Stratégie de trading quantitative utilisant plusieurs indicateurs pour identifier les points de retournement de trading

Aperçu

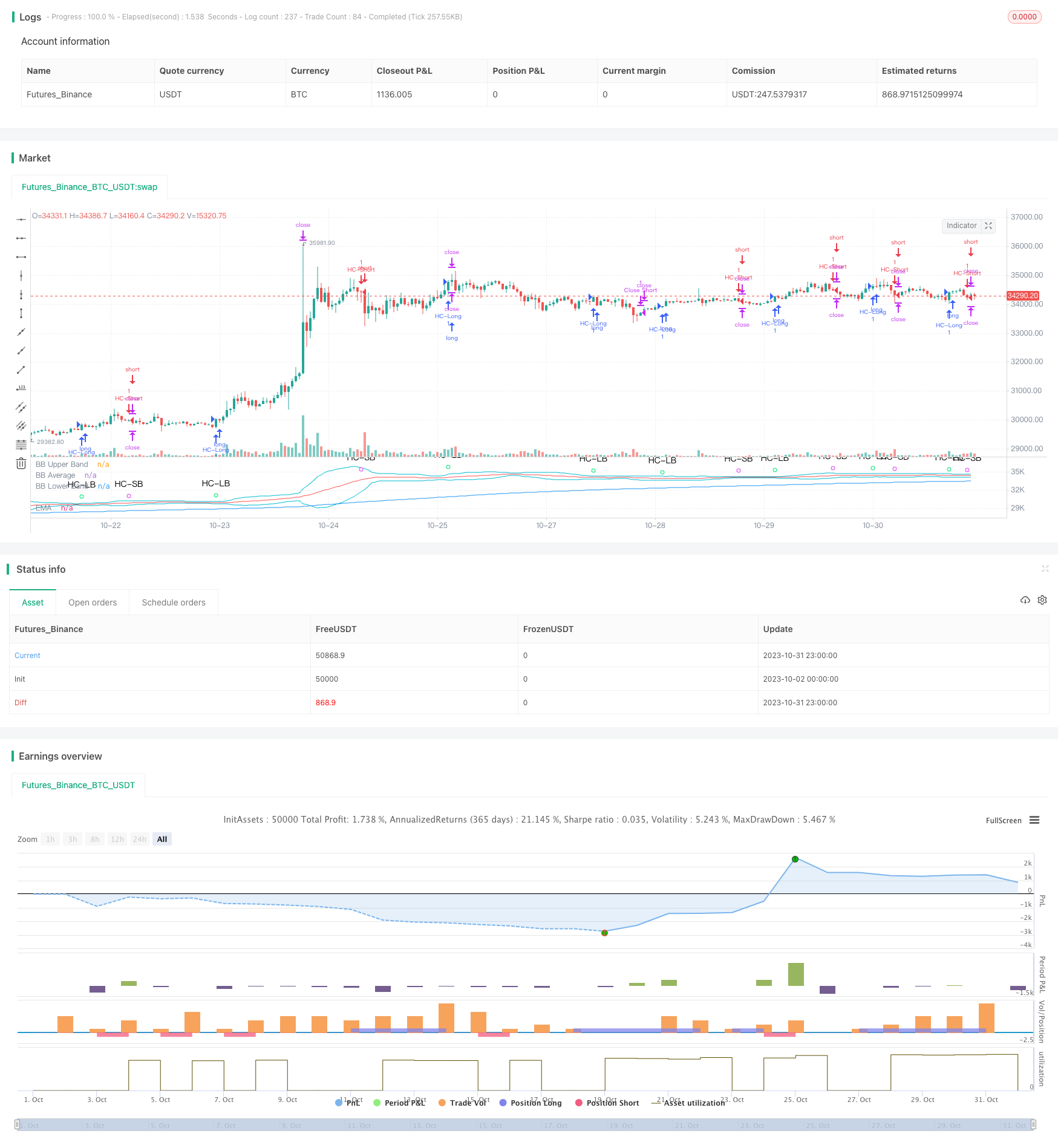

Cette stratégie utilise les cinq principaux indicateurs EMA, VWAP, MACD, Bollinger Bands et Schaff Trend Cycle pour identifier les points de retournement des prix dans une certaine fourchette, émettre des signaux d’achat et de vente. L’avantage de la stratégie est que la combinaison peut être adaptée en fonction des différents indicateurs du marché, réduire la probabilité de faux signaux et améliorer la probabilité de profit.

Principe de stratégie

L’EMA a choisi la direction de la grande tendance et a acheté uniquement dans la direction de la tendance

VWAP juge que les fonds des institutions sont achetés dans le sens où les institutions les achètent

Le MACD détermine la tendance de la courte ligne et la variation de la dynamique, la ligne de signal de rupture du MACD est considérée comme un signal d’achat/vente

Les bandes de Bollinger déterminent si le cours est en survente ou en survente, et considèrent la traversée de la trajectoire descendante comme un signal d’achat/vente.

Schaff Trend Cycle considère que la structure de correction de la courbe à court terme, au-delà des marges hautes et basses, est considérée comme un signal d’achat/vente

L’ordre d’achat/vente est donné lorsque les cinq indicateurs sont en phase.

Définition des points de rupture et des points de rupture, optimisation de la gestion des fonds

Avantages stratégiques

- La combinaison de plusieurs indicateurs réduit la probabilité de faux signaux

La combinaison de plusieurs indicateurs tels que l’EMA, le VWAP, le MACD, le BB et le STC peut être mutuellement vérifiée, ce qui réduit le faux signal généré par un seul indicateur et améliore la fiabilité du signal.

- Indicateur personnalisable

Le choix d’utiliser ou non un indicateur donné permet de combiner les indicateurs en fonction des variétés et des conditions du marché, ce qui rend la stratégie plus ciblée et adaptée.

- Optimisation de la gestion des fonds

Le système de stop loss et de stop-loss permet de limiter les pertes individuelles et de bloquer une partie des bénéfices pour une meilleure gestion des fonds.

- La stratégie est claire

L’ensemble de la stratégie est simple à comprendre et à modifier, grâce à des indicateurs simples et intuitifs, accompagnés d’un code annoté détaillé.

- Une pratique forte

La large utilisation d’indicateurs multiples, le réglage des paramètres raisonnables, peuvent être utilisés directement pour le commerce de disque dur, sans beaucoup d’optimisation, pour obtenir de bons résultats.

Risque stratégique

- Risque de retard dans l’identification des changements

L’EMA, le MACD et d’autres indicateurs ont un certain retard dans l’identification des variations de prix et peuvent manquer le meilleur moment pour acheter.

- Risque de paramètres défectueux

Si les paramètres de l’indicateur sont mal configurés, un grand nombre de faux signaux seront générés et la stratégie ne pourra pas fonctionner correctement.

- Le risque d’une victoire incertaine

Une combinaison de plusieurs indicateurs peut améliorer les chances de succès, mais ne peut pas garantir que chaque transaction soit rentable. Les changements dans l’environnement du marché peuvent entraîner une baisse des chances de succès.

- Le point d’arrêt définit un risque trop petit

Si le stop loss est trop petit, il peut être stoppé en cas de fluctuation normale du prix, ce qui augmente les pertes inutiles.

Orientation de l’optimisation de la stratégie

- Ajout de modèles d’apprentissage automatique pour juger de la fiabilité du signal

Les modèles peuvent être entraînés à évaluer la fiabilité d’un signal multimétrique, à le noter et à réduire les faux signaux.

- Augmentation des indicateurs quantitatifs pour la détection des tendances

L’ajout d’indicateurs quantitatifs tels que l’OBV, qui permettent d’identifier les signes de hausse des prix, améliore la certitude des points d’achat

- Optimisation des stratégies de stop loss

Il est possible d’étudier des stratégies de stop-loss ou de lock-in mobiles plus adaptées à la stratégie et d’optimiser la gestion des fonds.

- Optimisation des paramètres

Optimiser les paramètres de chaque indicateur par une rétroaction plus systématique pour améliorer la stabilité globale de la stratégie.

- Augmentation du nombre de transactions par robots

La connexion de l’API de transaction et la mise en place d’une commande automatique permettent à la stratégie de fonctionner de manière véritablement autonome.

Résumer

Cette stratégie intègre les avantages de plusieurs indicateurs techniques, est claire et pratique. Elle peut être utilisée comme référence de décision pour le trading discrétionnaire ou directement pour le trading algorithmique. Cependant, il est nécessaire d’optimiser l’ajustement en fonction de la variété et de l’environnement du marché, de réduire le risque et de renforcer la stabilité, afin de maintenir une rentabilité stable dans le marché réel.

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © MakeMoneyCoESTB2020

//*********************Notes for continued work***************

//3) add a Table of contents to each section of code

//4) add candle stick pattern considerations to chart

//5) add an input value for DTE range to backtest

//7) add abilit to turn on/off MACD plot

//9)

//************************************************************

//Hello my fellow investors

//After hours of reading, backtesting, and YouTube video watching

//I discovered that 200EMA, VWAP, BB, MACD, and STC

//produce the most consistent results for investment planning.

//This strategy allows you to pick between the aforementioned indicators or layer them together.

//It works on the pricipal of:

//1) Always follow the market trend - buy/sell above/below 200EMA

//2) Follow corporate investing trends - buy/sell above/below VWAP

//3) Apply MACD check - buy--> MACD line above signal line

// and corssover below histogram \\ sell --> MACD line below signal line

// and crossover above histogram.

//4) Check volitility with price against BB limits upper/Sell or lower/buy

//5) When STC crosses about 10 buy and when it drops below 90 sell

//6) Exit position when stop loss is triggered or profit target is hit. BB also provides a parameter to exit positions.

//This code is the product of many hours of hard work on the part of the greater tradingview community. The credit goes to everyone in the community who has put code out there for the greater good.

//Happy Hunting!

//Title

// strategy("WOMBO COMBO: 100/200EMA & VWAP & MACD", shorttitle="WOMBO COMBO", default_qty_type=strategy.percent_of_equity, default_qty_value=1.5, initial_capital=10000,slippage=2, currency=currency.USD, overlay=true)

//define calculations price source

price = input(title="Price Source", defval=close)

//***************************

//Calculate 20/50/100/200EMA

EMAlength = input(title="EMA_Length", defval=200)

EMA=ema(price, EMAlength)

//plot EMA

ColorEMA=EMAlength==200?color.blue:EMAlength==100?color.aqua:EMAlength==50?color.orange:color.red

plot(EMA, title = "EMA", color = ColorEMA)

//*****************************

//calculate VWAP

ColorVWAP = (price > vwap) ? color.lime : color.maroon

plot(vwap, title = "VWAP", color=ColorVWAP, linewidth=2)

//*****************************

//calculate MACD

//define variables for speed

fast = 12, slow = 26

//define parameters to calculate MACD

fastMA = ema(price, fast)

slowMA = ema(price, slow)

//define MACD line

macd = fastMA - slowMA

//define SIGNAL line

signal = sma(macd, 9)

//plot MACD line

//plot(macd, title = "MACD", color=color.orange)

//plot signal line

//plot(signal, title = "Signal", color=color.purple)

//plot histogram

//define histogram colors

//col_grow_above = color.green

//col_grow_below = color.red

//col_fall_above = color.lime

//col_fall_below = color.maroon

//define histogram value

//hist = macd - signal

//plot histogram

//plot(hist, title="Histogram", style=plot.style_columns, color=(hist>=0 ? (hist[1] < hist ? col_grow_above : col_fall_above) : (hist[1] < hist ? col_grow_below : col_fall_below) ), transp=0 )

//***************************************

//Calculate Bollinger Bands

//Define BB input variables

//lengthBB = input(20, minval=1)

//multBB = input(2.0, minval=0.001, maxval=50)

lengthBB = 20

multBB = 2

//define BB average

basisBB = sma(price, lengthBB)

//define BB standar deviation

devBB = multBB * stdev(price, lengthBB)

//define BB upper and lower limits

upperBB = basisBB + devBB

lowerBB = basisBB - devBB

//Plot BB graph

ShowBB = input(title="Show BB", defval="Y", type=input.string, options=["Y", "N"])

transP = (ShowBB=="Y") ? 0 : 100

plot (upperBB, title = "BB Upper Band", color = color.aqua, transp=transP)

plot (basisBB, title = "BB Average", color = color.red, transp=transP)

plot (lowerBB, title = "BB Lower Band", color = color.aqua, transp=transP)

//*************************************************

//Calculate STC

//fastLength = input(title="MACD Fast Length", type=input.integer, defval=12)

//slowLength = input(title="MACD Slow Length", type=input.integer, defval=26)

fastLength = 23

slowLength = 50

cycleLength = input(title="Cycle Length", type=input.integer, defval=10)

//d1Length = input(title="1st %D Length", type=input.integer, defval=3)

//d2Length = input(title="2nd %D Length", type=input.integer, defval=3)

d1Length = 3

d2Length = 3

srcSTC = close

macdSTC = ema(srcSTC, fastLength) - ema(srcSTC, slowLength)

k = nz(fixnan(stoch(macdSTC, macdSTC, macdSTC, cycleLength)))

d = ema(k, d1Length)

kd = nz(fixnan(stoch(d, d, d, cycleLength)))

stc = ema(kd, d2Length)

stc := stc > 100 ? 100 : stc < 0 ? 0 : stc

upperSTC = input(title="Upper STC limit", defval=90)

lowerSTC = input( title="Lower STC limit", defval=10)

ma1length=35

ma1 = ema(close,ma1length)

ma2 = ema(close,EMAlength)

//STCbuy = crossover(stc, lowerSTC) and ma1>ma2 and close>ma1

//STCsell = crossunder(stc, upperSTC) and ma1<ma2 and close<ma1

STCbuy = crossover(stc, lowerSTC)

STCsell = crossunder(stc, upperSTC)

//*************************************************

//Candle stick patterns

//DojiSize = input(0.05, minval=0.01, title="Doji size")

//data=(abs(open - close) <= (high - low) * DojiSize)

//plotchar(data, title="Doji", text='Doji', color=color.white)

data2=(close[2] > open[2] and min(open[1], close[1]) > close[2] and open < min(open[1], close[1]) and close < open )

//plotshape(data2, title= "Evening Star", color=color.red, style=shape.arrowdown, text="Evening\nStar")

data3=(close[2] < open[2] and max(open[1], close[1]) < close[2] and open > max(open[1], close[1]) and close > open )

//plotshape(data3, title= "Morning Star", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Morning\nStar")

data4=(open[1] < close[1] and open > close[1] and high - max(open, close) >= abs(open - close) * 3 and min(close, open) - low <= abs(open - close))

//plotshape(data4, title= "Shooting Star", color=color.red, style=shape.arrowdown, text="Shooting\nStar")

data5=(((high - low)>3*(open -close)) and ((close - low)/(.001 + high - low) > 0.6) and ((open - low)/(.001 + high - low) > 0.6))

//plotshape(data5, title= "Hammer", location=location.belowbar, color=color.white, style=shape.diamond, text="H")

data5b=(((high - low)>3*(open -close)) and ((high - close)/(.001 + high - low) > 0.6) and ((high - open)/(.001 + high - low) > 0.6))

//plotshape(data5b, title= "Inverted Hammer", location=location.belowbar, color=color.white, style=shape.diamond, text="IH")

data6=(close[1] > open[1] and open > close and open <= close[1] and open[1] <= close and open - close < close[1] - open[1] )

//plotshape(data6, title= "Bearish Harami", color=color.red, style=shape.arrowdown, text="Bearish\nHarami")

data7=(open[1] > close[1] and close > open and close <= open[1] and close[1] <= open and close - open < open[1] - close[1] )

//plotshape(data7, title= "Bullish Harami", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nHarami")

data8=(close[1] > open[1] and open > close and open >= close[1] and open[1] >= close and open - close > close[1] - open[1] )

//plotshape(data8, title= "Bearish Engulfing", color=color.red, style=shape.arrowdown, text="Bearish\nEngulfing")

data9=(open[1] > close[1] and close > open and close >= open[1] and close[1] >= open and close - open > open[1] - close[1] )

//plotshape(data9, title= "Bullish Engulfing", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nEngulfling")

upper = highest(10)[1]

data10=(close[1] < open[1] and open < low[1] and close > close[1] + ((open[1] - close[1])/2) and close < open[1])

//plotshape(data10, title= "Piercing Line", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Piercing\nLine")

lower = lowest(10)[1]

data11=(low == open and open < lower and open < close and close > ((high[1] - low[1]) / 2) + low[1])

//plotshape(data11, title= "Bullish Belt", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nBelt")

data12=(open[1]>close[1] and open>=open[1] and close>open)

//plotshape(data12, title= "Bullish Kicker", location=location.belowbar, color=color.lime, style=shape.arrowup, text="Bullish\nKicker")

data13=(open[1]<close[1] and open<=open[1] and close<=open)

//plotshape(data13, title= "Bearish Kicker", color=color.red, style=shape.arrowdown, text="Bearish\nKicker")

data14=(((high-low>4*(open-close))and((close-low)/(.001+high-low)>=0.75)and((open-low)/(.001+high-low)>=0.75)) and high[1] < open and high[2] < open)

//plotshape(data14, title= "Hanging Man", color=color.red, style=shape.arrowdown, text="Hanging\nMan")

data15=((close[1]>open[1])and(((close[1]+open[1])/2)>close)and(open>close)and(open>close[1])and(close>open[1])and((open-close)/(.001+(high-low))>0.6))

//plotshape(data15, title= "Dark Cloud Cover", color=color.red, style=shape.arrowdown, text="Dark\nCloudCover")

//**********Long & Short Entry Calculations***********************************

//Define countback variable

countback=input(minval=0, maxval=5, title="Price CountBack", defval=0)

//User input for what evaluations to run: EMA, VWAP, MACD, BB

EMA_Y_N=input(defval = "N", title="Run EMA", type=input.string, options=["Y", "N"])

VWAP_Y_N=input(defval = "N", title="Run VWAP", type=input.string, options=["Y", "N"])

MACD_Y_N=input(defval = "N", title="Run MACD", type=input.string, options=["Y", "N"])

BB_Y_N=input(defval = "N", title="Run BB", type=input.string, options=["Y", "N"])

STC_Y_N=input(defval = "Y", title="Run STC", type=input.string, options=["Y", "N"])

//long entry condition

dataHCLB=(iff(STC_Y_N=="Y", STCbuy, true) and iff(EMA_Y_N=="Y", price[countback]>EMA, true) and iff(VWAP_Y_N=="Y", price[countback]>vwap, true) and iff(MACD_Y_N=="Y", crossunder(signal[countback], macd[countback]), true) and iff(MACD_Y_N=="Y", macd[countback]<0, true) and iff(BB_Y_N=="Y", crossunder(price[countback], lowerBB), true))

plotshape(dataHCLB, title= "HC-LB", color=color.lime, style=shape.circle, text="HC-LB")

strategy.entry("HC-Long", strategy.long, comment="HC-Long", when = dataHCLB)

//short entry condition

dataHCSB=(iff(STC_Y_N=="Y", STCsell, true) and iff(EMA_Y_N=="Y", price[countback]<EMA, true) and iff(VWAP_Y_N=="Y", price[countback]<vwap, true) and iff(MACD_Y_N=="Y", crossunder(macd[countback], signal[countback]), true) and iff(MACD_Y_N=="Y", signal[countback]>0, true) and iff(BB_Y_N=="Y", crossover(price[countback], upperBB), true))

plotshape(dataHCSB, title= "HC-SB", color=color.fuchsia, style=shape.circle, text="HC-SB")

strategy.entry("HC-Short", strategy.short, comment="HC-Short", when=dataHCSB)

//******************Exit Conditions******************************

// Profit and Loss Exit Calculations

// User Options to Change Inputs (%)

stopPer = input(5, title='Stop Loss %', type=input.float) / 100

takePer = input(10, title='Take Profit %', type=input.float) / 100

// Determine where you've entered and in what direction

longStop = strategy.position_avg_price * (1 - stopPer)

shortStop = strategy.position_avg_price * (1 + stopPer)

shortTake = strategy.position_avg_price * (1 - takePer)

longTake = strategy.position_avg_price * (1 + takePer)

//exit position conditions and orders

if strategy.position_size > 0 or crossunder(price[countback], upperBB)

strategy.exit(id="Close Long", stop=longStop, limit=longTake)

if strategy.position_size < 0 or crossover(price[countback], lowerBB)

strategy.exit(id="Close Short", stop=shortStop, limit=shortTake)