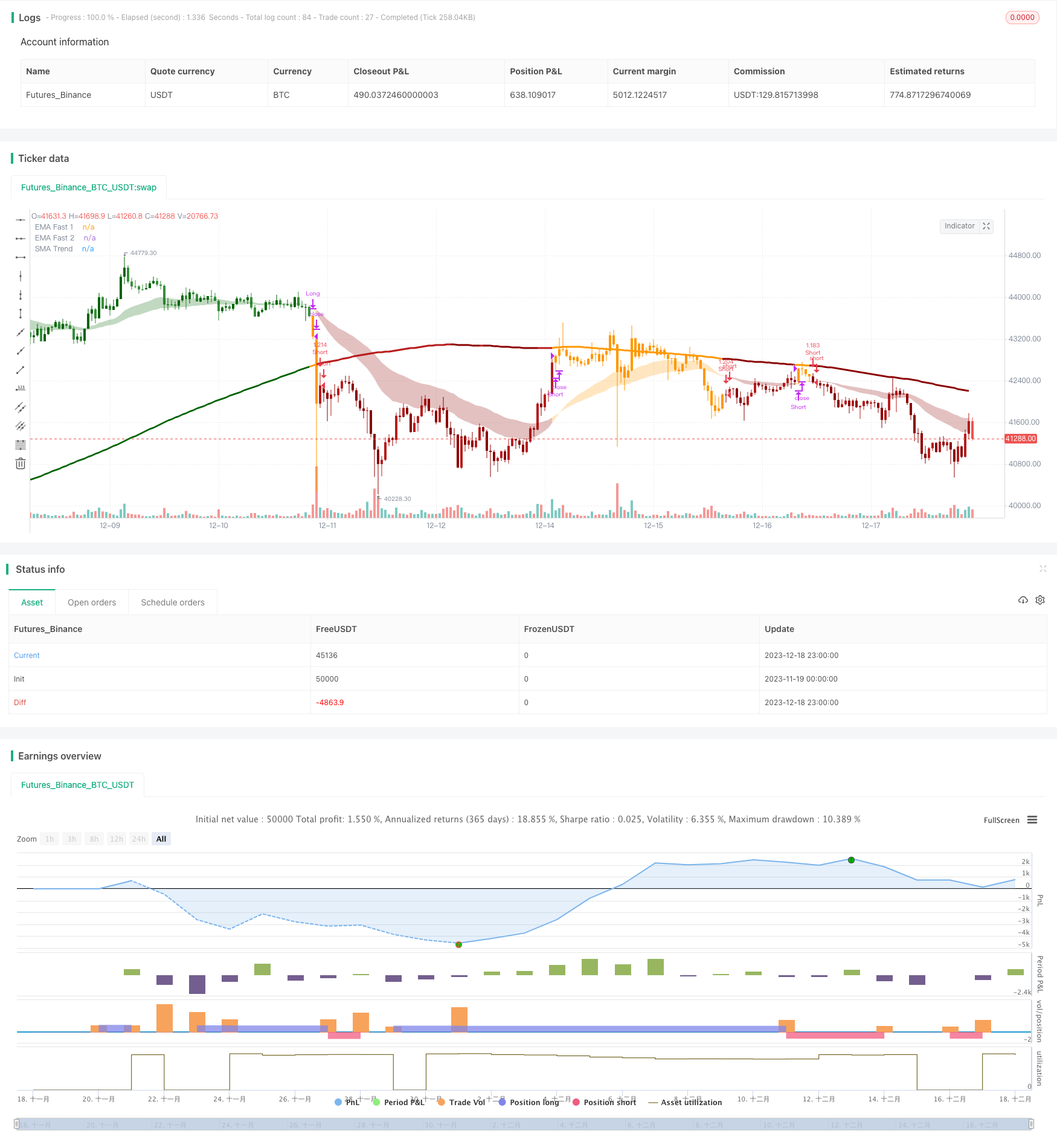

Diese Strategie identifiziert die Richtung eines Trends und handelt durch die Kombination von zwei Indicatoren. Erstens verwendet sie die Kreuzung zweier Moving Averages (Fastline und Medium-Speed-Line), um einen kurzfristigen Trend zu beurteilen. Zweitens verwendet sie die Kanalbreite und den langfristigen Moving Average, um die Richtung des Haupttrends zu beurteilen.

Strategieprinzip

Die Strategie verwendet drei Gruppen von Indikatoren. Zuerst wird der Gold- und die Gold-Fork-Death-Fork der schnellen EMA (Zyklus 26) und der mittleren EMA (Zyklus 50) verwendet, um den kurzfristigen Trend zu beurteilen. Zweitens wird der Kanalbereich berechnet, um zu beurteilen, ob der Preis diesen Bereich überschritten hat, um den mittelfristigen Trend zu beurteilen.

Die Logik des Urteils lautet:

Die Kreuzung von Schnell- und Mittelgeschwindigkeitslinien (Gold- und Todesforken) bestimmt die Richtung der kurzfristigen Trends.

Die Richtung des mittelfristigen Trends wird durch die Frage beurteilt, ob der Preis die Kanalbreite überschritten hat. Die Kanalbreite wird mit einem Faktor multipliziert, der auf der langfristigen Durchschnittslinie plus minus ATR basiert. Wenn der Preis die Obergrenze überschritten hat, ist dies ein Beobachtungswert.

Der Vergleich zwischen den Preisen und der Größe der langfristigen Durchschnittslinie beurteilt die wichtigsten Trends.

Schließlich wird nur dann ein Handelssignal ausgesendet, wenn die drei Beurteilungen “kurz”, “mittler” und “lang” übereinstimmen. Dieses Mischvermögen kann falsche Signale effektiv filtern und die Stabilität verbessern.

Strategische Vorteile

Diese Strategie der Doppelmessung hat mehrere Vorteile:

Es ist möglich, falsche Signale effektiv zu filtern und die Stabilität zu verbessern. Da die Handelssignale die Verifizierung von Ergebnissen aus mehreren Indikatoren benötigen, werden fehlerhafte Signale durch einen einzelnen Indikator vermieden.

Hohe Flexibilität bei der Anpassung der Parameter des Indikators an den Markt. Die Parameter der schnellen Durchschnittslinie und des Kanalbereichs können für verschiedene Marktumgebungen angepasst werden.

In Kombination mit Trend-Trading und Bandbreite-Trading. Die mittelfristigen Indikatoren erfassen die Trends, die langfristigen Indikatoren bestimmen die Bandbreiten, die insgesamt die Vorteile von Trend- und Umkehrstrategien bieten.

Die Effizienz der Verwendung von Geldern ist hoch. Die Bestellung kann nur dann effizient verwendet werden, wenn die Ergebnisse mehrerer Indikatoren übereinstimmen, um unnötige Transaktionen zu vermeiden.

Strategisches Risiko

Die Strategie birgt auch einige Risiken:

Risiken bei der Einstellung von Parametern. Moving Average Periodicity und Channel Range Parameter müssen vernünftig eingestellt werden, was dazu führen kann, dass Trends nicht effektiv entdeckt werden oder zu viele falsche Signale erzeugt werden.

Doppelte Kennzahlen erhöhen die Kosten für die Handelsmöglichkeiten. Im Vergleich zur Strategie mit einem einzigen Kennzeichen können einige Handelsmöglichkeiten verpasst werden und es ist nicht möglich, an den besten Punkten ein- und auszusteigen.

Die Stop-Loss-Strategie erfordert Vorsicht. Ein Durchbruch des Stop-Loss-Mechanismus in dieser Strategie kann zu unnötigen Verlusten führen und erfordert eine vorsichtige Einstellung der Stop-Loss-Ratio.

Die Strategie ist besser geeignet für eine marktwirtschaftliche Situation, in der ein deutlicher Trend zu erkennen ist.

Richtung der Strategieoptimierung

Diese Strategie kann in folgenden Bereichen optimiert werden:

Verschiedene Parameterkombinationen werden getestet, um die besten Parameter zu finden. Die optimale Parameter-Einstellung kann durch weitere Tests mit historischen Daten gefunden werden.

Erhöhung der automatischen Stop-Loss-Methode. Die Stop-Loss-Methode kann in Kombination mit dem Volatility Indicator dynamisch angepasst werden.

Zunahme der Quantitätsindikatoren zur Unterstützung der Beurteilung der Größe der Positionen an den Schlüsselpunkten und zur Verbesserung der Effizienz der Verwendung von Geldern.

Optimierung der Eintrittslogik. Mehr über die Cost Average-Strategie für die Eintrittsgruppe nachzudenken, um das Risiko einer Eintrittsgruppe zu verringern.

In Kombination mit einem maschinellen Lernmodell soll die robustheit und die Eignungsfähigkeit eines Modells beurteilt werden.

Zusammenfassen

Diese Strategie kann durch die schnelle und mittlere Dreifachmessung und die Doppel-Verifizierungs-Mechanik die falschen Signale wirksam unterdrücken und die Stabilität verbessern. Die Strategie bietet zugleich die Vorteile des Trendhandels und des Intervallhandels und eine hohe Effizienz bei der Verwendung von Kapital. Die Strategie kann durch Parameteroptimierung, Stop-Loss-Optimierung, Kombination von Quantitativ-Energie-Indikatoren und andere Möglichkeiten verbessert werden.

/*backtest

start: 2023-11-19 00:00:00

end: 2023-12-19 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// Indicator to combines:

// Trend Channel[Gu5] (SMA 200) +

// EMA's cross (26, 50 ) +

// Golden Cross (50, 200)

// Author: @gu5tavo71 08/2019

// v2.3.6, 2022.02.18

// Trend Channel [Gu5] // Author: @gu5tavo71 08/2019

//

// This source code is subject to these terms:

// Attribution-NonCommercial 4.0 International (CC BY-NC 4.0)

// https://www.safecreative.org/work/2202190517452-mix1-ema-cross-trend-channel-gu5-

// You are free to:

// Share, copy and redistribute this script

// Adapt, transform and build on this script

// Under the following terms:

// Non-commercial: You cannot sell my indicator. You can't sell my work.

// Attribution: If you post part of my code, you must give me proper credit

//

// I am using part of this code published by @PineCoders and Public Library

// Disclaimer: I am not a financial advisor.

// For purpose educate only. Use at your own risk.

strategy(title = 'Mix1 : Ema Cross + Trend Channel [Gu5] - Backtest', shorttitle = 'Mix01', overlay = true,

initial_capital = 100,

default_qty_value = 100,

default_qty_type = strategy.percent_of_equity,

commission_value = 0.075,

commission_type = strategy.commission.percent,

format = format.price,

precision = 2,

process_orders_on_close = true)

// --------- Inputs "==============================" |

i_maSrc = input.source (close, 'MA Source' , group = 'EMAs')

i_maFast1 = input.int (26, 'EMA Fast' , group = 'EMAs')

i_maFast2 = input.int (50, 'EMA Medium' , group = 'EMAs')

i_maLen = input.int (200, 'MA Trend' , group = 'Trend Channel')

o_maLen1 = 'EMA'

o_maLen2 = 'SMA'

i_maLenSel = input.string (o_maLen2, 'MA Type' , group = 'Trend Channel',

options = [o_maLen1, o_maLen2],

tooltip = "EMA or SMA")

i_htf = input.timeframe ('', 'Select Higher Timeframe' , tooltip = 'Only for MA Trend' , group = 'Trend Channel')

i_rangeLen = input.float (0.618, 'Channel Range Length' , tooltip = 'ATR of the MA Trend', group = 'Trend Channel')

i_slOn = input.bool (false, '■ Stop Loss On/Off' , group = 'Stop Loss')

i_sl = input.float (2.618, 'SL %' , step = 0.1, group = 'Stop Loss')

i_periodSw = input.bool (true, '■ Period On/Off' , group = 'Period')

o_start = timestamp ( '2020-01-01 00:00 GMT-3' )

o_end = timestamp ( '2099-12-31 00:00 GMT-3' )

i_periodStar = input (o_start, 'Start Time' , group = 'Period')

i_periodEnd = input (o_end, 'End Time' , group = 'Period')

o_posSel1 = 'Only Long'

o_posSel2 = 'Only Short'

o_posSel3 = 'Both'

i_posSel = input.string (o_posSel3, 'Position Type' , group = 'Strategy',

options = [o_posSel1, o_posSel2, o_posSel3],

tooltip = "Only Long, Only short or Both")

o_typeS1 = 'Strategy 1'

o_typeS2 = 'Strategy 2'

i_typeS = input.string (o_typeS2, 'Strategy Type' , group = 'Strategy',

options = [o_typeS1, o_typeS2],

tooltip = "Strategy 1:\nLong, when the price (close) crosses the ema.\nStrategy 2:\nLong, only when ema goes up")

i_barColOn = input.bool (true, '■ Bar Color On/Off' , group = 'Display')

i_alertOn = input.bool (false, '■ Alert On/Off' , group = 'Display')

i_channelOn = input.bool (false, '■ Channel Range On/Off' , tooltip = 'If the price (close) is over than the channel, the trend is bullish. If the price is under, bearish. And if the price is in the channel, it is in range', group = 'Display')

i_goldenOn = input.bool (false, '■ Golden Cross On/Off' )

o_alert = '{{strategy.order.comment}}'

i_alert = input.string (o_alert, 'Setting alert' , tooltip = 'For Alerts, just copy {{strategy.order.comment}} and paste in alert window.', group = 'Display')

// --------- Calculations

maFast1 = ta.ema(i_maSrc, i_maFast1)

maFast2 = ta.ema(i_maSrc, i_maFast2)

maDir = maFast1 > maFast2 ? 1 : -1

maTrend = request.security(syminfo.tickerid, i_htf,

i_maLenSel == "SMA" ? ta.sma(close, i_maLen)[1] : ta.ema(close, i_maLen)[1],

lookahead = barmerge.lookahead_on) //No repaint

maTrendDir = i_maSrc >= maTrend ? 1 : -1

rangeAtr = ta.atr(i_maLen) * i_rangeLen

rangeTop = maTrend + rangeAtr

rangeBot = maTrend - rangeAtr

rangeCh = (open <= rangeTop or close <= rangeTop) and

(open >= rangeBot or close >= rangeBot)

trendDir = i_typeS == 'Strategy 1' ?

rangeCh ? 0 :

maTrendDir == 1 and maDir == 1 and maTrend > maFast2 ? 0 :

maTrendDir == -1 and maDir == -1 and maTrend < maFast2 ? 0 :

maTrendDir == 1 and maDir == 1 ? 1 :

maTrendDir == -1 and maDir == -1 ? -1 : 0 :

rangeCh ? 0 :

maTrendDir == 1 and maDir == 1 ? 1 :

maTrendDir == -1 and maDir == -1 ? -1 : 0

GCross = i_goldenOn ? ta.crossover (maFast2, maTrend) : na

DCross = i_goldenOn ? ta.crossunder(maFast2, maTrend) : na

period = true

// Set initial values

condition = 0.0

entryLong = trendDir == 1 and

i_posSel != 'Only Short' and

(i_periodSw ? period : true)

entryShort = trendDir == -1 and

i_posSel != 'Only Long' and

(i_periodSw ? period : true)

exitLong = (trendDir != 1 or maDir == -1) and

condition[1] == 1 and

i_posSel != 'Only Short' and

(i_periodSw ? period : true)

exitShort = (trendDir != -1 or maDir == 1) and

condition[1] == -1 and

i_posSel != 'Only Long' and

(i_periodSw ? period : true)

closeCond = exitLong or exitShort

// Stop Loss (sl)

slEntry = close * i_sl / 100

slTop = close + slEntry

slBot = close - slEntry

slTopBuff = ta.valuewhen(condition[1] != 1 and entryLong, slBot, 0)

slBotBuff = ta.valuewhen(condition[1] != -1 and entryShort, slTop, 0)

slLine = condition[1] == -1 and entryLong ? slTopBuff :

condition[1] == 1 and entryShort ? slBotBuff :

condition[1] == 1 or entryLong ? slTopBuff :

condition[1] == -1 or entryShort ? slBotBuff : na

slTopCross = condition[1] == 1 and ta.crossunder(close, slLine) or high > slLine and low < slLine

slBotCross = condition[1] == -1 and ta.crossover (close, slLine) or high > slLine and low < slLine

slExit = i_slOn ? slTopCross or slBotCross : na

// Conditions

condition := condition[1] != 1 and entryLong ? 1 :

condition[1] != -1 and entryShort ? -1 :

condition[1] != 0 and slExit ? 0 :

condition[1] != 0 and exitLong ? 0 :

condition[1] != 0 and exitShort ? 0 : nz(condition[1])

long = condition[1] != 1 and condition == 1

short = condition[1] != -1 and condition == -1

xl = condition[1] == 1 and exitLong and not slExit

xs = condition[1] == -1 and exitShort and not slExit

sl = condition[1] != 0 and slExit

// --------- Colors

c_green = #006400 //Green

c_greenLight = #388e3c //Green Light

c_red = #8B0000 //Red

c_redLight = #b71c1c //Red Light

c_emas = xl ? color.new(color.orange, 99) :

xs ? color.new(color.orange, 99) :

trendDir == 1 and maDir == 1 ? color.new(c_green, 99) :

trendDir == -1 and maDir == -1 ? color.new(c_red, 99) :

color.new(color.orange, 99)

c_maFill = xl ? color.new(color.orange, 70) :

xs ? color.new(color.orange, 70) :

trendDir == 1 and maDir == 1 ? color.new(c_green, 70) :

trendDir == -1 and maDir == -1 ? color.new(c_red, 70) :

color.new(color.orange, 70)

c_maTrend = trendDir == 0 ? color.new(color.orange, 0) :

trendDir == 1 and maTrend[1] < maTrend ? color.new(c_green, 0) :

trendDir == 1 and maTrend[1] >= maTrend ? color.new(c_greenLight, 0) :

trendDir == -1 and maTrend[1] < maTrend ? color.new(c_redLight, 0) :

trendDir == -1 and maTrend[1] >= maTrend ? color.new(c_red, 0) : na

c_ch = trendDir == 0 ? color.new(color.orange, 50) :

trendDir == 1 ? color.new(c_green, 50) :

trendDir == -1 ? color.new(c_red, 50) : na

c_slLineUp = ta.rising (slLine, 1)

c_slLineDn = ta.falling(slLine, 1)

c_slLine = c_slLineUp ? na :

c_slLineDn ? na : color.red

c_barCol = trendDir == 0 ? color.new(color.orange, 0) :

trendDir == 1 and open <= close ? color.new(c_green, 0) :

trendDir == 1 and open > close ? color.new(c_greenLight, 0) :

trendDir == -1 and open >= close ? color.new(c_red, 0) :

trendDir == -1 and open < close ? color.new(c_redLight, 0) :

color.new(color.orange, 0)

// --------- Plots

p_maFast1 = plot(

maFast1,

title = 'EMA Fast 1',

color = c_emas,

linewidth = 1)

p_maFast2 = plot(

maFast2,

title = 'EMA Fast 2',

color = c_emas,

linewidth = 2)

fill(

p_maFast1, p_maFast2,

title = 'EMAs Fill',

color = c_maFill)

plot(

maTrend,

title = 'SMA Trend',

color = c_maTrend,

linewidth = 3)

p_chTop = plot(

i_channelOn ? rangeTop : na,

title = 'Top Channel',

color = c_maTrend,

linewidth = 1)

p_chBot = plot(

i_channelOn ? rangeBot : na,

title = 'Bottom Channel',

color = c_maTrend,

linewidth = 1)

fill(

p_chTop, p_chBot,

title = 'Channel',

color = c_ch)

plot(

i_slOn and condition != 0 ? slLine : na,

title = 'Stop Loss Line',

color = c_slLine,

linewidth = 1,

style = plot.style_linebr)

// --------- Alerts

barcolor(i_barColOn ? c_barCol : na)

plotshape(

i_alertOn and long ? high : na,

title = 'Long Label',

text = 'Long',

textcolor = color.white,

color = color.new(c_green, 0),

style = shape.labelup,

size = size.normal,

location = location.belowbar)

plotshape(

i_alertOn and short ? low : na,

title = 'Short Label',

text = 'Short',

textcolor = color.white,

color = color.new(c_red, 0),

style = shape.labeldown,

size = size.normal,

location = location.abovebar)

plotshape(

i_alertOn and (xl or xs) ? close : na,

title = 'Close Label',

text = 'Close',

textcolor = color.orange,

color = color.new(color.orange, 0),

style = shape.xcross,

size = size.small,

location = location.absolute)

plotshape(

i_alertOn and sl ? slLine : na,

title = 'Stop Loss',

text = 'Stop\nLoss',

textcolor = color.orange,

color = color.new(color.orange, 0),

style = shape.xcross,

size = size.small,

location = location.absolute)

plotshape(

i_alertOn and i_goldenOn and GCross ? maTrend : na,

title = 'Golden Cross Label',

text = 'Golden\nCross',

textcolor = color.white,

color = color.new(color.orange, 0),

style = shape.labelup,

size = size.normal,

location = location.absolute)

plotshape(

i_alertOn and i_goldenOn and DCross ? maTrend : na,

title = 'Death Cross Label',

text = 'Death\nCross',

textcolor = color.white,

color = color.new(color.orange, 0),

style = shape.labeldown,

size = size.normal,

location = location.absolute)

bgcolor(

i_periodSw and not period ? color.new(color.gray, 90) : na,

title = 'Session')

// --------- Backtest

if long and strategy.position_size == 0 and barstate.isconfirmed

strategy.entry('Long', strategy.long, comment = 'long')

if short and strategy.position_size == 0 and barstate.isconfirmed

strategy.entry('Short', strategy.short, comment = 'short')

strategy.exit(

id = 'XL',

from_entry = 'Long',

stop = i_slOn ? slLine : na)

strategy.exit(

id = 'XS',

from_entry = 'Short',

stop = i_slOn ? slLine : na)

strategy.close(

'Long',

comment = 'Close',

when = xl)

strategy.close(

'Short',

comment = 'Close',

when = xs)