Tudo Sobre a Estratégia de Negociação de Momentum com Stop Loss para Ouro

Autora:ChaoZhang, Data: 2024-02-20 16:27:18Tags:

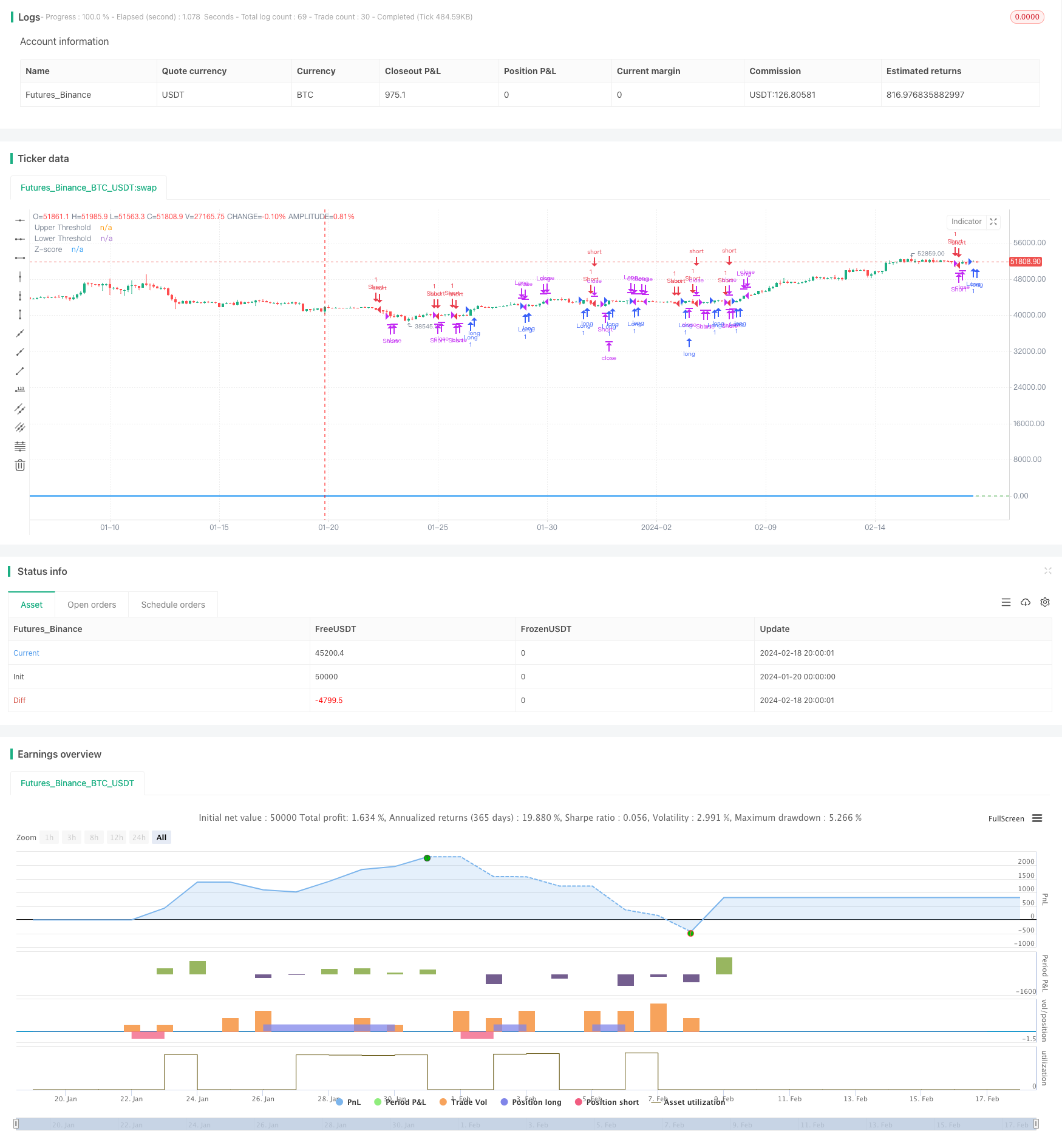

Resumo

Esta estratégia calcula o desvio do preço do ouro da sua média móvel exponencial de 21 dias para determinar situações de sobrecompra e sobrevenda no mercado.

Estratégia lógica

- Calcular a EMA de 21 dias como linha de base

- Cálculo do desvio do preço da EMA

- Padronizar o desvio em Z-Score

- Vá longo quando a pontuação Z ultrapassa 0,5; vá curto quando a pontuação Z ultrapassa -0,5

- Posições fechadas quando o Z-Score cair para 0,5/-0,5

- Configure stop loss quando a pontuação Z for superior a 3 ou inferior a -3

Análise das vantagens

As vantagens desta estratégia são as seguintes:

- EMA como suporte/resistência dinâmico para captar tendências

- Stddev e Z-Score avaliam eficazmente os níveis de sobrecompra/supervenda, reduzindo os falsos sinais

- A EMA exponencial dá mais peso aos preços recentes, tornando-a mais sensível

- Z-Score padroniza desvio para regras de julgamento unificadas

- O mecanismo de stop loss controla o risco e limita as perdas

Análise de riscos

Alguns riscos a considerar:

- A EMA pode gerar sinais errados quando as diferenças de preços ou quebras

- Os limiares Stddev/Z-Score precisam de ajuste adequado para melhor desempenho

- A definição incorreta de stop loss pode conduzir a perdas desnecessárias

- Eventos de cisne negro podem desencadear stop loss e perder oportunidade de tendência

Soluções: 1. Optimizar o parâmetro EMA para identificar as principais tendências 2. Backtest para encontrar limiares ideais de Stddev/Z-Score Testar a racionalidade da perda de stop com trailing stops 4. Reavaliação do mercado após o evento, ajustar a estratégia em conformidade

Orientações de otimização

Algumas formas de melhorar a estratégia:

- Usar indicadores de volatilidade como ATR em vez de simples Stddev para medir o apetite pelo risco

- Teste diferentes tipos de médias móveis para melhor referência

- Otimizar o parâmetro EMA para encontrar o melhor período

- Otimizar os limiares da pontuação Z para melhorar o desempenho

- Adicionar paradas baseadas na volatilidade para um controlo de risco mais inteligente

Conclusão

Em geral, esta é uma estratégia sólida de tendência. Ele usa a EMA para definir a direção da tendência e o desvio padronizado para identificar claramente os níveis de sobrecompra / sobrevenda para sinais comerciais. Controles razoáveis de stop loss controlam o risco enquanto deixam os lucros correrem.

/*backtest

start: 2024-01-20 00:00:00

end: 2024-02-19 00:00:00

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("GC Momentum Strategy with Stoploss and Limits", overlay=true)

// Input for the length of the EMA

ema_length = input.int(21, title="EMA Length", minval=1)

// Exponential function parameters

steepness = 2

// Calculate the EMA

ema = ta.ema(close, ema_length)

// Calculate the deviation of the close price from the EMA

deviation = close - ema

// Calculate the standard deviation of the deviation

std_dev = ta.stdev(deviation, ema_length)

// Calculate the Z-score

z_score = deviation / std_dev

// Long entry condition if Z-score crosses +0.5 and is below 3 standard deviations

long_condition = ta.crossover(z_score, 0.5)

// Short entry condition if Z-score crosses -0.5 and is above -3 standard deviations

short_condition = ta.crossunder(z_score, -0.5)

// Exit long position if Z-score converges below 0.5 from top

exit_long_condition = ta.crossunder(z_score, 0.5)

// Exit short position if Z-score converges above -0.5 from below

exit_short_condition = ta.crossover(z_score, -0.5)

// Stop loss condition if Z-score crosses above 3 or below -3

stop_loss_long = ta.crossover(z_score, 3)

stop_loss_short = ta.crossunder(z_score, -3)

// Enter and exit positions based on conditions

if (long_condition)

strategy.entry("Long", strategy.long)

if (short_condition)

strategy.entry("Short", strategy.short)

if (exit_long_condition)

strategy.close("Long")

if (exit_short_condition)

strategy.close("Short")

if (stop_loss_long)

strategy.close("Long")

if (stop_loss_short)

strategy.close("Short")

// Plot the Z-score on the chart

plot(z_score, title="Z-score", color=color.blue, linewidth=2)

// Optional: Plot zero lines for reference

hline(0.5, "Upper Threshold", color=color.red)

hline(-0.5, "Lower Threshold", color=color.green)

- Estratégia de armadilha de avanço da EMA

- Estratégia de negociação Golden Cross Dead Cross

- Estratégia de acompanhamento de tendências em quadros de tempo múltiplos baseada em supertendências

- Estratégia manual de alertas de compra e venda

- Estratégia de referência de tendência ascendente de avanço quantitativo

- Estratégia de negociação adaptativa baseada numa plataforma de negociação quantitativa

- Estratégia de negociação quantitativa baseada na nuvem de Ichimoku e na média móvel

- Estratégia de acompanhamento da inversão da média móvel dupla

- Estratégia de inversão das bandas de Bollinger

- Ichimoku Kinko Hyo Cloud + QQE Estratégia Quantitativa

- Parabola Oscilador Procurando altos e baixos Estratégia

- Estratégia de ruptura das bandas de Bollinger

- Estratégia de avanço da diferença de valor justo

- Sistema de cruzamento de média móvel adaptativa com ruptura de impulso

- Estratégia de negociação baseada em padrões de pico a pico

- Estratégia de compra de EMA múltipla

- Tendência de cruzamento da OBV EMA na sequência da estratégia

- Estratégia de acompanhamento da tendência cruzada do RSI e do MA

- Estratégia de reversão do impulso com dupla confirmação

- Crossover da EMA para a Estratégia Quant Long Line