Bandpass Mean PB Indicator Strategy

Author: ChaoZhang, Date: 2024-01-17 17:10:53Tags:

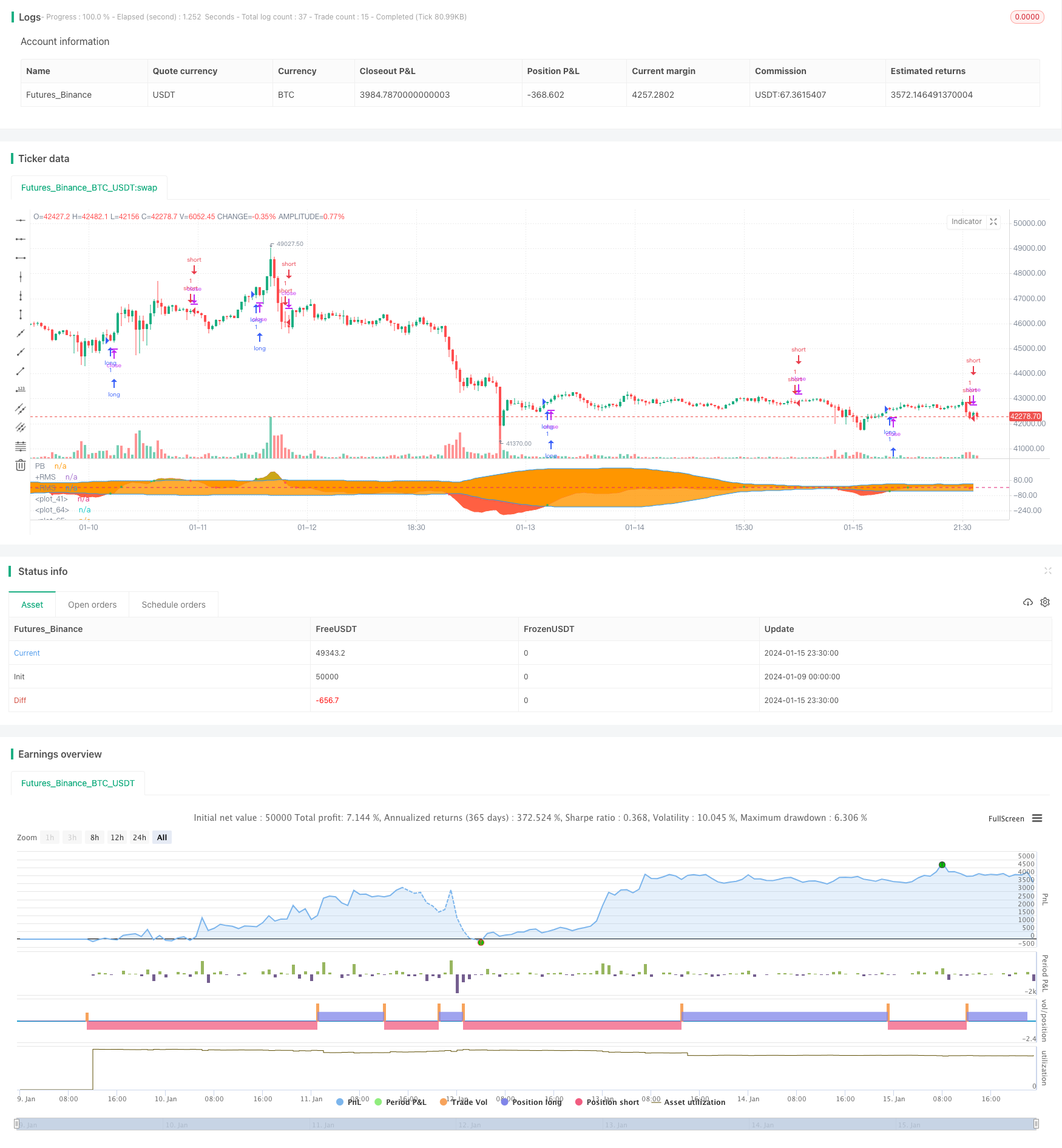

Overview

This strategy calculates the mean PB indicator and Bollinger bands to determine the golden cross and dead cross relationship between the PB indicator and the upper and lower rails of the Bollinger bands. It generates buy signals when the PB indicator breaks above the middle rail or lower rail of the Bollinger bands, and generates sell signals when the PB indicator breaks below the middle rail or upper rail of the Bollinger bands.

Strategy Principle

The core indicator of the strategy is the mean PB indicator. The mean PB indicator combines the stability of the moving average system and the sensitivity of the PB indicator. It uses the difference between fast and slow moving averages of different cycles to express price change trends to determine the long and short trends.

The strategy also uses the Bollinger Band indicator to identify overbought and oversold conditions of the stock price. The Bollinger Band indicator consists of three curves: middle rail, upper rail and lower rail. The middle rail is the n-day moving average; the upper and lower rails are calculated based on the middle rail and historical volatility. When the stock price is close to the upper rail, it is in the overbought zone; when it is close to the lower rail, it is in the oversold zone, and the area around the middle rail is a reasonable price range for the stock.

In summary, this strategy cleverly uses the mean PB indicator to determine the uptrend or downtrend of stock prices, and the Bollinger bands as an auxiliary indicator to determine overbought and oversold conditions, to find trading signals from the relationship between the two indicators. It belongs to a typical technical indicator trading strategy.

Advantage Analysis

The main advantages of this strategy are:

- Use the mean PB indicator to determine changes in price trends, high sensitivity

- Assist with Bollinger Bands to identify overbought and oversold zones to improve accuracy of determining entry and exit points

- Simple strategy logic, easy to implement

- Backtest data shows relatively satisfactory returns

Risk Analysis

The main risks of this strategy are:

- Both the mean PB indicator and Bollinger Bands rely on historical data for calculation. They may generate incorrect signals when stock prices fluctuate sharply.

- The PB indicator and Bollinger Bands are quite sensitive to parameter settings. Inappropriate settings may lead to excessive incorrect trades.

- Macro environment changes during the strategy implementation period, such as economic crisis, policy changes, etc., may cause the failure of the strategy.

To address the above risks, methods like optimizing parameter settings, strict stop loss, considering macro factors, manual monitoring can be used for risk mitigation.

Optimization Directions

The optimization directions for this strategy include:

- Optimize parameters of the mean PB indicator and Bollinger Bands to find the best parameter combination

- Add other indicators for filtration, such as MACD, KDJ, etc. to improve strategy performance

- Add stop loss mechanisms to effectively control single loss

- Incorporate larger time frame indicators to determine the major trend to avoid trading against the trend

Conclusion

The overall performance of this strategy is quite satisfactory. With the mean PB indicator as its core and Bollinger Bands to assist determining trading signals, it has simple logic, high sensitivity, and decent backtest results. By continuing to optimize parameter settings, adding other assisting indicators, implementing strict stop loss etc., the profitability and stability of the strategy can be further improved. It is worth verifying in live trading and application.

/*backtest

start: 2024-01-09 00:00:00

end: 2024-01-16 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("BandPass EOS", overlay=false, initial_capital = 1000)

src = input(close, "Source", input.source)

Period1 = input(41, "Fast Period", input.integer)

Period2 = input(54, "Slow Period", input.integer)

showBG = input(false, "Show crosses on background?", input.bool)

UseReversalStop = input(true, "Use additional triggers?", input.bool)

//Super Passband Filter

a1 = 0.0

a2 = 0.0

PB = 0.0

RMS = 0.0

if bar_index > Period1

a1 := 5 / Period1

a2 := 5 / Period2

PB := (a1 - a2) * src + (a2 * (1 - a1) - a1 * (1 - a2)) * src[1] +

(1 - a1 + 1 - a2) * nz(PB[1]) - (1 - a1) * (1 - a2) * nz(PB[2])

for i = 0 to 49 by 1

RMS := RMS + PB[i] * PB[i]

RMS

RMS := sqrt(RMS / 40)

RMS

z = 0

buy = PB > PB [5] and crossover(PB, -RMS) or PB > PB [5] and crossover (PB, RMS) or PB > PB [5] and crossover (PB, z)

sell = PB < PB [5] and crossunder(PB, RMS) or PB < PB [5] and crossunder (PB, -RMS) or PB < PB [5] and crossunder (PB, z)

signal = buy ? 1 : sell ? -1 : 0

bg = buy ? color.green : sell ? color.red : color.white

bg := showBG ? bg : na

upperFill = PB>RMS ? color.lime : na

lowerFill = PB<-RMS ? color.red : na

p1 = plot(PB,"PB",color.red)

p2 = plot(RMS,"+RMS",color.blue)

p3 = plot(-RMS,"-RMS",color.blue)

bgcolor(bg)

fill(p1,p2,upperFill)

fill(p1,p3,lowerFill)

hline(0)

//PERIOD

testStartYear = input(2018, "Backtest Start Year")

testStartMonth = input(1, "Backtest Start Month")

testStartDay = input(1, "Backtest Start Day")

testPeriodStart = timestamp(testStartYear,testStartMonth,testStartDay, 0, 0)

testStopYear = input(2019, "Backtest Stop Year")

testStopMonth = input(12, "Backtest Stop Month")

testStopDay = input(31, "Backtest Stop Day")

testPeriodStop = timestamp(testStopYear,testStopMonth,testStopDay, 0, 0)

testPeriod() => true

lcolor = PB > PB [5] and crossover(PB, -RMS) or PB > PB [5] and crossover (PB, RMS) or PB > PB [5] and crossover (PB, z)

scolor = PB < PB [5] and crossunder(PB, RMS) or PB < PB [5] and crossunder (PB, -RMS) or PB < PB [5] and crossunder (PB, z)

c1 = (PB < PB [5] and crossunder(PB, RMS) or PB < PB [5] and crossunder (PB, -RMS) or PB < PB [5] and crossunder (PB, z))

c2 = (PB > PB [5] and crossover(PB, -RMS) or PB > PB [5] and crossover (PB, RMS) or PB > PB [5] and crossover (PB, z))

plot (c1 ? PB : na, style = plot.style_circles, color = color.red, linewidth = 3)

plot (c2 ? PB : na, style = plot.style_circles, color = color.green, linewidth = 3)

if (PB > PB [5] and crossover(PB, -RMS) or PB > PB [5] and crossover (PB, RMS) or PB > PB [5] and crossover (PB, z))

strategy.entry("long", strategy.long, when = testPeriod())

if (PB < PB [5] and crossunder(PB, RMS) or PB < PB [5] and crossunder (PB, -RMS) or PB < PB [5] and crossunder (PB, z))

strategy.entry("short", strategy.short, when = testPeriod())

- Dual Confirmation Reversal Trend Tracking Strategy

- MACD Indicator Driven OBV Quant Trading Strategy

- Dollar Cost Averaging After Downtrend Strategy

- Triple Indicators Sentiment Driven Breakout Strategy

- A Trend Reversal Strategy Based on Moving Averages, Price Patterns and Volume

- Dual Moving Average Strategy

- Momentum Moving Average Crossover Trading Strategy

- Dual Moving Average Golden Cross Strategy

- Momentum Wave Bollinger Bands Trend Strategy

- Reverse Momentum Trading Strategy

- RSI & Fibonacci 5-Minute Trading Strategy

- Triple Moving Average Combined with MACD Quantitative Strategy

- Momentum Breakout Optimization

- Baseline Cross Qualifier ATR Volatility & HMA Trend Bias Mean Reversion Strategy

- Volatility Bands and VWAP Multi-Timeframe Stock Trend Trading Strategy

- Price Reversal with Crossover Capturing Strategy

- Ehlers Stochastic Cyber Cycle Strategy

- Breakthrough of Daily High-low Price Based on Fibonacci Levels

- Improved SuperTrend Strategy

- Quantitative Trading Strategy Integrating MACD, RSI and RVOL