개요

“단계 상장 고 유통 통화 쌍 전략”은 고 유통 통화 쌍의 단기 하락 추세를 이용하여 가격이 예상 하락 시 상장 거래를 하여 이익을 취하는 것을 목적으로 한다. 이 전략은 특정 조건에 따라 상장 입장에 들어가고, 동적 입장 규모와 위험 관리 조치를 사용하여 위험을 제어하고 이익을 잠금한다.

이 전략의 주요 내용은 다음과 같습니다.

- 유통이 높은 통화 쌍을 거래 지표로 선택하십시오.

- 가격 하락의 비율 조건에 따라 공백 입장에 들어갑니다.

- 동적으로 포지션 규모를 계산하고, 계정 지분 비율에 따라 위험을 제어한다.

- 스톱 로즈와 스톱 스톱 조건을 설정하여 잠재적인 손실을 제한하고 수익을 잠금합니다.

- 거래 기간이나 가격 변화 조건에 따라 거래에서 탈퇴한다.

전략 원칙

이 전략은 높은 유통 화폐 쌍이 단기간에 하락하는 경향을 이용한다. 가격이 특정 조건을 충족하면 전략은 공시 입장에 들어간다. 구체적인 원칙은 다음과 같다:

- 매번 하나의 거래만 활성화되도록 현재 매매가 없는지 확인합니다.

- 공백 거래의 지속 기간은 7일입니다.

- 가격이 입시 가격에서 예상된 비율 (부정값 30%) 에 도달했을 때, 공시 입장에 들어갑니다.

- 거래당 투자금 분배와 전체 위험을 제어하기 위해 계좌의 이익에 대한 예상 위험 비율에 따라 포지션 크기를 동적으로 계산합니다.

- 스톱로스 및 스톱 스톱 조건을 설정하여, 가격이 불리한 방향으로 움직일 때, 전략은 거래를 종료하여 손실을 최소화합니다. 가격이 유리 방향으로 움직일 때, 전략은 거래를 종료하여 이익을 잠금합니다.

- 거래 기간이나 가격 변화 조건에 따라 거래에서 탈퇴한다.

전략적 이점

- 단기 거래: 이 전략은 높은 유통 통화 쌍의 단기 하락 추세를 포착하는 데 초점을 맞추고, 거래 주기는 상대적으로 짧아 수익 목표를 신속하게 달성하는 데 도움이됩니다.

- 동적 포지션 규모: 계정 권리 이익의 예상 위험 비율에 따라 동적으로 포지션 규모를 계산하여 각 거래의 위험 경로를 효과적으로 제어하고 다양한 시장 조건에 적응합니다.

- 위험 관리: 스톱 로즈와 스톱 스톱 조건을 설정하고, 가격이 불리한 방향으로 움직일 때 거래를 조기에 종료하여 잠재적 인 손실을 최소화합니다. 가격이 유리하게 움직일 때 수익을 잠금하고, 달성 된 수익을 보호합니다.

- 사용 편의성: 이 전략의 조건과 논리는 비교적 간단하며, 이해하기 쉽고 구현하기 쉽고, 다양한 경험 수준의 거래자가 사용할 수 있습니다.

전략적 위험

- 시장 위험: 통화 쌍의 가격 변화는 불확실하며, 단기간에 갑작스러운 사건이나 예상치 못한 움직임이 발생할 수 있으므로 전략이 예상대로 작동하지 않습니다.

- 슬라이드 포인트 위험: 시장의 급격한 변동이나 유동성이 부족한 상황에서 실제 거래 가격은 예상 가격과 차이가 있을 수 있으며, 전략의 수익성에 영향을 미칠 수 있다.

- 파라미터 최적화 위험: 이 전략의 성능은 공백 지속 시간, 가격 하락 비율, 스톱 스톱 비율 등과 같은 여러 파라미터의 선택에 달려 있습니다. 부적절한 파라미터 설정은 전략의 성능이 좋지 않을 수 있습니다.

전략 최적화 방향

- 더 많은 기술 지표를 도입: 입구 및 출구 조건에 이동 평균, 상대 강도 지수 (RSI) 등과 같은 다른 기술 지표를 도입하여 입구 신호의 신뢰성과 정확성을 높인다.

- 최적화 파라미터 선택: 핵심 파라미터에 대한 최적화 및 민감성 분석을 수행합니다. 예를 들어, 공백 지속 시간, 가격 하락 비율, 스톱 스톱 비율 등이 있습니다. 최적의 파라미터 조합을 찾고, 전략의 수익성과 안정성을 향상시킵니다.

- 시장 정서 분석에 참여: 공포 지수 (VIX) 와 거래량과 같은 시장 정서 지표와 결합하여 시장 정서를 판단하고, 시장이 극도로 비관적이거나 거래량이 크게 줄어들 때 진출을 피하고, 전략의 적응성을 향상시킨다.

- 다중 통화 쌍 포트폴리오: 이 전략을 여러 개의 높은 유통 통화 쌍에 적용하여 다원화된 포트폴리오를 구축하여 단일 통화 쌍의 위험을 분산시키고 전체 수익의 안정성을 향상시킵니다.

요약하다

“단계 하위 거래 고 유통 통화 쌍 전략”은 고 유통 통화 쌍의 단기 하락 트렌드를 포착하여 특정 조건에서 하위 거래를하고 동적 위치 규모와 위험 관리 조치를 사용하여 이익을 취하고 위험을 통제합니다. 이 전략의 장점은 단기 거래, 동적 위치 규모 및 간단한 사용 편리성이지만 시장 위험, 슬라이드 포인트 위험 및 파라미터 최적화 위험에 직면합니다. 전략을 추가적으로 최적화하기 위해, 더 많은 기술 지표, 최적화 파라미터 선택, 시장 감정 분석 및 여러 통화 쌍에 적용하는 것을 고려 할 수 있습니다. 지속적인 최적화 및 개선으로, 이 전략은 통화 시장에서 안정적인 이익을 얻을 것으로 예상됩니다.

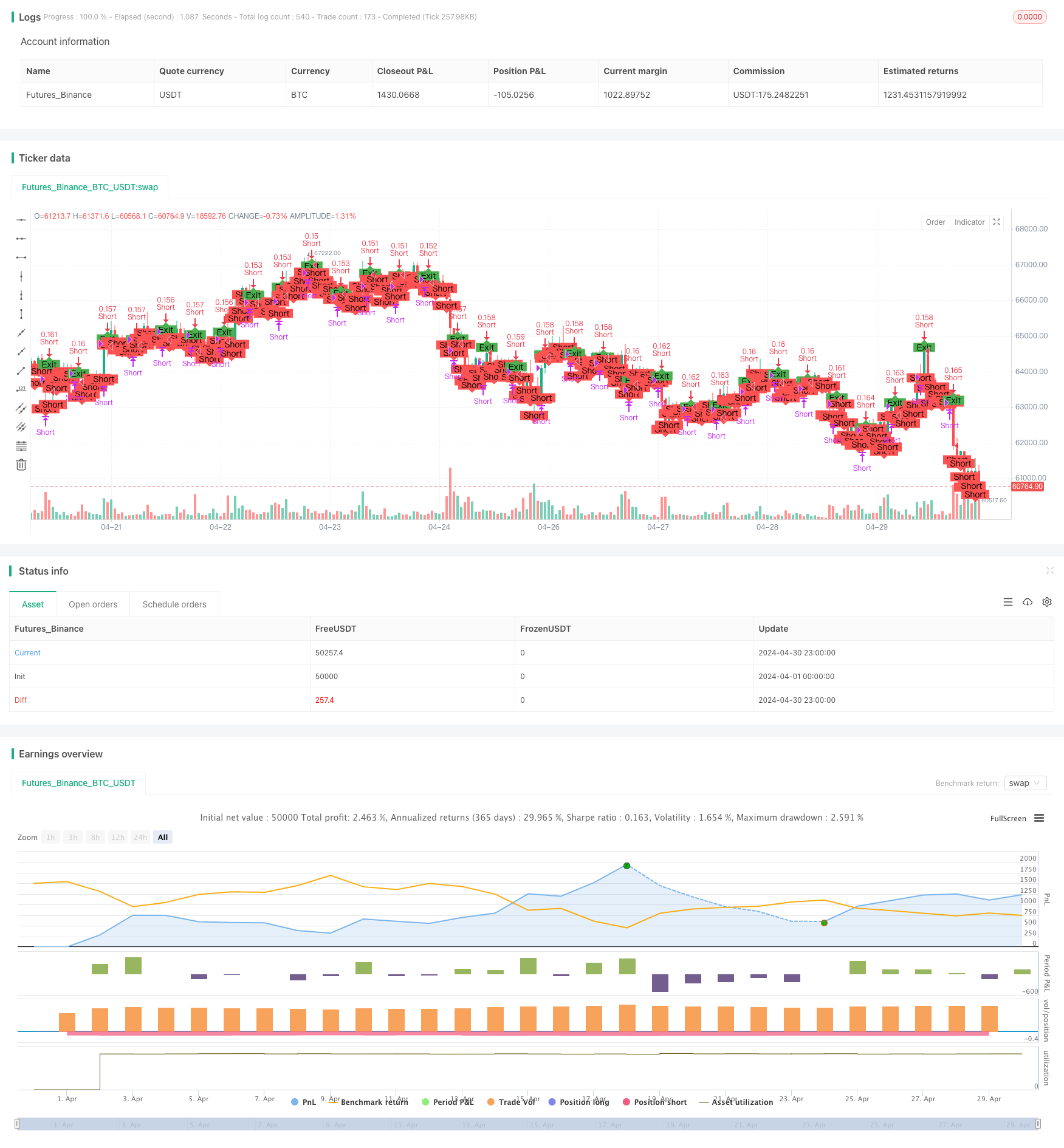

전략 소스 코드

/*backtest

start: 2024-04-01 00:00:00

end: 2024-04-30 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Short High-Grossing Forex Pair", overlay=true)

// Parameters

shortDuration = input.int(7, title="Short Duration (days)")

priceDropPercentage = input.float(30, title="Price Drop Percentage", minval=0, maxval=100)

riskPerTrade = input.float(1, title="Risk per Trade (%)", minval=0.1, maxval=100) / 100 // Risk per trade as a percentage of equity

stopLossPercent = input.float(5, title="Stop Loss Percentage", minval=0) // Stop Loss Percentage

takeProfitPercent = input.float(30, title="Take Profit Percentage", minval=0) // Take Profit Percentage

// Initialize variables

var int shortEnd = na

var float entryPrice = na

// Calculate dynamic position size

equity = strategy.equity

riskAmount = equity * riskPerTrade

pipValue = syminfo.pointvalue

stopLossPips = close * (stopLossPercent / 100)

positionSize = riskAmount / (stopLossPips * pipValue)

// Entry condition: Enter short position at the first bar with calculated position size

if (strategy.opentrades == 0)

strategy.entry("Short", strategy.short, qty=positionSize)

shortEnd := bar_index + shortDuration

entryPrice := close

alert("Entering short position", alert.freq_once_per_bar_close)

// Exit conditions

exitCondition = (bar_index >= shortEnd) or (close <= entryPrice * (1 - priceDropPercentage / 100))

// Stop-loss and take-profit conditions

stopLossCondition = (close >= entryPrice * (1 + stopLossPercent / 100))

takeProfitCondition = (close <= entryPrice * (1 - takeProfitPercent / 100))

// Exit the short position based on the conditions

if (strategy.opentrades > 0 and (exitCondition or stopLossCondition or takeProfitCondition))

strategy.close("Short")

alert("Exiting short position", alert.freq_once_per_bar_close)

// Plot entry and exit points for visualization

plotshape(series=strategy.opentrades > 0, location=location.belowbar, color=color.red, style=shape.labeldown, text="Short")

plotshape(series=strategy.opentrades == 0, location=location.abovebar, color=color.green, style=shape.labelup, text="Exit")

// Add alert conditions

alertcondition(strategy.opentrades > 0, title="Short Entry Alert", message="Entering short position")

alertcondition(strategy.opentrades == 0, title="Short Exit Alert", message="Exiting short position")