Stratégie de percée de l'oscillation moyenne mobile du double VWAP

Aperçu

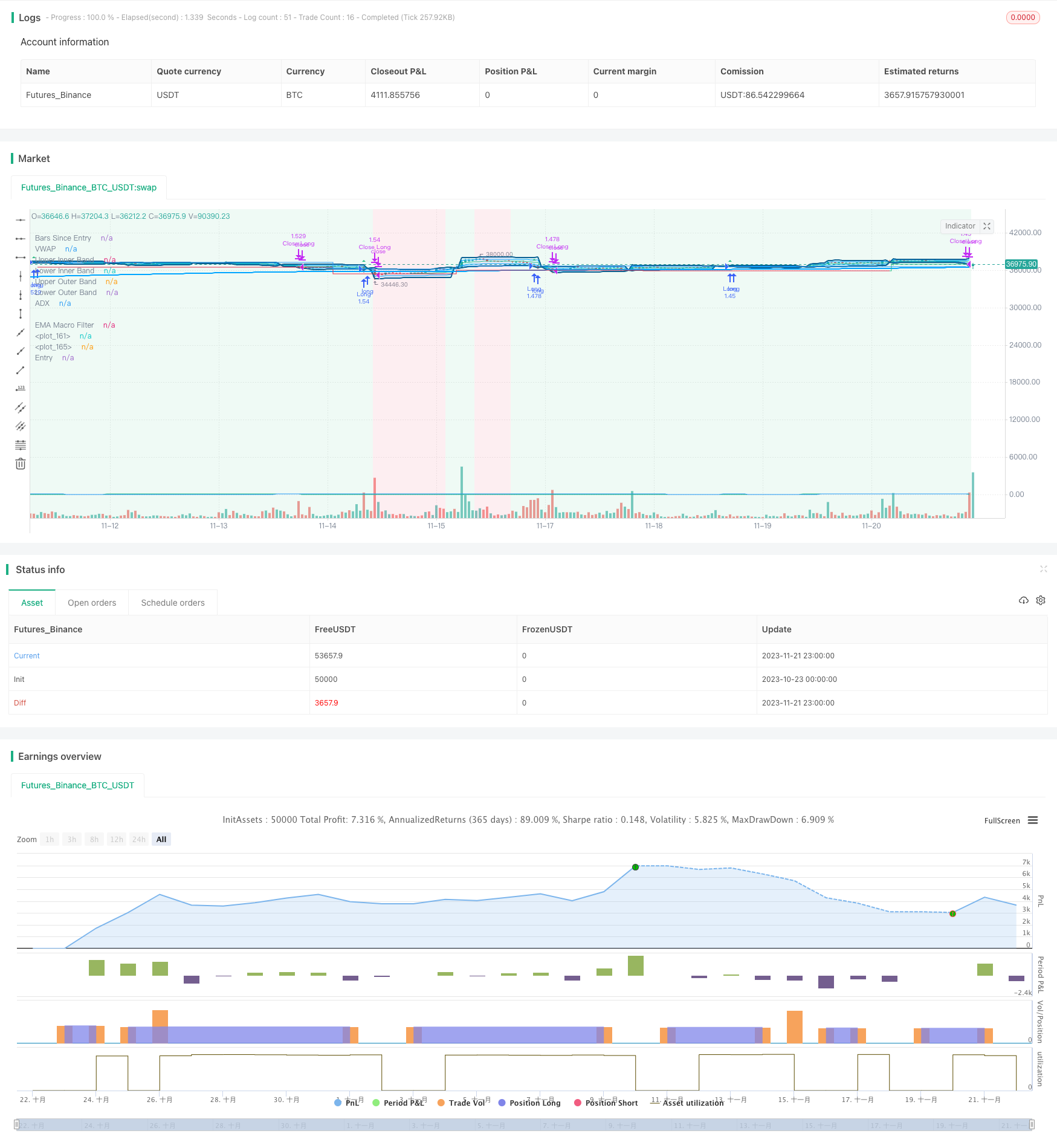

La stratégie de rupture de rupture de la moyenne de VWAP double analyse la tendance du marché par la moyenne de VWAP double pour trouver des opportunités de rupture dans un marché en crise. Elle combine l’indicateur ADX pour déterminer si le marché est en crise et utilise la moyenne de VWAP avec deux écarts de normes différents pour trouver une entrée unique sous la porte de rupture.

Principe de stratégie

La stratégie est principalement composée des éléments suivants:

Paramètres VWAP: calculer la ligne moyenne VWAP et sa bande passante. La bande passante VWAP interne est passée

stDevMultiplierContrôle, par défaut 1; bande passante VWAP externestDevMultiplierLe contrôle et l’acceptation implicites 2.Configuration ADX: calculer les valeurs ADX pour déterminer si le marché est en tremblement de terre. Les valeurs ADX peuvent être configurées pour déterminer si le marché est en tremblement de terre lorsque l’ADX est inférieur à la marge.

Configuration d’entrée: dans un marché en crise, l’entrée se fait lorsque le prix dépasse la bande passante externe VWAP. Le prix de stop-loss et le prix de stop-out peuvent être configurés.

Limiter l’accès: vous pouvez choisir le filtrage EMA de la ligne moyenne ou de la période pour éviter l’accès aux heures non idéales.

Le mode de profit: suivi de la rupture du stop loss ou de la rupture du stop loss. La rupture du VWAP exiting.

La stratégie utilise l’indicateur ADX pour juger de la volatilité et pour rechercher des opportunités d’entrée lorsque le prix franchit la bande passante VWAP. Les bandes VWAP doubles fournissent plus de filtrage pour assurer la force d’entrée. Le suivi des arrêts de perte rend les gains plus stables.

Analyse des avantages

Les bandes VWAP doubles offrent un filtrage supplémentaire pour assurer une entrée rapide.

L’indicateur ADX est un bon indicateur pour juger les marchés en crise et éviter de se tromper dans la tendance.

Le suivi des pertes est un bon moyen d’éviter les emprisonnements

Les paramètres de configuration sont riches et adaptatifs.

Les idées sont claires, faciles à comprendre, à reproduire et à modifier.

Risques et solutions

Une mauvaise configuration des paramètres peut entraîner une entrée trop intense dans le terrain ou une position nulle. L’optimisation des combinaisons de paramètres assure la stabilité de la stratégie.

Le suivi des arrêts peut être trop radical ou conservateur. Le suivi des arrêts peut être ajusté de manière dynamique en combinaison avec les indicateurs de volatilité.

La performance est sensible au moment de la transaction. Elle peut être optimisée par un filtre temporel pour assurer une entrée efficace.

L’indicateur VWAP est sensible aux prix anormaux. En combinaison avec d’autres indicateurs, il confirme la rationalité des prix.

Direction d’optimisation

Modification dynamique de l’amplitude de stop. La position de stop peut être ajustée en temps réel en fonction d’indicateurs tels que le taux de volatilité.

Multiple timeframe Confirmer l’heure d’entrée. Ajouter des tendances et des indicateurs institutionnels de plus longue durée, afin d’éviter les entrées inverses.

Prendre en compte la gestion des positions. Adapter le pourcentage de positions en fonction de la volatilité et de l’évolution des fonds du compte.

Tester les performances de différents cycles VWAP. La définition du cycle VWAP détermine la période de tenue de la stratégie et peut être optimisée.

Résumer

Les stratégies de rupture de fluctuation linéaire à double VWAP offrent un filtrage d’entrée supplémentaire en utilisant les bandes de VWAP à double VWAP. L’idée de la stratégie est claire et plus facile à mettre en œuvre. La stabilité de la stratégie peut être considérablement améliorée par des moyens tels que l’ajustement des paramètres, l’optimisation des arrêts de perte et la gestion de position.

/*backtest

start: 2023-10-23 00:00:00

end: 2023-11-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © jordanfray

//@version=5

strategy(title="Double VWAP Strategy", overlay=true, scale=scale.none, max_bars_back=500, default_qty_type=strategy.percent_of_equity, default_qty_value=100,initial_capital=100000, commission_type=strategy.commission.percent, commission_value=0.05, backtest_fill_limits_assumption=2)

// Indenting Classs

indent_1 = " "

indent_2 = " "

indent_3 = " "

indent_4 = " "

// Group Titles

group_one_title = "VWAP Settings"

group_two_title = "ADX Settings"

group_three_title = "Entry Settings"

group_four_title = "Limit Entries"

// Input Tips

adx_thresholdToolTip = "The minumn ADX value to allow opening a postion"

adxCancelToolTip= "You can optionally set a different lower value for ADX that will allow entries even if below the trigger threshold."

ocean_blue = color.new(#0C6090,0)

sky_blue = color.new(#00A5FF,0)

green = color.new(#2DBD85,0)

red = color.new(#E02A4A,0)

light_blue = color.new(#00A5FF,90)

light_green = color.new(#2DBD85,90)

light_red = color.new(#E02A4A,90)

light_yellow = color.new(#FFF900,90)

white = color.new(#ffffff,0)

transparent = color.new(#000000,100)

// Strategy Settings - VWAP

var cumVol = 0.

cumVol += nz(volume)

if barstate.islast and cumVol == 0

runtime.error("No volume is provided by the data vendor.")

computeVWAP(src, isNewPeriod, stDevMultiplier) =>

var float sum_src_vol = na

var float sum_vol = na

var float sum_src_src_vol = na

sum_src_vol := isNewPeriod ? src * volume : src * volume + sum_src_vol[1]

sum_vol := isNewPeriod ? volume : volume + sum_vol[1]

sum_src_src_vol := isNewPeriod ? volume * math.pow(src, 2) : volume * math.pow(src, 2) + sum_src_src_vol[1]

_vwap = sum_src_vol / sum_vol

variance = sum_src_src_vol / sum_vol - math.pow(_vwap, 2)

variance := variance < 0 ? 0 : variance

standard_deviation = math.sqrt(variance)

lower_band_value = _vwap - standard_deviation * stDevMultiplier

upper_band_value = _vwap + standard_deviation * stDevMultiplier

[_vwap, lower_band_value, upper_band_value]

var anchor = input.string(defval="Session", title="Anchor Period", options=["Session", "Week", "Month", "Quarter", "Year"], group=group_one_title)

src = input(defval = close, title = "Inner VWAP Source", group=group_one_title)

multiplier_inner = input(defval=1.0, title="Inner Bands Multiplier", group=group_one_title)

multiplier_outer = input(defval=2.0, title="Outer Bands Multiplier", group=group_one_title)

show_bands = true

timeChange(period) =>

ta.change(time(period))

isNewPeriod = switch anchor

"Session" => timeChange("D")

"Week" => timeChange("W")

"Month" => timeChange("M")

"Quarter" => timeChange("3M")

"Year" => timeChange("12M")

=> false

float vwap_val = na

float upper_inner_band_value = na

float lower_inner_band_value = na

float upper_outer_band_value = na

float lower_outer_band_value = na

[inner_vwap, inner_bottom, inner_top] = computeVWAP(src, isNewPeriod, multiplier_inner)

[outer_vwap, outer_bottom, outer_top] = computeVWAP(src, isNewPeriod, multiplier_outer)

vwap_val := inner_vwap

upper_inner_band_value := show_bands ? inner_top : na

lower_inner_band_value := show_bands ? inner_bottom : na

upper_outer_band_value := show_bands ? outer_top : na

lower_outer_band_value := show_bands ? outer_bottom : na

plot(vwap_val, title="VWAP", color=green)

upper_inner_band = plot(upper_inner_band_value, title="Upper Inner Band", color=sky_blue)

lower_inner_band = plot(lower_inner_band_value, title="Lower Inner Band", color=sky_blue)

upper_outer_band = plot(upper_outer_band_value, title="Upper Outer Band", linewidth=2, color=ocean_blue)

lower_outer_band = plot(lower_outer_band_value, title="Lower Outer Band", linewidth=2, color=ocean_blue)

fill(upper_outer_band, lower_outer_band, title="VWAP Bands Fill", color= show_bands ? light_blue : na)

// ADX Settings

adx_len = input.int(defval=14, title="ADX Smoothing", group=group_two_title)

di_len = input.int(defval=14, title="DI Length", group=group_two_title)

adx_threshold = input.int(defval=40, title="ADX Threshold", group=group_two_title, tooltip=adx_thresholdToolTip)

dirmov(len) =>

up = ta.change(high)

down = -ta.change(low)

plus_dm = na(up) ? na : (up > down and up > 0 ? up : 0)

minus_dm = na(down) ? na : (down > up and down > 0 ? down : 0)

true_range = ta.rma(ta.tr, len)

plus = fixnan(100 * ta.rma(plus_dm, len) / true_range)

minus = fixnan(100 * ta.rma(minus_dm, len) / true_range)

[plus, minus]

adx(di_len, adx_len) =>

[plus, minus] = dirmov(di_len)

sum = plus + minus

adx = 100 * ta.rma(math.abs(plus - minus) / (sum == 0 ? 1 : sum), adx_len)

adx_val = adx(di_len, adx_len)

plot(adx_val, title="ADX")

// Entry Settings

stop_loss_val = input.float(defval=2.0, title="Stop Loss (%)", step=0.1, group=group_three_title)/100

take_profit_val = input.float(defval=6.0, title="Take Profit (%)", step=0.1, group=group_three_title)/100

long_entry_limit_lookback = input.int(defval=1, title="Long Entry Limit Lookback", minval=1, step=1, group=group_three_title)

short_entry_limit_lookback = input.int(defval=1, title="Short Entry Limit Lookback", minval=1, step=1, group=group_three_title)

limit_order_long_price = ta.lowest(close, long_entry_limit_lookback)

limit_order_short_price = ta.highest(close, short_entry_limit_lookback)

start_trailing_after = input.float(defval=3, title="Start Trailing After (%)", step=0.1, group=group_three_title)/100

trail_behind = input.float(defval=2, title="Trail Behind (%)", step=0.1, group=group_three_title)/100

close_early_if_crosses_outter_band = input.bool(defval=false, title="Close early if price crosses outer VWAP band")

// Limit Entries

enableEmaFilter = input.bool(defval=true, title="Use EMA Filter", group=group_four_title)

emaFilterTimeframe = input.timeframe(defval="", title=indent_4+"Timeframe", group=group_four_title)

emaFilterLength = input.int(defval=300, minval=1, step=10, title=indent_4+"Length", group=group_four_title)

emaFilterSource = input.source(defval=hl2, title=indent_4+"Source", group=group_four_title)

ema_filter = ta.ema(emaFilterSource, emaFilterLength)

ema_filter_smoothed = request.security(syminfo.tickerid, emaFilterTimeframe, ema_filter[barstate.isrealtime ? 1 : 0], gaps=barmerge.gaps_on)

plot(enableEmaFilter ? ema_filter_smoothed: na, title="EMA Macro Filter", linewidth=2, color=sky_blue, editable=true)

useTimeFilter = input.bool(defval=false, title="Use Time Session Filter", group=group_four_title)

withinTime = true

long_start_trailing_val = strategy.position_avg_price + (strategy.position_avg_price * start_trailing_after)

short_start_trailing_val = strategy.position_avg_price - (strategy.position_avg_price * start_trailing_after)

long_trail_behind_val = close - (strategy.position_avg_price * (trail_behind/100))

short_trail_behind_val = close + (strategy.position_avg_price * (trail_behind/100))

currently_in_a_long_postion = strategy.position_size > 0

currently_in_a_short_postion = strategy.position_size < 0

long_profit_target = strategy.position_avg_price * (1 + take_profit_val)

long_stop_loss = strategy.position_avg_price * (1.0 - stop_loss_val)

short_profit_target = strategy.position_avg_price * (1 - take_profit_val)

short_stop_loss = strategy.position_avg_price * (1 + stop_loss_val)

bars_since_entry = currently_in_a_long_postion or currently_in_a_short_postion ? bar_index - strategy.opentrades.entry_bar_index(strategy.opentrades - 1) + 1 : 5

plot(bars_since_entry, editable=false, title="Bars Since Entry", color=green)

long_run_up = ta.highest(high, bars_since_entry)

long_trailing_stop = currently_in_a_long_postion and bars_since_entry > 0 and long_run_up > long_start_trailing_val ? long_run_up - (long_run_up * trail_behind) : long_stop_loss

//long_run_up_line = plot(long_run_up, style=plot.style_stepline, editable=false, color=currently_in_a_long_postion ? green : transparent)

long_trailing_stop_line = plot(long_trailing_stop, style=plot.style_stepline, editable=false, color=currently_in_a_long_postion ? long_trailing_stop > strategy.position_avg_price ? green : red : transparent)

short_run_up = ta.lowest(low, bars_since_entry)

short_trailing_stop = currently_in_a_short_postion and bars_since_entry > 0 and short_run_up < short_start_trailing_val ? short_run_up + (short_run_up * trail_behind) : short_stop_loss

//short_run_up_line = plot(short_run_up, style=plot.style_stepline, editable=false, color=currently_in_a_short_postion ? green : transparent)

short_trailing_stop_line = plot(short_trailing_stop, style=plot.style_stepline, editable=false, color=currently_in_a_short_postion ? short_trailing_stop < strategy.position_avg_price ? green : red : transparent)

// Conditions

adx_is_below_threshold = adx_val < adx_threshold

price_crossed_down_VWAP_lower_outer_band = ta.crossunder(low, lower_outer_band_value)

price_closed_above_VWAP_lower_outer_band = close > lower_outer_band_value

price_crossed_up_VWAP_upper_outer_band = ta.crossover(high,upper_outer_band_value)

price_closed_below_VWAP_upper_outer_band = close < upper_outer_band_value

price_above_ema_filter = close > ema_filter_smoothed

price_below_ema_filter = close < ema_filter_smoothed

//Trade Restirctions

no_trades_allowed = not withinTime or not adx_is_below_threshold

// Enter trades when...

long_conditions_met = enableEmaFilter ? price_above_ema_filter and not currently_in_a_long_postion and withinTime and adx_is_below_threshold and price_crossed_down_VWAP_lower_outer_band and price_closed_above_VWAP_lower_outer_band : not currently_in_a_long_postion and withinTime and adx_is_below_threshold and price_crossed_down_VWAP_lower_outer_band and price_closed_above_VWAP_lower_outer_band

short_conditions_met = enableEmaFilter ? price_below_ema_filter and not currently_in_a_short_postion and withinTime and adx_is_below_threshold and price_crossed_up_VWAP_upper_outer_band and price_closed_below_VWAP_upper_outer_band : not currently_in_a_short_postion and withinTime and adx_is_below_threshold and price_crossed_up_VWAP_upper_outer_band and price_closed_below_VWAP_upper_outer_band

plotshape(long_conditions_met ? close : na, title="Long Entry Symbol", color=green, style=shape.triangleup, location=location.abovebar)

plotshape(short_conditions_met ? close : na, title="Short Entry Symbol", color=red, style=shape.triangledown, location=location.belowbar)

// Take Profit When...

price_closed_below_short_trailing_stop = ta.cross(close, short_trailing_stop)

price_hit_short_entry_profit_target = low > short_profit_target

price_closed_above_long_entry_trailing_stop = ta.cross(close, long_trailing_stop)

price_hit_long_entry_profit_target = high > long_profit_target

long_position_take_profit = close_early_if_crosses_outter_band ? price_crossed_up_VWAP_upper_outer_band or price_closed_above_long_entry_trailing_stop or price_hit_long_entry_profit_target : price_closed_above_long_entry_trailing_stop or price_hit_long_entry_profit_target

short_position_take_profit = close_early_if_crosses_outter_band ? price_crossed_down_VWAP_lower_outer_band or price_closed_below_short_trailing_stop or price_hit_short_entry_profit_target : price_closed_below_short_trailing_stop or price_hit_short_entry_profit_target

// Cancel limir order if...

cancel_long_condition = false

cancel_short_condition = false

// Long Entry

strategy.entry(id="Long", direction=strategy.long, limit=limit_order_long_price, when=long_conditions_met)

strategy.cancel(id="Cancel Long", when=cancel_long_condition)

strategy.exit(id="Close Long", from_entry="Long", stop=long_trailing_stop, limit=long_profit_target, when=long_position_take_profit)

// Short Entry

strategy.entry(id="Short", direction=strategy.short, limit=limit_order_short_price, when=short_conditions_met)

strategy.cancel(id="Cancel Short", when=cancel_short_condition)

strategy.exit(id="Close Short", from_entry="Short", stop=short_trailing_stop, limit=short_profit_target, when=short_position_take_profit)

entry = plot(strategy.position_avg_price, editable=false, title="Entry", style=plot.style_stepline, color=currently_in_a_long_postion or currently_in_a_short_postion ? color.blue : transparent, linewidth=1)

fill(entry,long_trailing_stop_line, editable=false, color=currently_in_a_long_postion ? long_trailing_stop > strategy.position_avg_price ? light_green : light_red : transparent)

fill(entry,short_trailing_stop_line, editable=false, color=currently_in_a_short_postion ? short_trailing_stop < strategy.position_avg_price ? light_green : light_red : transparent)

bgcolor(title="No Trades Allowed", color=no_trades_allowed ? light_red : light_green)