Penjejak Lembu

Gambaran keseluruhan

Sistem pengesanan pasaran lembu adalah sistem perdagangan mekanikal berdasarkan trend. Ia menggunakan indikator trend pada grafik 4 jam untuk menapis isyarat perdagangan, dan masuk berdasarkan indikator pada grafik 15 minit. Petunjuk utama termasuk RSI, penunjuk rawak dan MACD.

Prinsip

Logik teras sistem ini adalah menggabungkan penunjuk dari pelbagai bingkai masa untuk mengenal pasti arah trend dan masa masuk. Khususnya, RSI, penunjuk rawak dan EMA pada grafik 4 jam harus memenuhi syarat untuk menentukan arah trend keseluruhan. Ini dapat menyaring kebisingan yang paling berkesan.

Kelebihan

- Kombinasi pelbagai bingkai masa yang berkesan untuk menyaring isyarat palsu dan mengenal pasti trend utama

- 15 minit detil untuk mendapatkan masa kemasukan yang lebih tepat

- Portfolio penunjuk menggunakan penunjuk teknologi arus perdana seperti RSI, penunjuk rawak, MACD, mudah difahami, juga mudah dioptimumkan

- Menggunakan kaedah pengurusan risiko yang ketat seperti mStop, Stop Loss, dan Tracking Stop Loss untuk mengawal risiko perdagangan tunggal

Risiko

- Risiko Overtrading. Sistem ini sensitif terhadap jangka masa yang singkat dan mungkin menghasilkan banyak isyarat perdagangan yang menyebabkan overtrading

- Risiko penembusan palsu. Penghakiman indikator jangka pendek mungkin berlaku kesalahan penghakiman, menghasilkan isyarat penembusan palsu

- Risiko kegagalan penunjuk. Penunjuk teknikal mempunyai batasan tertentu dan mungkin gagal dalam keadaan yang melampau

Oleh itu, sistem ini boleh dioptimumkan dalam beberapa aspek:

- Menyesuaikan parameter penunjuk agar lebih sesuai dengan keadaan pasaran yang berbeza

- Meningkatkan syarat penapisan untuk mengurangkan kekerapan transaksi dan mencegah perdagangan berlebihan

- Mengoptimumkan strategi hentian dan hentian yang lebih sesuai dengan pergerakan pasaran

- Uji kombinasi indikator yang berbeza untuk mencari penyelesaian terbaik

ringkaskan

Sistem pengesanan pasaran lembu secara keseluruhan adalah sistem perdagangan mekanikal yang sangat praktikal untuk mengesan trend. Ia menggunakan gabungan indikator dari pelbagai bingkai masa untuk mengenal pasti trend pasaran dan masa masuk utama. Dengan pengaturan parameter yang munasabah dan pengujian pengoptimuman berterusan, sistem ini dapat menyesuaikan diri dengan kebanyakan keadaan pasaran dan mencapai keuntungan yang stabil.

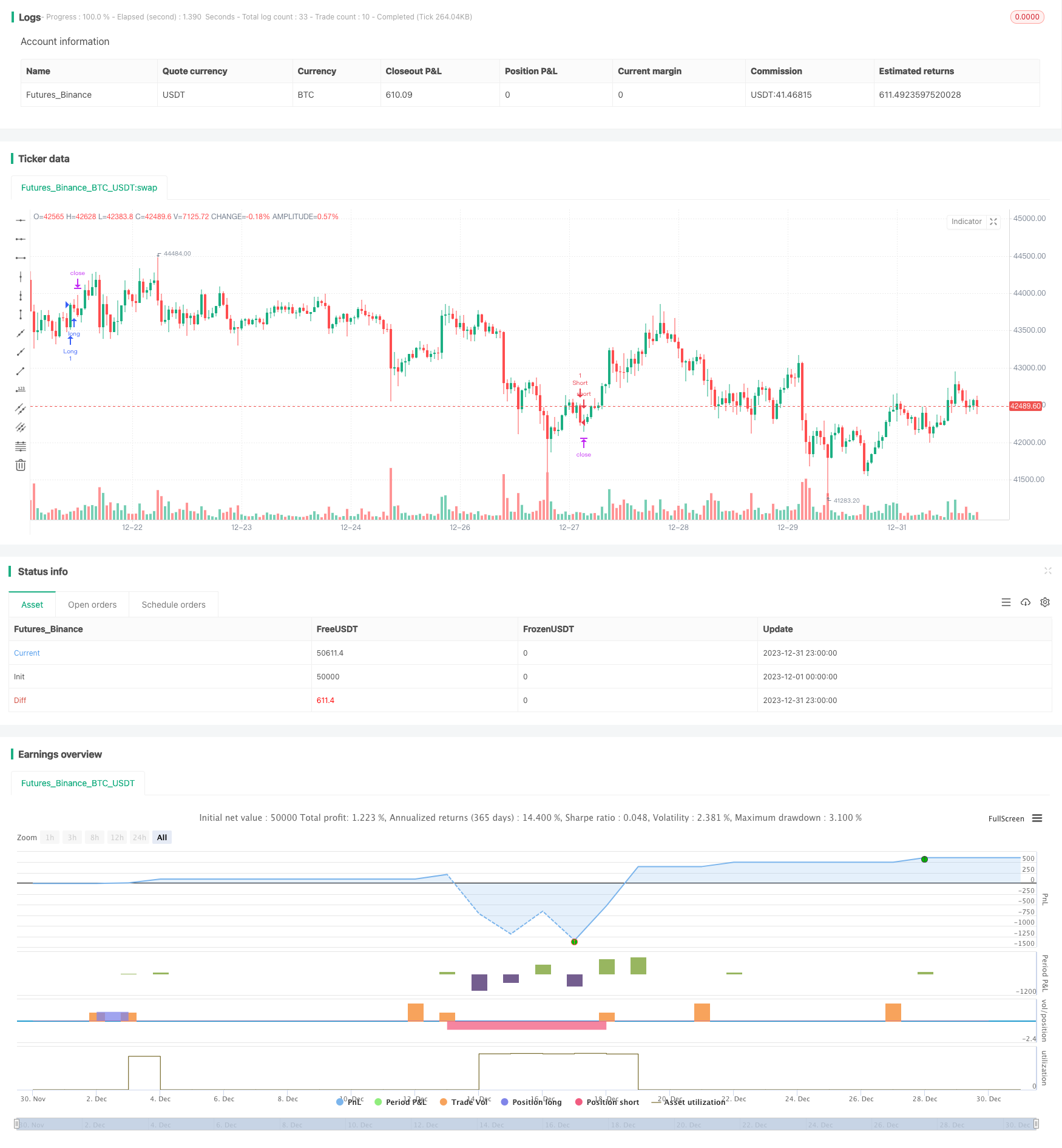

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Cowabunga System from babypips.com", overlay=true)

// 4 Hour Stochastics

length4 = input(162, minval=1, title="4h StochLength"), smoothK4 = input(48, minval=1, title="4h StochK"), smoothD4 = input(48, minval=1, title="4h StochD")

k4 = sma(stoch(close, high, low, length4), smoothK4)

d4 = sma(k4, smoothD4)

//15 min Stoch

length = input(10, minval=1, title="15min StochLength"), smoothK = input(3, minval=1, title="15min StochK"), smoothD = input(3, minval=1, title="15min StochD")

k = sma(stoch(close, high, low, length), smoothK)

d= sma(k, smoothD)

//4 hour RSI

src1 = close, len1 = input(240, minval=1, title="4H RSI Length")

up1 = rma(max(change(src1), 0), len1)

down1 = rma(-min(change(src1), 0), len1)

rsi4 = down1 == 0 ? 100 : up1 == 0 ? 0 : 100 - (100 / (1 + up1 / down1))

//15 min RSI

src = close, len = input(9, minval=1, title="15M RSI Length")

up = rma(max(change(src), 0), len)

down = rma(-min(change(src), 0), len)

rsi15 = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

//MACD Settings

source = close

fastLength = input(12, minval=1, title="MACD Fast"), slowLength=input(26,minval=1, title="MACD Slow")

signalLength=input(9,minval=1, title="MACD Signal")

fastMA = ema(source, fastLength)

slowMA = ema(source, slowLength)

macd = fastMA - slowMA

signal = ema(macd, signalLength)

// Stops and Profit inputs

inpTakeProfit = input(defval = 1000, title = "Take Profit", minval = 0)

inpStopLoss = input(defval = 0, title = "Stop Loss", minval = 0)

inpTrailStop = input(defval = 400, title = "Trailing Stop", minval = 0)

inpTrailOffset = input(defval = 0, title = "Trailing Stop Offset", minval = 0)

// Stops and Profit Targets

useTakeProfit = inpTakeProfit >= 1 ? inpTakeProfit : na

useStopLoss = inpStopLoss >= 1 ? inpStopLoss : na

useTrailStop = inpTrailStop >= 1 ? inpTrailStop : na

useTrailOffset = inpTrailOffset >= 1 ? inpTrailOffset : na

//Specific Time to Trade

myspecifictradingtimes = input('0500-1600', title="My Defined Hours")

longCondition1 = time(timeframe.period, myspecifictradingtimes) != 0

longCondition2 = rsi4 <= 80

longCondition3 = k4 >= d4 and k4 <= 80

longCondition4 = ema(close, 80) >= ema(close, 162)

allLongerLongs = longCondition1 and longCondition2 and longCondition3 and longCondition4

longCondition5 = rsi15 <= 80

longCondition6 = k >= d and k <= 80 and fastMA >= slowMA

longCondition7 = ema(close, 5) >= ema(close, 10)

allLongLongs = longCondition5 and longCondition6 and longCondition7

if crossover(close, ema(close, 5)) and allLongerLongs and allLongLongs

strategy.entry("Long", strategy.long, comment="LongEntry")

shortCondition1 = time(timeframe.period, myspecifictradingtimes) != 0

shortCondition2 = rsi4 >= 20

shortCondition3 = k4 <= d4 and k4 >= 20

shortCondition4 = ema(close, 80) <= ema(close, 162)

allShorterShorts = shortCondition1 and shortCondition2 and shortCondition3 and shortCondition4

shortCondition5 = rsi15 >= 20

shortCondition6 = k <= d and k >= 20 and fastMA <= slowMA

shortCondition7 = ema(close, 5) <= ema(close, 10)

allShortShorts = shortCondition5 and shortCondition6 and shortCondition7

if crossunder(close, ema(close,5)) and allShorterShorts and allShortShorts

strategy.entry("Short", strategy.short, comment="ShortEntry")

strategy.exit("Exit Long", from_entry = "Long", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset)

strategy.exit("Exit Short", from_entry = "Short", profit = useTakeProfit, loss = useStopLoss, trail_points = useTrailStop, trail_offset = useTrailOffset)