Estratégia de diminuição da tendência do índice percentual BB

Autora:ChaoZhang, Data: 2023-12-06 14:43:39Tags:

Resumo

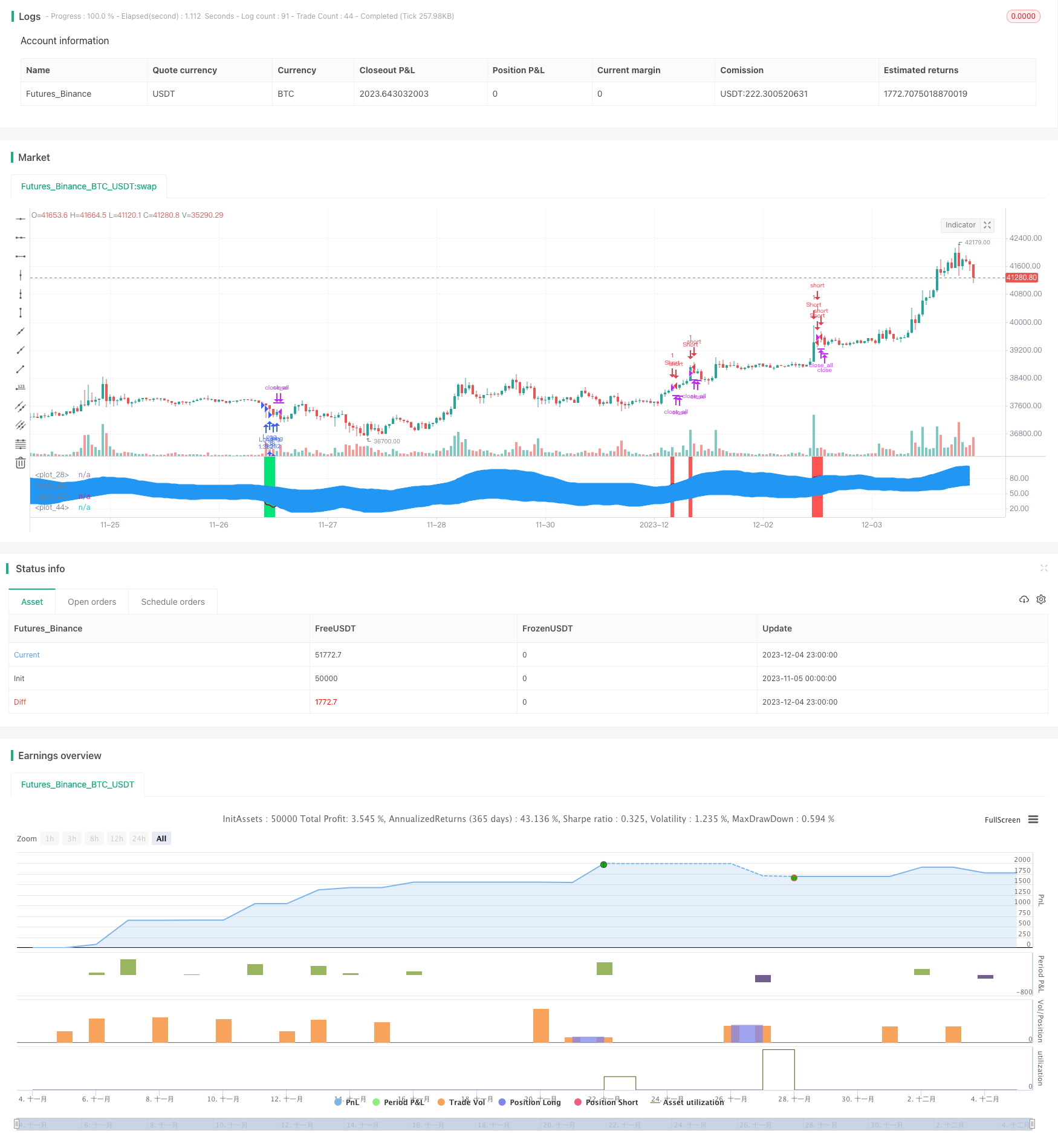

Esta estratégia baseia-se no índice percentual BB combinado com indicadores RSI e MFI. Ele toma decisões longas e curtas detectando quebras de preço do trilho superior e inferior das Bandas de Bollinger, juntamente com sinais de sobrevenda/supercompra do RSI e sinais de sobrevenda/supercompra do MFI. É uma típica estratégia de negociação de tendência que desaparece.

Estratégia lógica

- Calcular Bollinger Band Percentage (BB%). BB% representa o desvio padrão do preço em relação à banda média de Bollinger, que julga a direção do mercado através do canal de Bollinger.

- Incorporar indicadores RSI e MFI para determinar as condições de sobrecompra e sobrevenda. RSI compara o ganho médio e a perda média ao longo de um período de tempo para determinar os níveis de sobrecompra e sobrevenda.

- Quando o preço atravessa o trilho inferior de Bollinger para cima, vá longo; quando o preço atravessa o trilho superior de Bollinger para baixo, vá curto.

Vantagens

- A negociação de tendências decrescentes evita as tendências do mercado e reduz as flutuações dos rendimentos.

- A combinação de múltiplos indicadores filtra os sinais e melhora a precisão das decisões.

- As definições parametrizadas são flexíveis para ajustar as características de risco-retorno da estratégia.

- Aplicável a instrumentos altamente voláteis como commodities, forex, criptomoedas, etc.

Riscos e soluções

- Há uma alta probabilidade de falsos sinais de rupturas de Bollinger, exigindo uma combinação de múltiplos indicadores para filtragem.

- O julgamento do sinal de ruptura requer critérios adequadamente relaxados para evitar perder boas oportunidades.

- Ajustar as definições dos parâmetros para controlar os riscos, tais como o dimensionamento das posições, a elevação das linhas de stop loss, etc.

Orientações de otimização

- Incorporar mecanismos de stop loss baseados na volatilidade, como o indicador ATR.

- Introduzir modelos de aprendizagem de máquina para ajudar a avaliar a qualidade do sinal de ruptura.

- Otimizar os mecanismos de seleção de instrumentos para ajustar dinamicamente os instrumentos participantes.

- Incorporar mais fatores como indicadores de sentimento, notícias, etc. para melhorar o quadro de decisão.

Conclusão

Esta estratégia é aplicada principalmente a instrumentos não-trending de alta volatilidade. Implementa a negociação de tendência desbotada através de combinações de canal e indicadores de Bollinger. As características de risco-retorno podem ser controladas ajustando parâmetros. Melhorias adicionais podem ser feitas introduzindo mais indicadores e modelos auxiliares para otimizar a qualidade da decisão, alcançando assim um melhor desempenho da estratégia.

/*backtest

start: 2023-11-05 00:00:00

end: 2023-12-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Noro

//2018

//@version=2

strategy(title = "BB%/MFI/RSI", shorttitle = "BB%/MFI/RSI", default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 100)

//Settings

needlong = input(true, defval = true, title = "Long")

needshort = input(false, defval = false, title = "Short")

capital = input(100, defval = 100, minval = 1, maxval = 10000, title = "Lot, %")

fromyear = input(1900, defval = 1900, minval = 1900, maxval = 2100, title = "From Year")

toyear = input(2100, defval = 2100, minval = 1900, maxval = 2100, title = "To Year")

frommonth = input(01, defval = 01, minval = 01, maxval = 12, title = "From Month")

tomonth = input(12, defval = 12, minval = 01, maxval = 12, title = "To Month")

fromday = input(01, defval = 01, minval = 01, maxval = 31, title = "From Day")

today = input(31, defval = 31, minval = 01, maxval = 31, title = "To Day")

source = hlc3

length = input(14, minval=1), mult = input(2.0, minval=0.001, maxval=50), bblength = input(50, minval=1, title="BB Period")

DrawRSI_f=input(true, title="Draw RSI?", type=bool)

DrawMFI_f=input(false, title="Draw MFI?", type=bool)

HighlightBreaches=input(true, title="Highlight Oversold/Overbought?", type=bool)

DrawMFI = (not DrawMFI_f) and (not DrawRSI_f) ? true : DrawMFI_f

DrawRSI = (DrawMFI_f and DrawRSI_f) ? false : DrawRSI_f

// RSI

rsi_s = DrawRSI ? rsi(source, length) : na

plot(DrawRSI ? rsi_s : na, color=maroon, linewidth=2)

// MFI

upper_s = DrawMFI ? sum(volume * (change(source) <= 0 ? 0 : source), length) : na

lower_s = DrawMFI ? sum(volume * (change(source) >= 0 ? 0 : source), length) : na

mf = DrawMFI ? rsi(upper_s, lower_s) : na

plot(DrawMFI ? mf : na, color=green, linewidth=2)

// Draw BB on indices

bb_s = DrawRSI ? rsi_s : DrawMFI ? mf : na

basis = sma(bb_s, length)

dev = mult * stdev(bb_s, bblength)

upper = basis + dev

lower = basis - dev

plot(basis, color=red)

p1 = plot(upper, color=blue)

p2 = plot(lower, color=blue)

fill(p1,p2, blue)

b_color = (bb_s > upper) ? red : (bb_s < lower) ? lime : na

bgcolor(HighlightBreaches ? b_color : na, transp = 0)

//Signals

up = bb_s < lower and close < open

dn = bb_s > upper and close > open

size = strategy.position_size

lp = size > 0 and close > open

sp = size < 0 and close < open

exit = (up == false and dn == false) and (lp or sp)

//Trading

lot = strategy.position_size == 0 ? strategy.equity / close * capital / 100 : lot[1]

if up

if strategy.position_size < 0

strategy.close_all()

strategy.entry("Long", strategy.long, needlong == false ? 0 : lot, when=(time > timestamp(fromyear, frommonth, fromday, 00, 00) and time < timestamp(toyear, tomonth, today, 23, 59)))

if dn

if strategy.position_size > 0

strategy.close_all()

strategy.entry("Short", strategy.short, needshort == false ? 0 : lot, when=(time > timestamp(fromyear, frommonth, fromday, 00, 00) and time < timestamp(toyear, tomonth, today, 23, 59)))

if time > timestamp(toyear, tomonth, today, 23, 59) or exit

strategy.close_all()

- Reversão das bandas de Bollinger com filtro de tendência MA

- Estratégia de negociação quantitativa baseada no RSI

- Estratégia de negociação cruzada de média móvel múltipla

- Estratégia de cruzamento da média móvel

- Estratégia de saída automática de S/R

- Estratégia de abertura e de encerramento do canal de preços de impulso

- Melhoria da estratégia de cruzamento da média móvel com orientação da tendência do mercado

- Estratégia de negociação de candelabro dinâmico

- SSL Hybrid Exit Arrow Quant Estratégia

- Estratégia de cronometragem ADX de média móvel dupla

- MACD Bollinger Turtle Estratégia de negociação

- Estratégia Triple SuperTrend e Stoch RSI

- Estratégia cruzada de média móvel de lucro de 1%

- Estratégia de negociação cruzada de média móvel quantitativa ponderada

- Estratégia de indicador de RSI auxiliar múltipla

- Estratégia de tendência cruzada de média móvel dupla

- Estratégia de reversão das bandas de Bollinger

- Uma estratégia de tendência adaptativa ATR-ADX V2

- Estratégia de negociação de ciclo de dois fatores

- Estratégia de swingers média máxima máxima e mínima