Versão em Python da Estratégia de Hedge Intertemporal de Bollinger de Futuros de Mercadorias (apenas para fins de estudo)

Autora:Bem-estar, Criado: 2020-06-20 10:52:34, Atualizado: 2025-01-14 20:40:43

A estratégia de arbitragem intertemporal previamente escrita requer entrada manual do spread de hedge para abertura e fechamento de posições. Julgar a diferença de preço é mais subjetivo. Neste artigo, mudaremos a estratégia de hedge anterior para a estratégia de usar o indicador BOLL para abrir e fechar posições.

class Hedge:

'Hedging control class'

def __init__(self, q, e, initAccount, symbolA, symbolB, maPeriod, atrRatio, opAmount):

self.q = q

self.initAccount = initAccount

self.status = 0

self.symbolA = symbolA

self.symbolB = symbolB

self.e = e

self.isBusy = False

self.maPeriod = maPeriod

self.atrRatio = atrRatio

self.opAmount = opAmount

self.records = []

self.preBarTime = 0

def poll(self):

if (self.isBusy or not exchange.IO("status")) or not ext.IsTrading(self.symbolA):

Sleep(1000)

return

insDetailA = exchange.SetContractType(self.symbolA)

if not insDetailA:

return

recordsA = exchange.GetRecords()

if not recordsA:

return

insDetailB = exchange.SetContractType(self.symbolB)

if not insDetailB:

return

recordsB = exchange.GetRecords()

if not recordsB:

return

# Calculate the spread price K line

if recordsA[-1]["Time"] != recordsB[-1]["Time"]:

return

minL = min(len(recordsA), len(recordsB))

rA = recordsA.copy()

rB = recordsB.copy()

rA.reverse()

rB.reverse()

count = 0

arrDiff = []

for i in range(minL):

arrDiff.append(rB[i]["Close"] - rA[i]["Close"])

arrDiff.reverse()

if len(arrDiff) < self.maPeriod:

return

# Calculate Bollinger Bands indicator

boll = TA.BOLL(arrDiff, self.maPeriod, self.atrRatio)

ext.PlotLine("upper trail", boll[0][-2], recordsA[-2]["Time"])

ext.PlotLine("middle trail", boll[1][-2], recordsA[-2]["Time"])

ext.PlotLine("lower trail", boll[2][-2], recordsA[-2]["Time"])

ext.PlotLine("Closing price spread", arrDiff[-2], recordsA[-2]["Time"])

LogStatus(_D(), "upper trail:", boll[0][-1], "\n", "middle trail:", boll[1][-1], "\n", "lower trail:", boll[2][-1], "\n", "Current closing price spread:", arrDiff[-1])

action = 0

# Signal trigger

if self.status == 0:

if arrDiff[-1] > boll[0][-1]:

Log("Open position A buy B sell", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 2

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A buy B sell", "Positive")

elif arrDiff[-1] < boll[2][-1]:

Log("Open position A sell B buy", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 1

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A sell B buy", "Negative")

elif self.status == 1 and arrDiff[-1] > boll[1][-1]:

Log("Close position A buy B sell", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 2

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A buy B sell", "Close Negative")

elif self.status == 2 and arrDiff[-1] < boll[1][-1]:

Log("Close position A sell B buy", ", A latest price:", recordsA[-1]["Close"], ", B latest price:", recordsB[-1]["Close"], "#FF0000")

action = 1

# Add chart markers

ext.PlotFlag(recordsA[-1]["Time"], "A sell B buy", "Close Positive")

# Execute specific instructions

if action == 0:

return

self.isBusy = True

tasks = []

if action == 1:

tasks.append([self.symbolA, "sell" if self.status == 0 else "closebuy"])

tasks.append([self.symbolB, "buy" if self.status == 0 else "closesell"])

elif action == 2:

tasks.append([self.symbolA, "buy" if self.status == 0 else "closesell"])

tasks.append([self.symbolB, "sell" if self.status == 0 else "closebuy"])

def callBack(task, ret):

def callBack(task, ret):

self.isBusy = False

if task["action"] == "sell":

self.status = 2

elif task["action"] == "buy":

self.status = 1

else:

self.status = 0

account = _C(exchange.GetAccount)

LogProfit(account["Balance"] - self.initAccount["Balance"], account)

self.q.pushTask(self.e, tasks[1][0], tasks[1][1], self.opAmount, callBack)

self.q.pushTask(self.e, tasks[0][0], tasks[0][1], self.opAmount, callBack)

def main():

SetErrorFilter("ready|login|timeout")

Log("Connecting to the trading server...")

while not exchange.IO("status"):

Sleep(1000)

Log("Successfully connected to the trading server")

initAccount = _C(exchange.GetAccount)

Log(initAccount)

def callBack(task, ret):

Log(task["desc"], "success" if ret else "failure")

q = ext.NewTaskQueue(callBack)

p = ext.NewPositionManager()

if CoverAll:

Log("Start closing all remaining positions...")

p.CoverAll()

Log("Operation complete")

t = Hedge(q, exchange, initAccount, SA, SB, MAPeriod, ATRRatio, OpAmount)

while True:

q.poll()

t.poll()

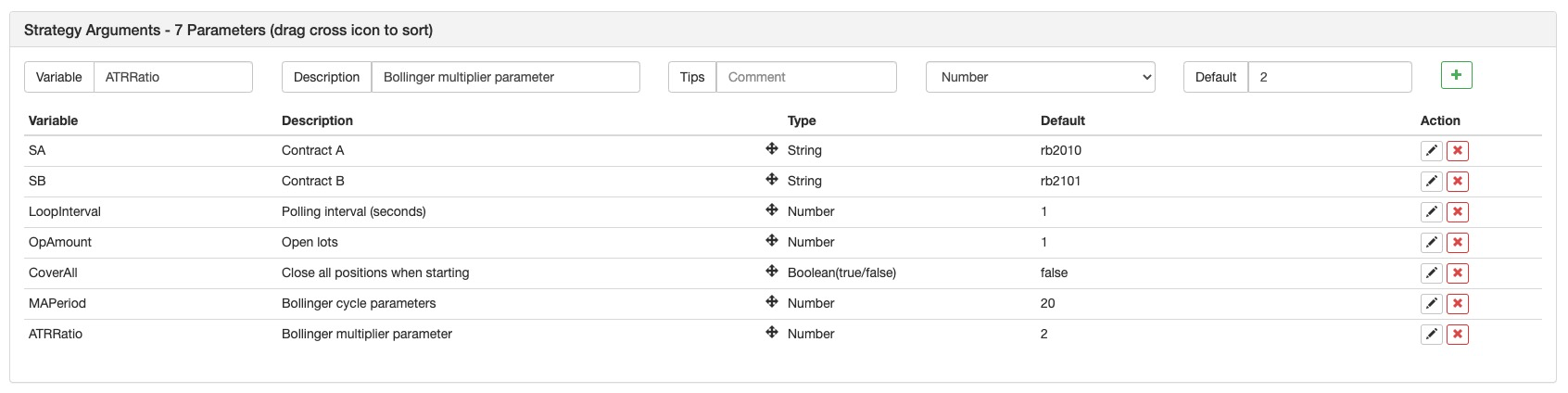

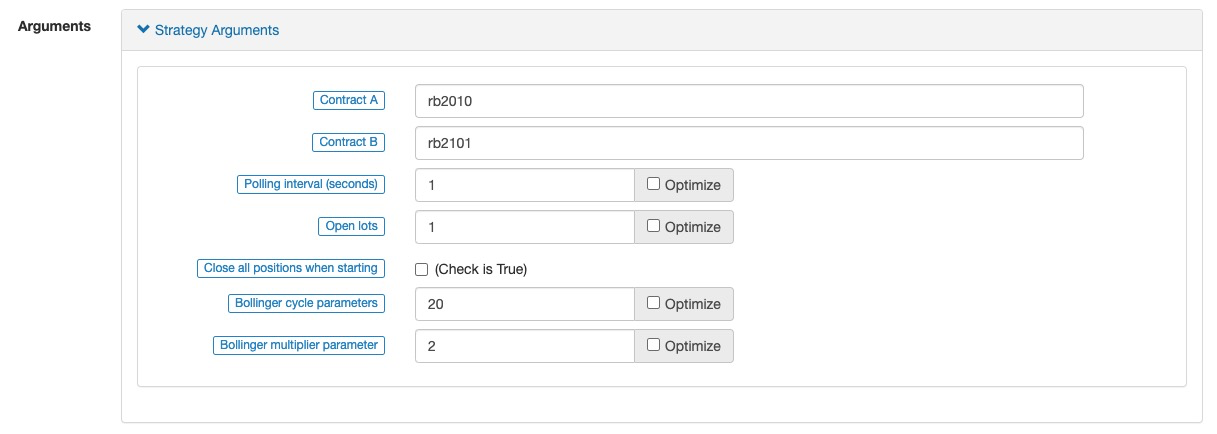

Configuração dos parâmetros da estratégia:

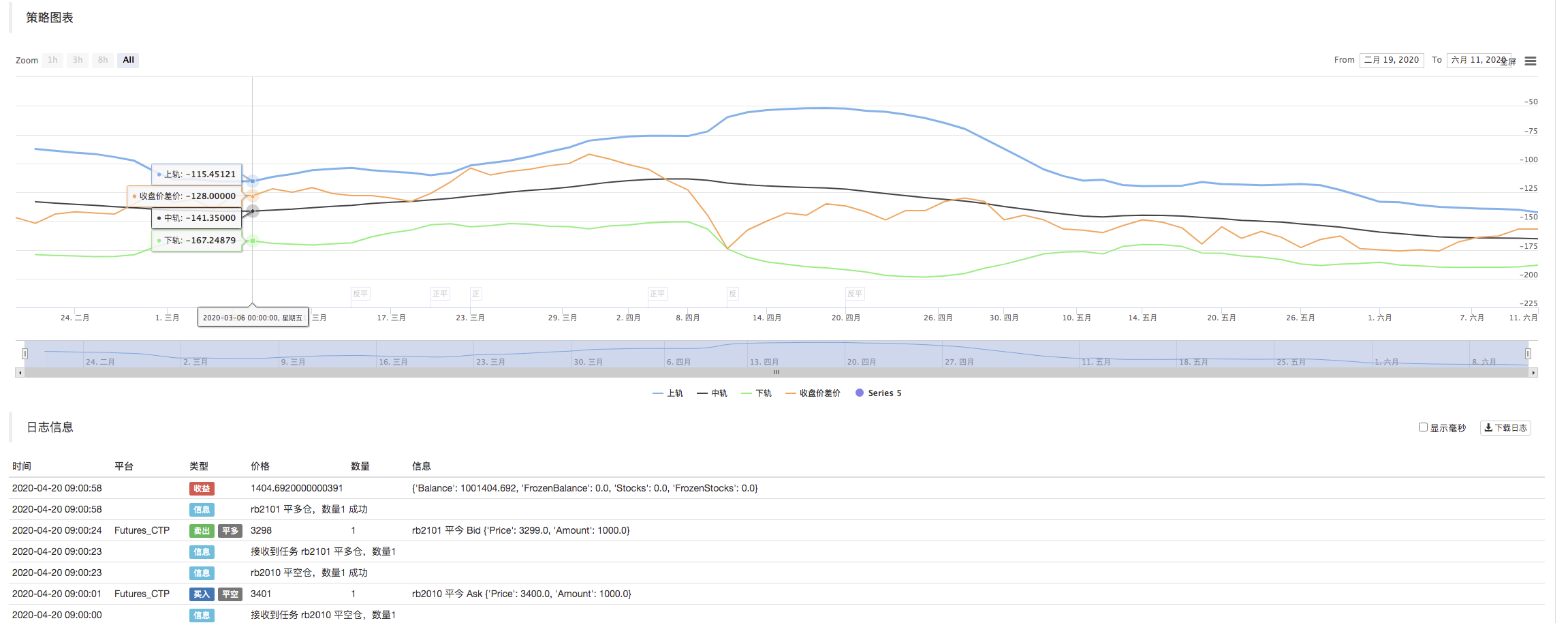

O quadro geral da estratégia é basicamente o mesmo que o quadro daVersão Python da estratégia de cobertura intertemporal de futuros de mercadoriasQuando a estratégia está em execução, os dados da linha K dos dois contratos são obtidos e, em seguida, a diferença de preço é calculada para calcular o spread.TA.BOLLQuando o spread exceder o trilho superior da Bollinger Band, ele será coberto e quando tocar o trilho inferior, ele será oposto ao funcionamento.

Teste de retrocesso:

Este artigo é usado principalmente apenas para fins de estudo. Estratégia completa:https://www.fmz.com/strategy/213826

- Prática quantitativa das bolsas DEX (2) -- Guia do utilizador do hiperlíquido

- Práticas de quantificação da DEX Exchange ((2) -- Guia de uso do Hyperliquid

- Prática quantitativa das bolsas DEX (1) -- dYdX v4 Guia do utilizador

- Introdução à arbitragem de lead-lag em criptomoedas (3)

- Práticas de quantificação da DEX exchange ((1) -- dYdX v4 Guia de uso

- Introdução ao conjunto de Lead-Lag na moeda digital (3)

- Introdução à arbitragem de lead-lag em criptomoedas (2)

- Introdução ao suporte de Lead-Lag na moeda digital (2)

- Discussão sobre a recepção de sinais externos da plataforma FMZ: uma solução completa para receber sinais com serviço HTTP em estratégia

- Discussão da recepção de sinais externos da plataforma FMZ: estratégias para o sistema completo de recepção de sinais do serviço HTTP embutido

- Introdução à arbitragem de lead-lag em criptomoedas (1)

- A negociação na FMEX permite a otimização do volume de encomendas

- Análise e Realização de Futuros de Mercadorias Gráfico da Impressão de Volume

- Desbloqueio de ordenação FMEX Optimização de volume mínimo máximo

- O bot pode enviar mensagens através de uma interface de concha

- FMEX transação de desbloqueio para o máximo de volume

- Estratégia EMV de volatilidade simples

- A mão a mão ensina-te a envelopar um documento de políticas Python de forma barata.

- Taxa de desvio estratégia de negociação BIAS

- Avaliação da curva de capital de backtest utilizando a ferramenta "pyfolio"

- FMZ Quantified Grain (My) Language - Gráfico de interface

- Interface com o robô FMZ utilizando o indicador "Tradingview"

- FMZ Quantificação da Língua Maia (My) - Parâmetros da biblioteca de transações da Língua Maia

- Gráfico de arbitragem de commodities "futures and spots" Baseado em dados fundamentais da FMZ

- Sistema de backtest de alta frequência baseado em cada transação e os defeitos do backtest de linha K

- Versão Python da estratégia de cobertura intertemporal de futuros de mercadorias

- Alguns pensamentos sobre a lógica da negociação de futuros de criptomoedas

- Ferramenta de análise avançada baseada no desenvolvimento da gramática Alpha101

- Ensinar-lhe a atualizar o coletor de mercado backtest a fonte de dados personalizados

- Deficiência do sistema de retorno de alta frequência baseado em transações por papel e retorno de linha K

- Explicação do mecanismo de backtest do nível de simulação FMZ