Стратегия разворота скользящей средней

Эта стратегия называется Mean Reversion Reverse Strategy Based on Moving Average, и основной идеей является покупка после падения ключевой средней линии и остановка после достижения заданного целевого прибыли.

Основной принцип этой стратегии заключается в том, чтобы использовать переход к краткосрочной средней линии, чтобы поймать возможность отскока в консолидированном состоянии. В частности, когда цена после падения более длительного периода средней линии (например, 20-дневная линия, 50-дневная линия и т. д.) проявляет сильные признаки перепада, из-за особенностей средней реверсии рыночных колебаний цена часто производит определенный уровень отскока.

Конкретная логика покупки этой стратегии заключается в следующем: купить одну руку после падения цены на 20-ю дневную линию, наложить одну руку после падения на 50-ю дневную линию, продолжать наложить одну руку после падения на 100-ю дневную линию, наложить одну руку до максимума после падения на 200-ю дневную линию, сделать еще 4 руки. После достижения заранее установленного стоп-таргета.

Анализ преимуществ

- Использование обратных характеристик средней линии для эффективного выявления краткосрочных шансов на отскок

- Построение складов в партиях снижает риски появления единичных пунктов.

- Настройка условий остановки, чтобы закрепить прибыль

- Фильтрация с использованием стартовых цен и предыдущих минимумов, чтобы избежать ложных прорывов

Анализ рисков

- При длительном удержании риски возврата могут быть. Убытки могут расшириться, если рынок продолжит падать.

- Сигналы средней линии могут быть ошибочными, что приводит к убыткам

- Возможно, не достигнут установленный параметр, не удастся полностью или частично остановить торможение

Направление оптимизации

- Возможность тестирования доходности и устойчивости при различных параметрах

- Покупка может быть рассмотрена в сочетании с другими показателями, такими как MACD, KD и т. Д.

- Среднелинейный цикл, подходящий для стиля торговли, может быть выбран в зависимости от характеристик разных сортов

- Можно вводить алгоритмы машинного обучения для динамической оптимизации параметров

Подвести итог

Эта стратегия в целом является более классической и общепринятой стратегией сплошной торговли. Она правильно использует свойства сплошной торговли, а также объединяет несколько сплошных линий для идентификации краткосрочных покупок.

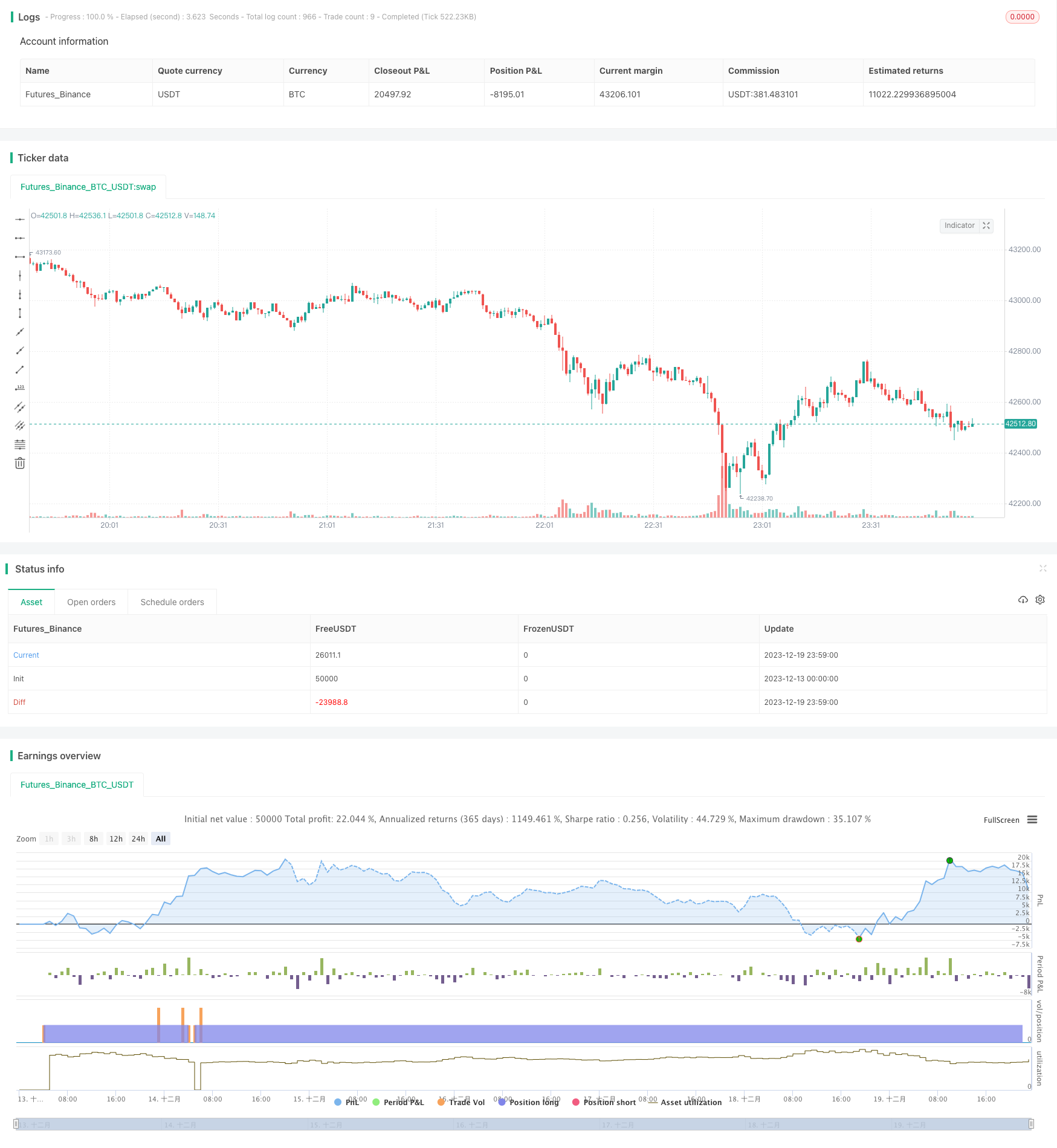

/*backtest

start: 2023-12-13 00:00:00

end: 2023-12-20 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("EMA_zorba1", shorttitle="zorba_ema", overlay=true)

// Input parameters

qt1 = input.int(5, title="Quantity 1", minval=1)

qt2 = input.int(10, title="Quantity 2", minval=1)

qt3 = input.int(15, title="Quantity 3", minval=1)

qt4 = input.int(20, title="Quantity 4", minval=1)

ema10 = ta.ema(close, 10)

ema20 = ta.ema(close, 20)

ema50 = ta.ema(close, 50)

ema100 = ta.ema(close, 100)

ema200 = ta.ema(close, 200)

// Date range filter

start_date = timestamp(year=2021, month=1, day=1)

end_date = timestamp(year=2024, month=10, day=27)

in_date_range = true

// Profit condition

profit_percentage = input(1, title="Profit Percentage") // Adjust this value as needed

// Pyramiding setting

pyramiding = input.int(2, title="Pyramiding", minval=1, maxval=10)

// Buy conditions

buy_condition_1 = in_date_range and close < ema20 and close > ema50 and close < open and close < low[1]

buy_condition_2 = in_date_range and close < ema50 and close > ema100 and close < open and close < low[1]

buy_condition_3 = in_date_range and close < ema100 and close > ema200 and close < open and close < low[1]

buy_condition_4 = in_date_range and close < ema200 and close < open and close < low[1]

// Exit conditions

profit_condition = strategy.position_avg_price * (1 + profit_percentage / 100) <= close

exit_condition_1 = in_date_range and (close > ema10 and ema10 > ema20 and ema10 > ema50 and ema10 > ema100 and ema10 > ema200 and close < open) and profit_condition and close < low[1] and close < low[2]

exit_condition_2 = in_date_range and (close < ema10 and close[1] > ema10 and close < close[1] and ema10 > ema20 and ema10 > ema50 and ema10 > ema100 and ema10 > ema200 and close < open) and profit_condition and close < low[1] and close < low[2]

// Exit condition for when today's close is less than the previous day's low

//exit_condition_3 = close < low[1]

// Strategy logic

strategy.entry("Buy1", strategy.long, qty=qt1 * pyramiding, when=buy_condition_1)

strategy.entry("Buy2", strategy.long, qty=qt2 * pyramiding, when=buy_condition_2)

strategy.entry("Buy3", strategy.long, qty=qt3 * pyramiding, when=buy_condition_3)

strategy.entry("Buy4", strategy.long, qty=qt4 * pyramiding, when=buy_condition_4)

strategy.close("Buy1", when=exit_condition_1 or exit_condition_2)

strategy.close("Buy2", when=exit_condition_1 or exit_condition_2)

strategy.close("Buy3", when=exit_condition_1 or exit_condition_2)

strategy.close("Buy4", when=exit_condition_1 or exit_condition_2)