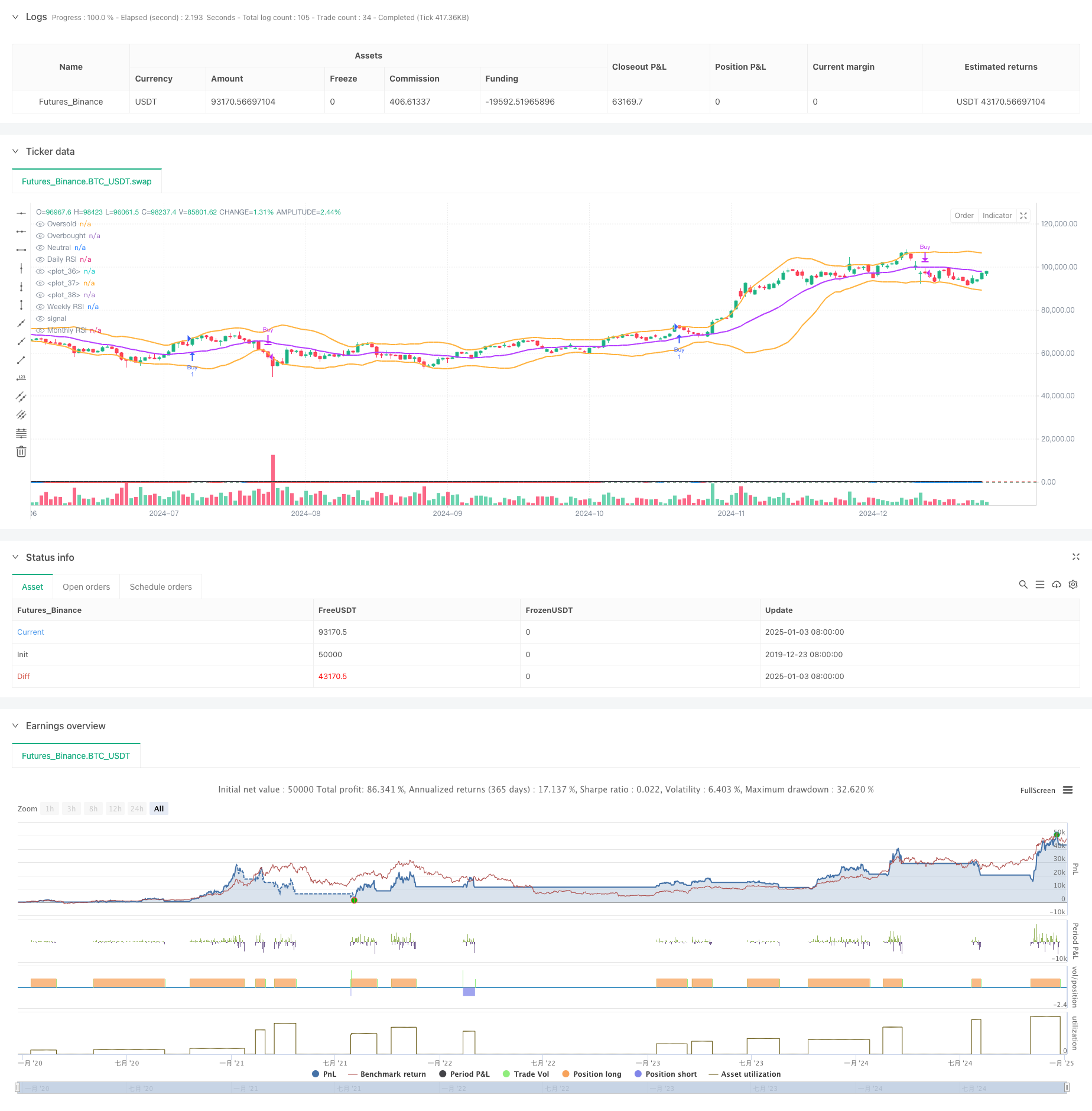

概要

この戦略は、主に指数移動平均 (EMA)、スーパートレンド、ボリンジャーバンド、相対力指数 (RSI) の包括的な分析に基づいて、複数の指標を組み合わせた複合取引システムです。この戦略のコアロジックは、EMA とスーパートレンドを中心に取引シグナルを構築し、ボリンジャーバンドと RSI を組み合わせて市場のボラティリティとモメンタムの補助的な判断を提供します。取引システムは、日次、週次、月次を含む複数期間の RSI 分析を使用して、取引の決定にさらに包括的な市場の視点を提供します。

戦略原則

この戦略では、多層テクニカル指標の組み合わせを使用して、市場のトレンドとボラティリティの機会を捉えます。

- トリプルEMA(13、34、100)を使用してトレンド追跡システムを確立し、移動平均クロスオーバーとポジション関係によってトレンドの方向を決定します。

- スーパートレンドインジケーターをトレンド確認とストップロスの参照として統合する

- ADXインジケーターを使用して強いトレンド市場をスクリーニングし、トレンドの強さのしきい値を25に設定します。

- ボリンジャーバンド(20,2)を使用して価格変動を監視する

- 3期間RSI(14)を使用して市場の買われ過ぎと売られ過ぎの状況を分析する

取引シグナルの発動条件:

- ロングエントリー: スーパートレンドがロングに転じる + EMA13 が EMA34 を横切る + 価格が EMA100 を上回る + ADX>25

- ショートエントリー: スーパートレンドがロングに転じる + EMA13 が EMA34 を下回る + 価格が EMA100 を下回る + ADX>25

- 終値シグナル: 価格がスーパートレンドを横切ったら、対応するポジションを終了します。

戦略的優位性

- 複数のテクニカル指標を統合することで、より信頼性の高い取引シグナルが提供され、誤ったシグナルが効果的に削減されます。

- トリプルEMAシステムは、異なる期間のトレンド特性を完全に把握できます。

- ADXインジケーターの導入により、強いトレンドの市場でのみ取引できるようになります。

- 複数期間のRSI分析は、市場の勢いをより包括的に評価します。

- スーパートレンドインジケーターは客観的なストップロスポジションの参照を提供します

- ボリンジャーバンドの統合により、市場のボラティリティと潜在的なブレイクアウトの機会を判断するのに役立ちます。

戦略リスク

- 複数のインジケーターシステムにより信号の遅れが生じ、エントリーのタイミングに影響する可能性がある

- 不安定な市場では、誤ったブレイクアウトシグナルが頻繁に発生する可能性がある

- 固定ADXしきい値は、異なる市場環境では一貫性のない動作をする可能性があります。

- 急激かつ劇的な市場変動は、不当なストップロスの設定につながる可能性がある。 リスク管理の提案:

- さまざまな市場特性に基づいてADXしきい値を動的に調整する

- ボラティリティ適応型ストップロスメカニズムの導入

- 信号確認としてボリューム分析を追加

戦略最適化の方向性

- 指標パラメータの最適化

- 適応型EMA期間の導入を検討する

- ボラティリティに基づいてスーパートレンド係数を動的に調整する

- さまざまな市場ステージに合わせてボリンジャーバンドのパラメータを最適化

- 信号システムの強化

- 取引シグナルを検証するためにボリューム要因を統合する

- 市場構造分析を追加

- ボラティリティフィルターの導入

- リスク管理の改善

- 動的なストップロスメカニズムを設計する

- 倉庫管理システムの確立

- 取引時間フィルターを追加しました

要約する

この戦略は、複数のテクニカル指標を有機的に組み合わせることで、比較的完全な取引システムを構築します。 EMA とスーパートレンドの組み合わせにより主要な取引シグナルが提供され、ADX スクリーニングにより強いトレンド環境で取引が行われることが保証され、ボリンジャー バンドと RSI の補助分析により追加の市場展望が提供されます。この戦略の主な利点は、信号の信頼性とシステムの整合性ですが、信号の遅延とパラメータの最適化という課題にも直面しています。提案された最適化の方向性を通じて、この戦略は安定性を維持しながら収益性を向上させることが期待されます。

ストラテジーソースコード

/*backtest

start: 2019-12-23 08:00:00

end: 2025-01-04 08:00:00

period: 1d

basePeriod: 1d

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//made by Chinmay

//@version=6

strategy("CJ - Multi1", overlay=true)

// Input for RSI length

rsi_length = input.int(14, title="RSI Length")

// Calculate Daily RSI

daily_rsi = ta.rsi(close, rsi_length)

// Calculate Weekly RSI (using security function to get weekly data)

weekly_rsi = request.security(syminfo.tickerid, "W", ta.rsi(close, rsi_length))

// Calculate Monthly RSI (using security function to get weekly data)

monthly_rsi = request.security(syminfo.tickerid, "M", ta.rsi(close, rsi_length))

// Plot the RSIs

plot(daily_rsi, color=color.blue, title="Daily RSI", linewidth=2)

plot(weekly_rsi, color=color.red, title="Weekly RSI", linewidth=2)

plot(monthly_rsi, color=color.black, title="Monthly RSI", linewidth=2)

// Create horizontal lines at 30, 50, and 70 for RSI reference

hline(30, "Oversold", color=color.green)

hline(70, "Overbought", color=color.red)

hline(50, "Neutral", color=color.gray)

// Bollinger Bands Calculation

bb_length = 20

bb_mult = 2

bb_stddev = ta.stdev(close, bb_length)

bb_average = ta.sma(close, bb_length)

bb_upper = bb_average + bb_mult * bb_stddev

bb_lower = bb_average - bb_mult * bb_stddev

plot(bb_upper, color=color.new(#ffb13b, 0), linewidth=2)

plot(bb_average, color=color.new(#b43bff, 0), linewidth=2)

plot(bb_lower, color=color.new(#ffb13b, 0), linewidth=2)

// Inputs for EMA

ema_L1 = input.int(defval=13, title="EMA Length 1")

ema_L2 = input.int(defval=34, title="EMA Length 2")

ema_L3 = input.int(defval=100, title="EMA Length 3")

adx_level = input.int(defval=25, title="ADX Level")

// Inputs for Supertrend

atr_l = input.int(defval=10, title="ATR Length")

factor = input.float(defval=3.0, title="Supertrend Multiplier")

// Calculate EMA

ema1 = ta.ema(close, ema_L1)

ema2 = ta.ema(close, ema_L2)

ema3 = ta.ema(close, ema_L3)

// Calculate Supertrend

[supertrend, direction] = ta.supertrend(factor, atr_l)

// Calculate ADX and DI

[diplus, diminus, adx] = ta.dmi(14,14)

// Buy and Sell Conditions

buy = direction == -1 and ema1 > ema2 and close > ta.ema(close, 100) and adx > adx_level

short = direction == -1 and ema1 < ema2 and close < ta.ema(close, 100) and adx > adx_level

sell = ta.crossunder(close, supertrend)

cover = ta.crossover(close, supertrend)

// Strategy Logic

if buy

strategy.entry("Buy", strategy.long, comment="Long Entry")

if sell

strategy.close("Buy", comment="Sell Exit")

// Uncomment for Short Strategy

if short

strategy.entry("Short", strategy.short, comment="Short Entry")

if cover

strategy.close("Short", comment="Cover Exit")