Sabar ikuti strategi mengikut trend

Gambaran keseluruhan

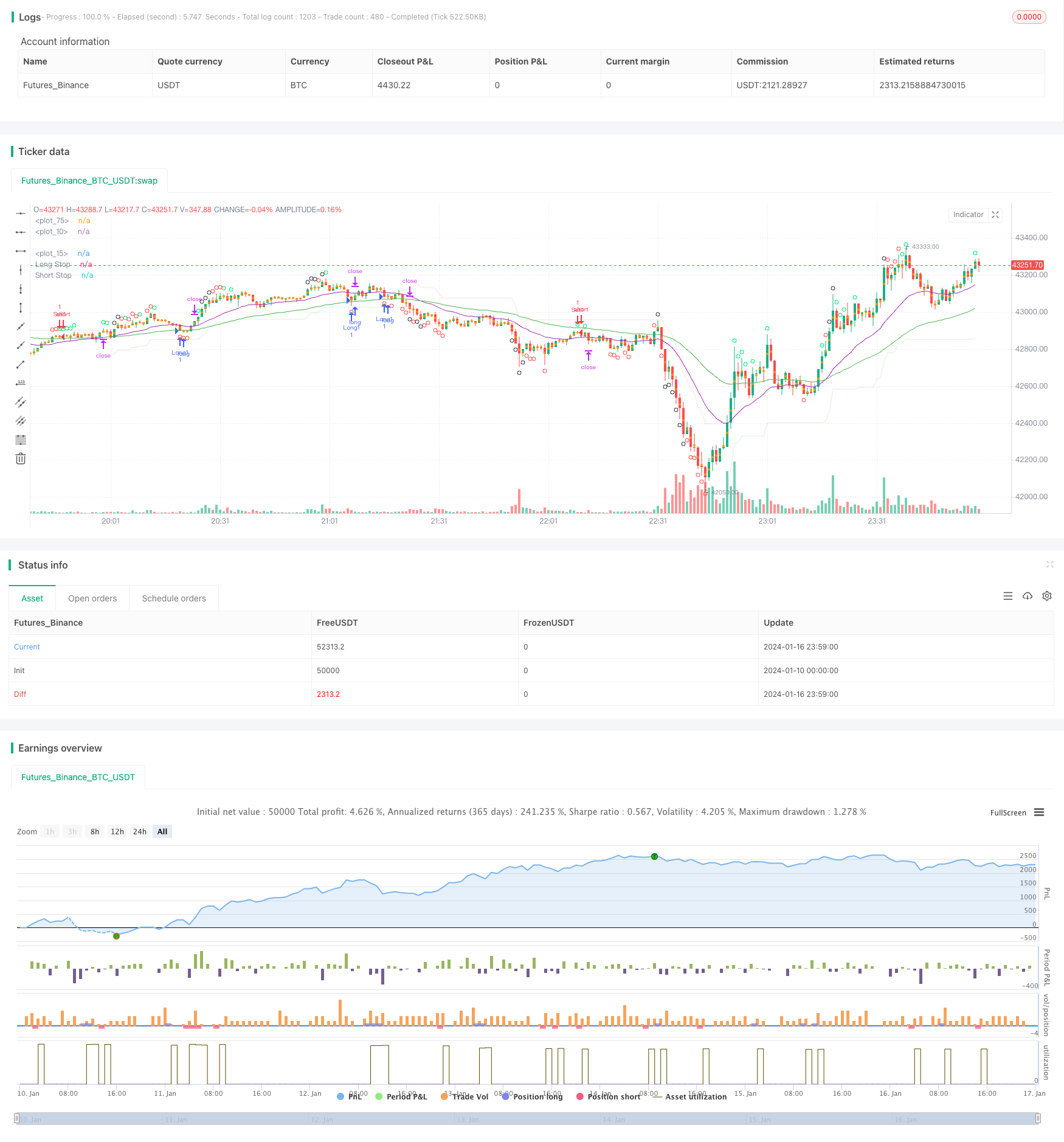

Strategi mengikuti trend dengan kesabaran adalah strategi mengikuti trend. Ia menggunakan gabungan indikator rata-rata bergerak untuk menentukan arah trend, dan menggabungkan indikator CCI yang terlalu banyak untuk menghantar isyarat perdagangan. Strategi ini mengikuti trend besar, dan dapat mengelakkan penyekatan dengan berkesan dalam keadaan goyah.

Prinsip Strategi

Strategi ini menggunakan gabungan EMA 21 dan 55 kitaran untuk menentukan arah trend. EMA jangka pendek ditakrifkan sebagai tren naik apabila di atas EMA jangka panjang, dan EMA jangka pendek ditakrifkan sebagai tren menurun apabila di bawah EMA jangka panjang.

Indeks CCI digunakan untuk menilai keadaan overbought dan oversold. Di atas CCI, garis 100 adalah isyarat oversold yang paling bawah, dan di bawah 100 adalah isyarat oversold yang paling atas. Strategi ini terbahagi kepada tiga tahap kekuatan isyarat perdagangan berdasarkan garis overbought dan oversold yang berbeza dalam indikator CCI.

Apabila menilai sebagai trend menaik, jika petunjuk CCI mengeluarkan isyarat oversell yang kuat di bawah, masuklah ke dalam perdagangan. Apabila menilai sebagai trend menurun, jika petunjuk CCI mengeluarkan isyarat oversell yang kuat di atas, masuklah ke dalam perdagangan kosong.

Barisan hentian ditetapkan sebagai penunjuk SuperTrend, dan sasaran keuntungan ditetapkan sebagai jumlah titik tetap.

Analisis kelebihan

Strategi ini mempunyai kelebihan utama:

- Ikuti Trend Besar dan Jangan Tertipu

- Indeks CCI dapat menentukan titik balik dengan berkesan

- Pendahuluan SuperTrend

- Penangguhan tetap dan penangguhan tetap, risiko boleh dikawal

Analisis risiko

Strategi ini mempunyai risiko utama:

- Kebarangkalian Kesesatan Trend

- Kebarangkalian CCI memberi isyarat palsu

- Kebarangkalian terlampau cetek atau terlampau dalam menyebabkan terlampau banyak

- Kemungkinan bahawa stop-loss tetap tidak dapat terus menjejaki trend

Untuk menghadapi risiko ini, kita boleh mengoptimumkan dengan menyesuaikan parameter kitaran EMA, parameter CCI, dan titik berhenti berhenti. Ia juga perlu untuk memperkenalkan lebih banyak petunjuk untuk mengesahkan isyarat strategi.

Arah pengoptimuman

Strategi ini dioptimumkan untuk:

Uji gabungan lebih banyak indikator untuk mencari penilaian trend yang lebih baik dan indikator pengesahan isyarat.

Menggunakan ATR Dynamic Stop Loss Stop untuk lebih baik mengesan trend dan mengawal risiko.

memperkenalkan model pembelajaran mesin berdasarkan latihan data sejarah untuk menilai kebarangkalian trend.

Sesuaikan dan optimumkan parameter untuk pelbagai jenis.

ringkaskan

Strategi trend track kesabaran secara keseluruhannya adalah strategi trend follow yang sangat praktikal. Ia menggunakan purata bergerak untuk menentukan arah trend besar, penunjuk CCI menemui isyarat titik reversal, dan garis berhenti super trend ditetapkan dengan munasabah.

/*backtest

start: 2024-01-10 00:00:00

end: 2024-01-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © greenmask9

//@version=4

strategy("Patient Trendfollower (7) Strategy", overlay=true)

// 21 EMA

emalength = input(21, title="Short EMA")

emashort = ema(close, emalength)

plot(emashort, color = color.purple, linewidth=1)

// 55 EMA

emalength2 = input(55, title="Long EMA")

ema = ema(close, emalength2)

plot(ema, color = color.green, linewidth=1)

//CCI calculation and inputs

lengthcci = input(20, minval=1, title="Overbought/sold detector period")

src = input(close, title="Overbought/sold detector source")

ma = sma(src, lengthcci)

ccivalue = (src - ma) / (0.015 * dev(src, lengthcci))

//CCI plotting

ccioverbought = input(defval=100, title="Overbought level 1")

ccioverbought2 = input(defval=140, title="Overbought level 2")

ccioverbought3 = input(defval=180, title="Overbought level 3")

ccioversold = input(defval=-100, title="Oversold level 1")

ccioversold2 = input(defval=-140, title="Oversold level 2")

ccioversold3 = input(defval=-180, title="Oversold level 3")

cciOB = (ccivalue >= ccioverbought and ccivalue < ccioverbought2)

plotshape(cciOB, title= "Overbought", location=location.abovebar, color=color.lime, transp=0, style=shape.circle)

cciOS = (ccivalue <= ccioversold and ccivalue > ccioversold2)

plotshape(cciOS, title= "Oversold", location=location.belowbar, color=color.lime, transp=0, style=shape.circle)

cciOB2 = (ccivalue >= ccioverbought2 and ccivalue < ccioverbought3)

plotshape(cciOB2, title= "Overbought", location=location.abovebar, color=color.red, transp=0, style=shape.circle)

cciOS2 = (ccivalue <= ccioversold and ccivalue > ccioversold3)

plotshape(cciOS2, title= "Oversold", location=location.belowbar, color=color.red, transp=0, style=shape.circle)

cciOB3 = (ccivalue >= ccioverbought3)

plotshape(cciOB3, title= "Overbought", location=location.abovebar, color=color.black, transp=0, style=shape.circle)

cciOS3 = (ccivalue <= ccioversold3)

plotshape(cciOS3, title= "Oversold", location=location.belowbar, color=color.black, transp=0, style=shape.circle)

//Supertrend

length = input(title="ATR Period", type=input.integer, defval=55)

mult = input(title="ATR Multiplier", type=input.float, step=0.1, defval=5.0)

wicks = input(title="Take Wicks into Account ?", type=input.bool, defval=true)

illuminate = input(title="Illuminate Trend", type=input.bool, defval=true)

atr = mult * atr(length)

longStop = hl2 - atr

longStopPrev = nz(longStop[1], longStop)

longStop := (wicks ? low[1] : close[1]) > longStopPrev ? max(longStop, longStopPrev) : longStop

shortStop = hl2 + atr

shortStopPrev = nz(shortStop[1], shortStop)

shortStop := (wicks ? high[1] : close[1]) < shortStopPrev ? min(shortStop, shortStopPrev) : shortStop

dir = 1

dir := nz(dir[1], dir)

dir := dir == -1 and (wicks ? high : close) > shortStopPrev ? 1 : dir == 1 and (wicks ? low : close) < longStopPrev ? -1 : dir

longColor = color.new(color.green, 90)

shortColor = color.new(color.red, 90)

noneColor = color.new(color.white, 100)

longStopPlot = plot(dir == 1 ? longStop : na, title="Long Stop", style=plot.style_linebr, linewidth=2, color=longColor)

shortStopPlot = plot(dir == 1 ? na : shortStop, title="Short Stop", style=plot.style_linebr, linewidth=2, color=shortColor)

midPricePlot = plot(ohlc4, title="", style=plot.style_circles, linewidth=0)

longFillColor = illuminate ? (dir == 1 ? longColor : noneColor) : noneColor

shortFillColor = illuminate ? (dir == -1 ? shortColor : noneColor) : noneColor

fill(midPricePlot, longStopPlot, title="Long State Filling", color=longFillColor)

fill(midPricePlot, shortStopPlot, title="Short State Filling", color=shortFillColor)

//entries

uptrend = emashort>ema and dir == 1

upsignal = ccivalue<=ccioversold and ccivalue>ccioversold2

upsignal2 = ccivalue<=ccioversold2 and ccivalue>ccioversold3

upsignal3 = ccivalue<=ccioversold3

downtrend = emashort<ema and dir == -1

downsignal = ccivalue>=ccioverbought and ccivalue<ccioverbought2

downsignal2 = ccivalue>=ccioverbought2 and ccivalue<ccioverbought3

downsignal3 = ccivalue>=ccioverbought3

//adapts to the current bar, I need to save the bars number when the condition for buy was true, static number is spread

spread = input (0.00020, title="Spread")

upstoploss = longStop - spread

downstoploss = shortStop + spread

strategy.initial_capital = 50000

ordersize=floor(strategy.initial_capital/close)

testlong = input(title="Test longs", type=input.bool, defval=true)

testshort = input(title="Test shorts", type=input.bool, defval=true)

//new

degree = input(title="Test level 1 overbought/sold levels", type=input.bool, defval=true)

degree2 = input(title="Test level 2 overbought/sold levels", type=input.bool, defval=false)

degree3 = input(title="Test level 3 overbought/sold levels", type=input.bool, defval=false)

statictarget = input(title="Use static target", type=input.bool, defval=true)

statictargetvalue = input(title="Static target in pips", type=input.integer, defval=400)

//timetrade = input(title="Open trades only withing specified time", type=input.bool, defval=true)

//timtrade = input()

//přidat možnost TP podle ATR a sl podle ATR

buy1 = uptrend and upsignal and strategy.opentrades==0 and testlong and degree

x1 = barssince (buy1)

if (buy1)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long1", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long1" , profit=statictargetvalue,stop=upstoploss[x1])

buy2 = uptrend and upsignal2 and strategy.opentrades==0 and testlong and degree2

x2 = barssince (buy2)

if (buy2)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long2", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long2" , profit=statictargetvalue,stop=upstoploss[x2])

buy3 = uptrend and upsignal3 and strategy.opentrades==0 and testlong and degree3

x3 = barssince (buy3)

if (buy3)

//bodlo by zakázat atrtarget v tomto případě

if (statictarget)

strategy.entry("Long3", strategy.long, ordersize)

strategy.exit( "Exitlong", from_entry="Long3" , profit=statictargetvalue,stop=upstoploss[x3])

sell1 = downtrend and downsignal and strategy.opentrades==0 and testshort and degree

y1 = barssince (sell1)

if (sell1)

if (statictarget)

strategy.entry("Sell1", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell1" , profit=statictargetvalue,stop=downstoploss[y1])

sell2 = downtrend and downsignal2 and strategy.opentrades==0 and testshort and degree2

y2 = barssince (sell2)

if (sell2)

if (statictarget)

strategy.entry("Sell2", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell2" , profit=statictargetvalue,stop=downstoploss[y2])

sell3 = downtrend and downsignal3 and strategy.opentrades==0 and testshort and degree3

y3 = barssince (sell3)

if (sell3)

if (statictarget)

strategy.entry("Sell3", strategy.short, ordersize)

strategy.exit( "Exitshort", from_entry="Sell3" , profit=statictargetvalue,stop=downstoploss[y3])