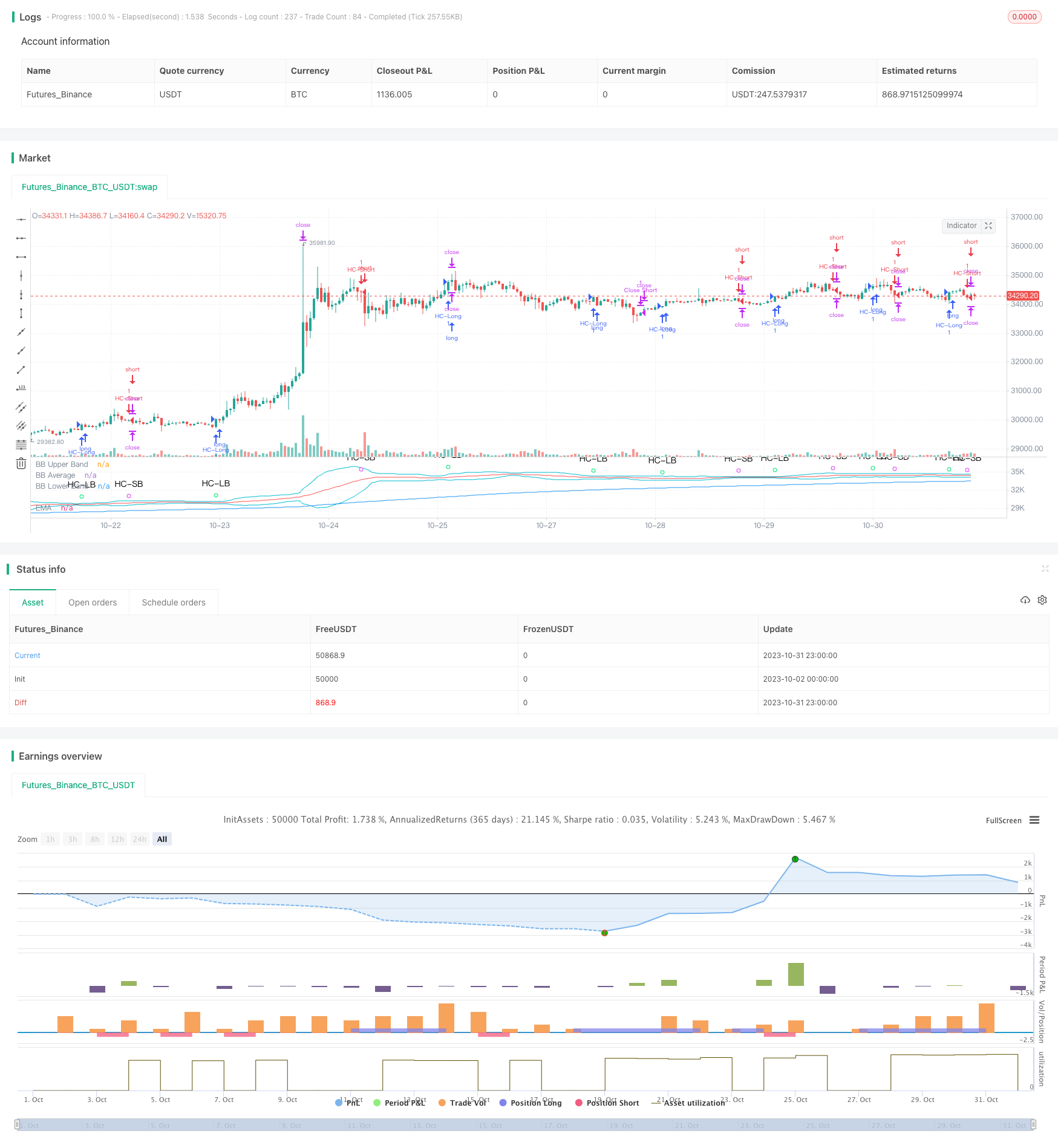

Estrategia de trading cuantitativo que utiliza múltiples indicadores para identificar puntos de reversión de trading

Descripción general

Esta estrategia utiliza los cinco indicadores EMA, VWAP, MACD, Bollinger Bands y Schaff Trend Cycle para identificar los puntos de inflexión de los precios dentro de un rango determinado y emitir señales de compra y venta. La ventaja de la estrategia es que puede adaptarse a la combinación de diferentes indicadores del mercado, reducir la probabilidad de señales falsas y aumentar la probabilidad de obtener ganancias.

Principio de estrategia

La EMA promedio determina la dirección de la tendencia general y compra solo en la dirección de la tendencia

VWAP considera que los fondos de las instituciones se dirigen hacia adquisiciones y adquisiciones en la dirección de adquisiciones

El MACD determina la tendencia de la línea corta y el cambio de movimiento, la línea de señal de ruptura de la línea MACD se considera una señal de compra/venta

Las Bandas de Bollinger determinan si se ha sobrevendido o sobrevendido, y el precio cruza la vía descendente como una señal de compra/venta

El Schaff Trend Cycle considera que el corto plazo es un giro de la estructura de reestructuración, y que superar el umbral alto o bajo es una señal de compra/venta.

Cuando las cinco principales señales se unen, se emite una orden de compra/venta.

Establecer puntos de parada y de suspensión para optimizar la administración de fondos

Ventajas estratégicas

- La combinación de múltiples indicadores reduce la probabilidad de falsas señales

La combinación de varios indicadores, como EMA, VWAP, MACD, BB y STC, se pueden verificar entre sí, reduciendo la falsa señal producida por un solo indicador y, por lo tanto, aumentando la fiabilidad de la señal.

- Indicadores personalizados

Permite elegir si se utiliza un indicador o una combinación de indicadores en función de diferentes variedades y entornos del mercado, lo que hace que la estrategia sea más específica y adaptable.

- Optimización de la gestión de fondos

Establezca puntos de parada y de retención para limitar las pérdidas individuales y bloquear parte de las ganancias, para una mejor administración de los fondos.

- La estrategia está clara.

Utilizando indicadores simples e intuitivos, y acompañados de comentarios detallados en el código, la idea de la estrategia es clara y fácil de entender y modificar.

- Es muy práctico.

Se utilizan ampliamente varios indicadores, los parámetros son razonables, se pueden usar directamente en operaciones reales, y se pueden lograr buenos resultados sin necesidad de una gran optimización.

Riesgo estratégico

- Riesgo de identificar cambios en el indicador con retraso

Los indicadores como EMA, MACD y otros están un poco atrasados en la identificación de los cambios en los precios, y pueden perderse el momento de compra óptima.

- Riesgo de configuración incorrecta de los parámetros

Si los parámetros del indicador están mal configurados, se generarán una gran cantidad de falsas señales que no permitirán el funcionamiento normal de la estrategia.

- El riesgo de una victoria no garantizada

La combinación de múltiples indicadores puede aumentar las probabilidades de éxito, pero no garantiza que todas las transacciones sean rentables. Los cambios en el entorno del mercado pueden reducir las probabilidades de éxito.

- El punto de parada establece un riesgo demasiado pequeño

Si se establece un punto de parada demasiado pequeño, se puede detener la salida de pérdidas cuando los precios fluctúan normalmente, aumentando las pérdidas innecesarias.

Dirección de optimización de la estrategia

- Aumentar los modelos de aprendizaje automático para determinar la fiabilidad de la señal

Se puede entrenar a los modelos para juzgar la fiabilidad de las señales de múltiples indicadores, calificarlas y reducir las falsas señales.

- Aumentar los indicadores cuantitativos para la identificación de las tendencias

La introducción de indicadores cuantitativos como el OBV para identificar señales de impulso en los precios y aumentar la certeza de los puntos de compra

- Optimización de las estrategias de stop loss

Se pueden estudiar estrategias móviles de stop loss o lock-in más adecuadas para esta estrategia, optimizando la administración de fondos.

- Optimización de parámetros

Optimización de los parámetros de cada indicador a través de una retroalimentación más sistemática para mejorar la solidez general de la estrategia.

- Aumentar el comercio de robots

La conexión a la API de transacciones, la implementación de pedidos automáticos, permite que las estrategias funcionen realmente sin guardias.

Resumir

Esta estrategia integra las ventajas de varios indicadores técnicos, la claridad de la idea, la practicidad, puede ser utilizado como referencia para la toma de decisiones en el comercio discrecional, también puede ser utilizado directamente en el comercio algorítmico. Sin embargo, todavía es necesario realizar ajustes optimizados para variedades específicas y entornos de mercado, reducir el riesgo y mejorar la estabilidad, para finalmente mantener una ganancia estable en el mercado real.

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MakeMoneyCoESTB2020

//*********************Notes for continued work***************

//3) add a Table of contents to each section of code

//4) add candle stick pattern considerations to chart

//5) add an input value for DTE range to backtest

//7) add abilit to turn on/off MACD plot

//9)

//************************************************************

//Hello my fellow investors

//After hours of reading, backtesting, and YouTube video watching

//I discovered that 200EMA, VWAP, BB, MACD, and STC

//produce the most consistent results for investment planning.

//This strategy allows you to pick between the aforementioned indicators or layer them together.

//It works on the pricipal of:

//1) Always follow the market trend - buy/sell above/below 200EMA

//2) Follow corporate investing trends - buy/sell above/below VWAP

//3) Apply MACD check - buy--> MACD line above signal line

// and corssover below histogram \\ sell --> MACD line below signal line

// and crossover above histogram.

//4) Check volitility with price against BB limits upper/Sell or lower/buy

//5) When STC crosses about 10 buy and when it drops below 90 sell

//6) Exit position when stop loss is triggered or profit target is hit. BB also provides a parameter to exit positions.

//This code is the product of many hours of hard work on the part of the greater tradingview community. The credit goes to everyone in the community who has put code out there for the greater good.

//Happy Hunting!

//Title

// strategy("WOMBO COMBO: 100/200EMA & VWAP & MACD", shorttitle="WOMBO COMBO", default_qty_type=strategy.percent_of_equity, default_qty_value=1.5, initial_capital=10000,slippage=2, currency=currency.USD, overlay=true)

//define calculations price source

price = input(title="Price Source", defval=close)

//***************************

//Calculate 20/50/100/200EMA

EMAlength = input(title="EMA_Length", defval=200)

EMA=ema(price, EMAlength)

//plot EMA

ColorEMA=EMAlength==200?color.blue:EMAlength==100?color.aqua:EMAlength==50?color.orange:color.red

plot(EMA, title = "EMA", color = ColorEMA)

//*****************************

//calculate VWAP

ColorVWAP = (price > vwap) ? color.lime : color.maroon

plot(vwap, title = "VWAP", color=ColorVWAP, linewidth=2)

//*****************************

//calculate MACD

//define variables for speed

fast = 12, slow = 26

//define parameters to calculate MACD

fastMA = ema(price, fast)

slowMA = ema(price, slow)

//define MACD line

macd = fastMA - slowMA

//define SIGNAL line

signal = sma(macd, 9)

//plot MACD line

//plot(macd, title = "MACD", color=color.orange)

//plot signal line

//plot(signal, title = "Signal", color=color.purple)

//plot histogram

//define histogram colors

//col_grow_above = color.green

//col_grow_below = color.red

//col_fall_above = color.lime

//col_fall_below = color.maroon

//define histogram value

//hist = macd - signal

//plot histogram

//plot(hist, title="Histogram", style=plot.style_columns, color=(hist>=0 ? (hist[1] < hist ? col_grow_above : col_fall_above) : (hist[1] < hist ? col_grow_below : col_fall_below) ), transp=0 )

//***************************************

//Calculate Bollinger Bands

//Define BB input variables

//lengthBB = input(20, minval=1)

//multBB = input(2.0, minval=0.001, maxval=50)

lengthBB = 20

multBB = 2

//define BB average

basisBB = sma(price, lengthBB)

//define BB standar deviation

devBB = multBB * stdev(price, lengthBB)

//define BB upper and lower limits

upperBB = basisBB + devBB

lowerBB = basisBB - devBB

//Plot BB graph

ShowBB = input(title="Show BB", defval="Y", type=input.string, options=["Y", "N"])

transP = (ShowBB=="Y") ? 0 : 100

plot (upperBB, title = "BB Upper Band", color = color.aqua, transp=transP)

plot (basisBB, title = "BB Average", color = color.red, transp=transP)

plot (lowerBB, title = "BB Lower Band", color = color.aqua, transp=transP)

//*************************************************

//Calculate STC

//fastLength = input(title="MACD Fast Length", type=input.integer, defval=12)

//slowLength = input(title="MACD Slow Length", type=input.integer, defval=26)

fastLength = 23

slowLength = 50

cycleLength = input(title="Cycle Length", type=input.integer, defval=10)

//d1Length = input(title="1st %D Length", type=input.integer, defval=3)

//d2Length = input(title="2nd %D Length", type=input.integer, defval=3)

d1Length = 3

d2Length = 3

srcSTC = close

macdSTC = ema(srcSTC, fastLength) - ema(srcSTC, slowLength)

k = nz(fixnan(stoch(macdSTC, macdSTC, macdSTC, cycleLength)))

d = ema(k, d1Length)

kd = nz(fixnan(stoch(d, d, d, cycleLength)))

stc = ema(kd, d2Length)

stc := stc > 100 ? 100 : stc < 0 ? 0 : stc

upperSTC = input(title="Upper STC limit", defval=90)

lowerSTC = input( title="Lower STC limit", defval=10)

ma1length=35

ma1 = ema(close,ma1length)

ma2 = ema(close,EMAlength)

//STCbuy = crossover(stc, lowerSTC) and ma1>ma2 and close>ma1

//STCsell = crossunder(stc, upperSTC) and ma1<ma2 and close<ma1

STCbuy = crossover(stc, lowerSTC)

STCsell = crossunder(stc, upperSTC)

//*************************************************

//Candle stick patterns

//DojiSize = input(0.05, minval=0.01, title="Doji size")

//data=(abs(open - close) <= (high - low) * DojiSize)

//plotchar(data, title="Doji", text='Doji', color=color.white)

data2=(close[2] > open[2] and min(open[1], close[1]) > close[2] and open < min(open[1], close[1]) and close < open )

//plotshape(data2, title= "Evening Star", color=color.red, style=shape.arrowdown, text="Evening\nStar")

data3=(close[2] < open[2] and max(open[1], close[1]) < close[2] and open > max(open[1], close[1]) and close > open )

//plotshape(data3, title= "Morning Star", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Morning\nStar")

data4=(open[1] < close[1] and open > close[1] and high - max(open, close) >= abs(open - close) * 3 and min(close, open) - low <= abs(open - close))

//plotshape(data4, title= "Shooting Star", color=color.red, style=shape.arrowdown, text="Shooting\nStar")

data5=(((high - low)>3*(open -close)) and ((close - low)/(.001 + high - low) > 0.6) and ((open - low)/(.001 + high - low) > 0.6))

//plotshape(data5, title= "Hammer", location=location.belowbar, color=color.white, style=shape.diamond, text="H")

data5b=(((high - low)>3*(open -close)) and ((high - close)/(.001 + high - low) > 0.6) and ((high - open)/(.001 + high - low) > 0.6))

//plotshape(data5b, title= "Inverted Hammer", location=location.belowbar, color=color.white, style=shape.diamond, text="IH")

data6=(close[1] > open[1] and open > close and open <= close[1] and open[1] <= close and open - close < close[1] - open[1] )

//plotshape(data6, title= "Bearish Harami", color=color.red, style=shape.arrowdown, text="Bearish\nHarami")

data7=(open[1] > close[1] and close > open and close <= open[1] and close[1] <= open and close - open < open[1] - close[1] )

//plotshape(data7, title= "Bullish Harami", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nHarami")

data8=(close[1] > open[1] and open > close and open >= close[1] and open[1] >= close and open - close > close[1] - open[1] )

//plotshape(data8, title= "Bearish Engulfing", color=color.red, style=shape.arrowdown, text="Bearish\nEngulfing")

data9=(open[1] > close[1] and close > open and close >= open[1] and close[1] >= open and close - open > open[1] - close[1] )

//plotshape(data9, title= "Bullish Engulfing", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nEngulfling")

upper = highest(10)[1]

data10=(close[1] < open[1] and open < low[1] and close > close[1] + ((open[1] - close[1])/2) and close < open[1])

//plotshape(data10, title= "Piercing Line", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Piercing\nLine")

lower = lowest(10)[1]

data11=(low == open and open < lower and open < close and close > ((high[1] - low[1]) / 2) + low[1])

//plotshape(data11, title= "Bullish Belt", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nBelt")

data12=(open[1]>close[1] and open>=open[1] and close>open)

//plotshape(data12, title= "Bullish Kicker", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nKicker")

data13=(open[1]<close[1] and open<=open[1] and close<=open)

//plotshape(data13, title= "Bearish Kicker", color=color.red, style=shape.arrowdown, text="Bearish\nKicker")

data14=(((high-low>4*(open-close))and((close-low)/(.001+high-low)>=0.75)and((open-low)/(.001+high-low)>=0.75)) and high[1] < open and high[2] < open)

//plotshape(data14, title= "Hanging Man", color=color.red, style=shape.arrowdown, text="Hanging\nMan")

data15=((close[1]>open[1])and(((close[1]+open[1])/2)>close)and(open>close)and(open>close[1])and(close>open[1])and((open-close)/(.001+(high-low))>0.6))

//plotshape(data15, title= "Dark Cloud Cover", color=color.red, style=shape.arrowdown, text="Dark\nCloudCover")

//**********Long & Short Entry Calculations***********************************

//Define countback variable

countback=input(minval=0, maxval=5, title="Price CountBack", defval=0)

//User input for what evaluations to run: EMA, VWAP, MACD, BB

EMA_Y_N=input(defval = "N", title="Run EMA", type=input.string, options=["Y", "N"])

VWAP_Y_N=input(defval = "N", title="Run VWAP", type=input.string, options=["Y", "N"])

MACD_Y_N=input(defval = "N", title="Run MACD", type=input.string, options=["Y", "N"])

BB_Y_N=input(defval = "N", title="Run BB", type=input.string, options=["Y", "N"])

STC_Y_N=input(defval = "Y", title="Run STC", type=input.string, options=["Y", "N"])

//long entry condition

dataHCLB=(iff(STC_Y_N=="Y", STCbuy, true) and iff(EMA_Y_N=="Y", price[countback]>EMA, true) and iff(VWAP_Y_N=="Y", price[countback]>vwap, true) and iff(MACD_Y_N=="Y", crossunder(signal[countback], macd[countback]), true) and iff(MACD_Y_N=="Y", macd[countback]<0, true) and iff(BB_Y_N=="Y", crossunder(price[countback], lowerBB), true))

plotshape(dataHCLB, title= "HC-LB", color=color.lime, style=shape.circle, text="HC-LB")

strategy.entry("HC-Long", strategy.long, comment="HC-Long", when = dataHCLB)

//short entry condition

dataHCSB=(iff(STC_Y_N=="Y", STCsell, true) and iff(EMA_Y_N=="Y", price[countback]<EMA, true) and iff(VWAP_Y_N=="Y", price[countback]<vwap, true) and iff(MACD_Y_N=="Y", crossunder(macd[countback], signal[countback]), true) and iff(MACD_Y_N=="Y", signal[countback]>0, true) and iff(BB_Y_N=="Y", crossover(price[countback], upperBB), true))

plotshape(dataHCSB, title= "HC-SB", color=color.fuchsia, style=shape.circle, text="HC-SB")

strategy.entry("HC-Short", strategy.short, comment="HC-Short", when=dataHCSB)

//******************Exit Conditions******************************

// Profit and Loss Exit Calculations

// User Options to Change Inputs (%)

stopPer = input(5, title='Stop Loss %', type=input.float) / 100

takePer = input(10, title='Take Profit %', type=input.float) / 100

// Determine where you've entered and in what direction

longStop = strategy.position_avg_price * (1 - stopPer)

shortStop = strategy.position_avg_price * (1 + stopPer)

shortTake = strategy.position_avg_price * (1 - takePer)

longTake = strategy.position_avg_price * (1 + takePer)

//exit position conditions and orders

if strategy.position_size > 0 or crossunder(price[countback], upperBB)

strategy.exit(id="Close Long", stop=longStop, limit=longTake)

if strategy.position_size < 0 or crossover(price[countback], lowerBB)

strategy.exit(id="Close Short", stop=shortStop, limit=shortTake)