सिंगल मूविंग एवरेज क्रॉसिंग बोलिंगर बैंड रणनीति

निर्माण तिथि:

2023-12-22 14:10:14

अंत में संशोधित करें:

2023-12-22 14:10:14

कॉपी:

1

क्लिक्स:

492

1

ध्यान केंद्रित करना

1237

समर्थक

अवलोकन

यह रणनीति एकल-समानता रेखा और ब्रिन बैंड संकेतक पर आधारित है, जब कीमत ब्रिन बैंड को पार करती है, तो खरीद या बेचने के लिए कार्रवाई की जाती है। साथ ही, एक समानता रेखा की दिशा का आकलन करने के लिए, केवल तभी खरीदा जाता है जब औसत रेखा ऊपर जाती है, और जब औसत रेखा नीचे जाती है, तो बेच दिया जाता है।

रणनीति सिद्धांत

इस रणनीति को मुख्य रूप से निम्नलिखित मापदंडों के आधार पर आंका गया हैः

- औसत रेखा ((SMA): CLOSE समापन मूल्य के लिए एक सरल चलती औसत की गणना करें, जो मूल्य प्रवृत्ति को दर्शाता है।

- ब्रिन पट्टी पर चढ़ना: यह ऊर्ध्वाधर कोण प्रतिरोध रेखा को दर्शाता है, और इसे तोड़ना एक मजबूत ब्रेक को दर्शाता है

- ब्रिन बैंड डाउन ट्रैकः यह समर्थन रेखा को दर्शाता है और इसे तोड़ने से रुझान में बदलाव की संभावना होती है।

ये हैं ट्रेडिंग के संकेत

- खरीदें सिग्नलः खरीदें जब समापन मूल्य बुरिन बैंड को पार कर जाता है और औसत बढ़ रहा है।

- बेचने का संकेतः जब समापन मूल्य ब्रीज के नीचे गिर जाता है और औसत रेखा नीचे की स्थिति में होती है, तो बेचें।

इस प्रकार, ट्रेंड और ब्रेकआउट के संयोजन से ट्रेडिंग सिग्नल को अधिक विश्वसनीय बनाया जाता है और झूठे ब्रेकआउट से बचा जाता है।

रणनीतिक लाभ

- नियम सरल, स्पष्ट और समझने में आसान हैं।

- औसत रेखा का उपयोग करें और बड़े रुझानों की दिशा का आकलन करें।

- ब्रिन ने स्थानीय ब्रेक पॉइंट का आकलन करने के लिए नीचे की पटरी पर एक ब्रेक सिग्नल को सटीक रूप से पकड़ लिया।

- यह अपेक्षाकृत कम है और अधिकांश लोगों की जोखिम वरीयताओं के अनुरूप है।

रणनीतिक जोखिम

- एकल संकेतक त्रुटि संकेतों के लिए अतिसंवेदनशील हैं, जो कि पैरामीटर को अनुकूलित करके त्रुटि दर को कम कर सकते हैं।

- स्टॉप-लॉस को उचित रूप से समायोजित किया जा सकता है यदि यह बड़े बाजार के झटके का सामना करने में असमर्थ है।

- यदि आप एक विशाल प्रवृत्ति के साथ अधिक लाभ नहीं प्राप्त कर सकते हैं, तो आप स्थिति बढ़ाने पर विचार कर सकते हैं।

रणनीति अनुकूलन

- अधिक किस्मों को अनुकूलित करने के लिए औसत चक्र पैरामीटर को अनुकूलित करें

- अन्य संकेतकों जैसे कि MACD को फ़िल्टर करके, गलत संकेतों को कम करें।

- गतिशील रूप से स्टॉप पॉइंट को समायोजित करें, अधिकतम निकासी को सीमित करें।

- और यह एक ऐसी चीज है जो पैसे के प्रबंधन के विचार से जुड़ी हुई है, जो लाभ और हानि को संतुलित करती है।

संक्षेप

यह रणनीति सामान्य रूप से सरल और व्यावहारिक है और अधिकांश लोगों के लिए उपयुक्त है। कुछ अनुकूलन समायोजनों के साथ, रणनीति को अधिक कठोर बनाया जा सकता है और अधिक बाजार स्थितियों के लिए अनुकूलित किया जा सकता है।

रणनीति स्रोत कोड

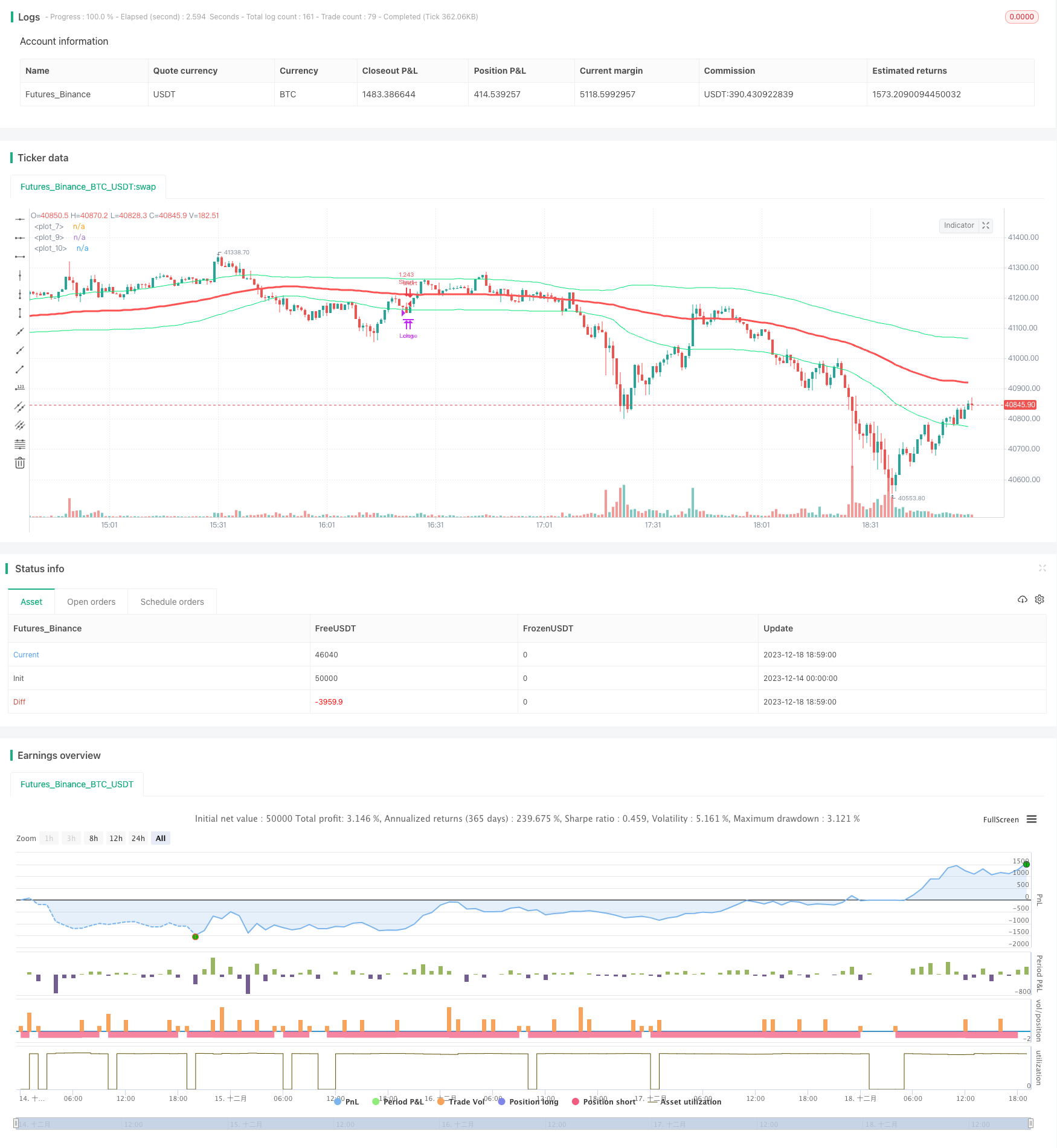

/*backtest

start: 2023-12-14 00:00:00

end: 2023-12-18 19:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title="single sma cross", shorttitle="single sma cross",default_qty_type = strategy.percent_of_equity, default_qty_value = 100,overlay=true,currency="USD")

s=input(title="s",defval=90)

p=input(title="p",type=float,defval=.9,step=.1)

sa=sma(close,s)

plot(sa,color=red,linewidth=3)

band=stdev(close,s)*p

plot(band+sa,color=lime,title="")

plot(-band+sa,color=lime,title="")

// ===Strategy Orders============================================= ========

inpTakeProfit = input(defval = 0, title = "Take Profit", minval = 0)

inpStopLoss = input(defval = 0, title = "Stop Loss", minval = 0)

inpTrailStop = input(defval = 0, title = "Trailing Stop Loss", minval = 0)

inpTrailOffset = input(defval = 0, title = "Trailing Stop Loss Offset", minval = 0)

useTakeProfit = inpTakeProfit >= 1 ? inpTakeProfit : na

useStopLoss = inpStopLoss >= 1 ? inpStopLoss : na

useTrailStop = inpTrailStop >= 1 ? inpTrailStop : na

useTrailOffset = inpTrailOffset >= 1 ? inpTrailOffset : na

longCondition = crossover(close,sa+band) and rising(sa,5)

shortCondition = crossunder(close,sa-band) and falling(sa,5)

crossmid = cross(close,sa)

strategy.entry(id = "Long", long=true, when = longCondition)

strategy.close(id = "Long", when = shortCondition)

strategy.entry(id = "Short", long=false, when = shortCondition)

strategy.close(id = "Short", when = longCondition)

strategy.exit("Exit Long", from_entry = "Long", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset, when=crossmid)

strategy.exit("Exit Short", from_entry = "Short", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset, when=crossmid)