Pelaksanaan cepat alat perdagangan kuantitatif separa automatik

Penulis:Kebaikan, Dicipta: 2020-08-30 10:11:02, Dikemas kini: 2023-10-08 19:54:06

Pelaksanaan cepat alat perdagangan kuantitatif separa automatik

Dalam perdagangan niaga hadapan komoditi, arbitraj intertemporari adalah kaedah perdagangan yang biasa. Jenis arbitraj ini tidak bebas risiko. Apabila arah satu sisi penyebaran terus berkembang, kedudukan arbitraj akan berada dalam keadaan kehilangan terapung. Walau bagaimanapun, selagi kedudukan arbitraj dikawal dengan betul, ia masih sangat operasional dan layak.

Dalam artikel ini, kita cuba beralih ke strategi perdagangan lain, dan bukannya membina strategi perdagangan automatik sepenuhnya, kita menyedari alat perdagangan kuantitatif interaktif separa automatik untuk memudahkan arbitrage intertemporari dalam perdagangan niaga hadapan komoditi.

Platform pembangunan kami akan menggunakan platform FMZ Quant. Tumpuan artikel ini adalah bagaimana untuk membina strategi separa automatik dengan fungsi interaktif.

Arbitraj intertemporal adalah konsep yang sangat mudah.

Konsep arbitrase intertemporal

- Kutipan dari Wikipedia

# Strategy Design

The strategy framework is as follows:

Fungsi utama

Walaupun benar.

If(exchange.IO(

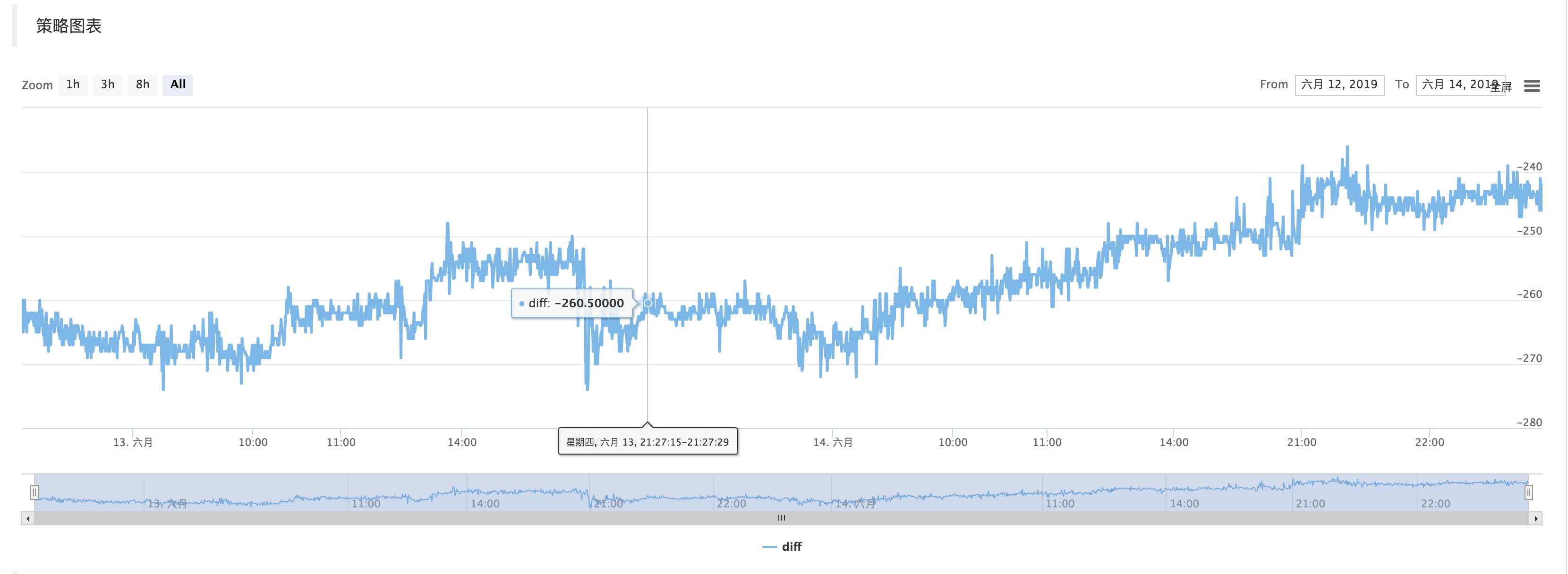

If the CTP protocol is connected properly, then we need to set up the trading contract and then get the market quote. After obtaining the quotes, we can use the FMZ Quant platform build-in "line drawing" library to draw the difference.

Fungsi utama

Walaupun benar.

If(exchange.IO(

LogStatus(_D(),

Get the market data, calculate the difference, and draw the graph to record. let it simply reflects the recent fluctuations in the price difference.

Use the function of "line drawing" library ```$.PlotLine```

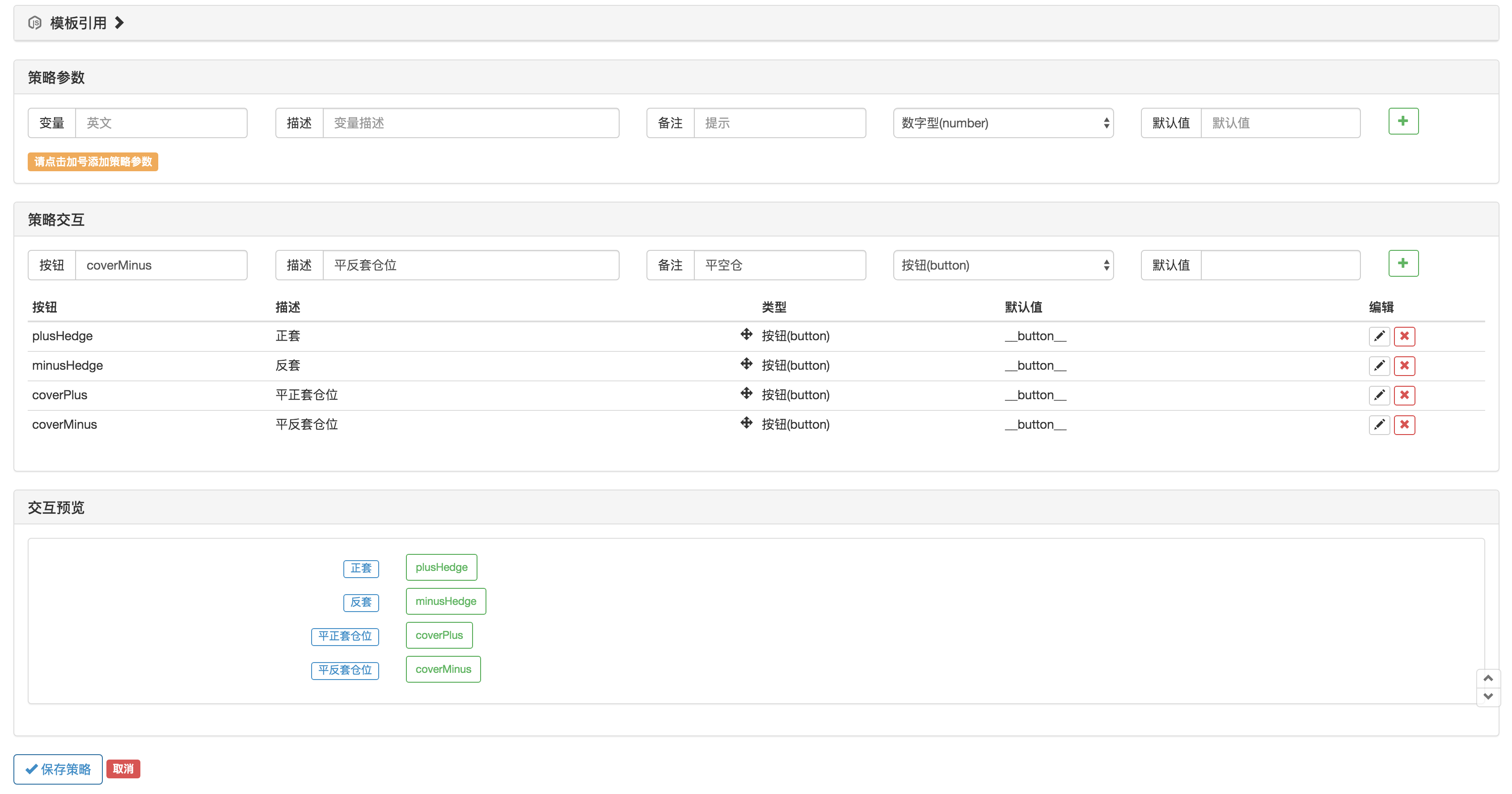

# Interactive part

On the strategy editing page, you can add interactive controls directly to the strategy:

Use the function ```GetCommand``` in the strategy code to capture the command that was sent to the robot after the above strategy control was triggered.

After the command is captured, different commands can be processed differently.

The trading part of the code can be packaged using the "Commodity Futures Trading Class Library" function. First, use ```var q = $.NewTaskQueue()``` to generate the transaction control object ```q``` (declared as a global variable).

var cmd = GetCommand()

jika (cmd) {

jika (cmd ==

- Amalan Kuantitatif Bursa DEX (2) -- Panduan Pengguna Hyperliquid

- DEX Exchange Quantitative Practice ((2) -- Panduan Penggunaan Hyperliquid

- Amalan Kuantitatif Bursa DEX (1) -- Panduan Pengguna dYdX v4

- Pengenalan kepada Arbitraj Lead-Lag dalam Cryptocurrency (3)

- DEX Exchange Quantitative Practice ((1) -- panduan pengguna dYdX v4

- Pengenalan suite Lead-Lag dalam mata wang digital (3)

- Pengenalan kepada Arbitraj Lead-Lag dalam Cryptocurrency (2)

- Pendahuluan mengenai Lead-Lag dalam mata wang digital (2)

- Perbincangan mengenai Penerimaan Isyarat Luaran Platform FMZ: Penyelesaian Lengkap untuk Menerima Isyarat dengan Perkhidmatan Http Terbina dalam Strategi

- Penyelidikan penerimaan isyarat luaran platform FMZ: strategi penyelesaian lengkap untuk penerimaan isyarat perkhidmatan HTTP terbina dalam

- Pengenalan kepada Arbitraj Lead-Lag dalam Cryptocurrency (1)

- Maklumat mengenai strategi algoritma penggandaan mata hadapan

- Secara ringkasnya, mengapa pergerakan aset OKEX tidak boleh dilakukan melalui strategi lindung nilai kontrak.

- Memikirkan pergerakan aset melalui strategi lindung nilai kontrak

- Memperlihatkan dasar penyuntingan untuk memperluaskan perpustakaan kelas tersuai

- Penyelesaian untuk mendapatkan mesej permintaan HTTP dari hos

- Penggunaan pelayan dalam transaksi kuantitatif

- [Perang Milenium] Rasio Pertukaran Bitcoin Kira-kira Strategi 3 Hedging Kupu-kupu

- Strategi Menyimpan Keseimbangan (Strategi Pengajaran)

- RSI2 Strategi Pembalikan Purata menggunakan dalam niaga hadapan

- Futures dan cryptocurrency API penjelasan

- Memperkenalkan penunjuk Aroon

- Kajian awal mengenai Backtesting Strategi Pilihan Mata Wang Digital

- Perbezaan Antara Perdagangan Kuantitatif dan Perdagangan Subjektif

- Strategi Saluran ATR Diimplementasikan di pasaran kripto

- Thermostat Strategi menggunakan di pasaran crypto oleh MyLanguage

- hans123 strategi terobosan intraday

- Strategi Pilihan Mata Wang Digital Mengesahkan Ujian Awal

- TradingViewWebHook penggera disambungkan terus ke robot FMZ

- Tambah jam penggera kepada strategi dagangan

- Strategi lindung nilai kontrak niaga hadapan OKEX dengan menggunakan C++