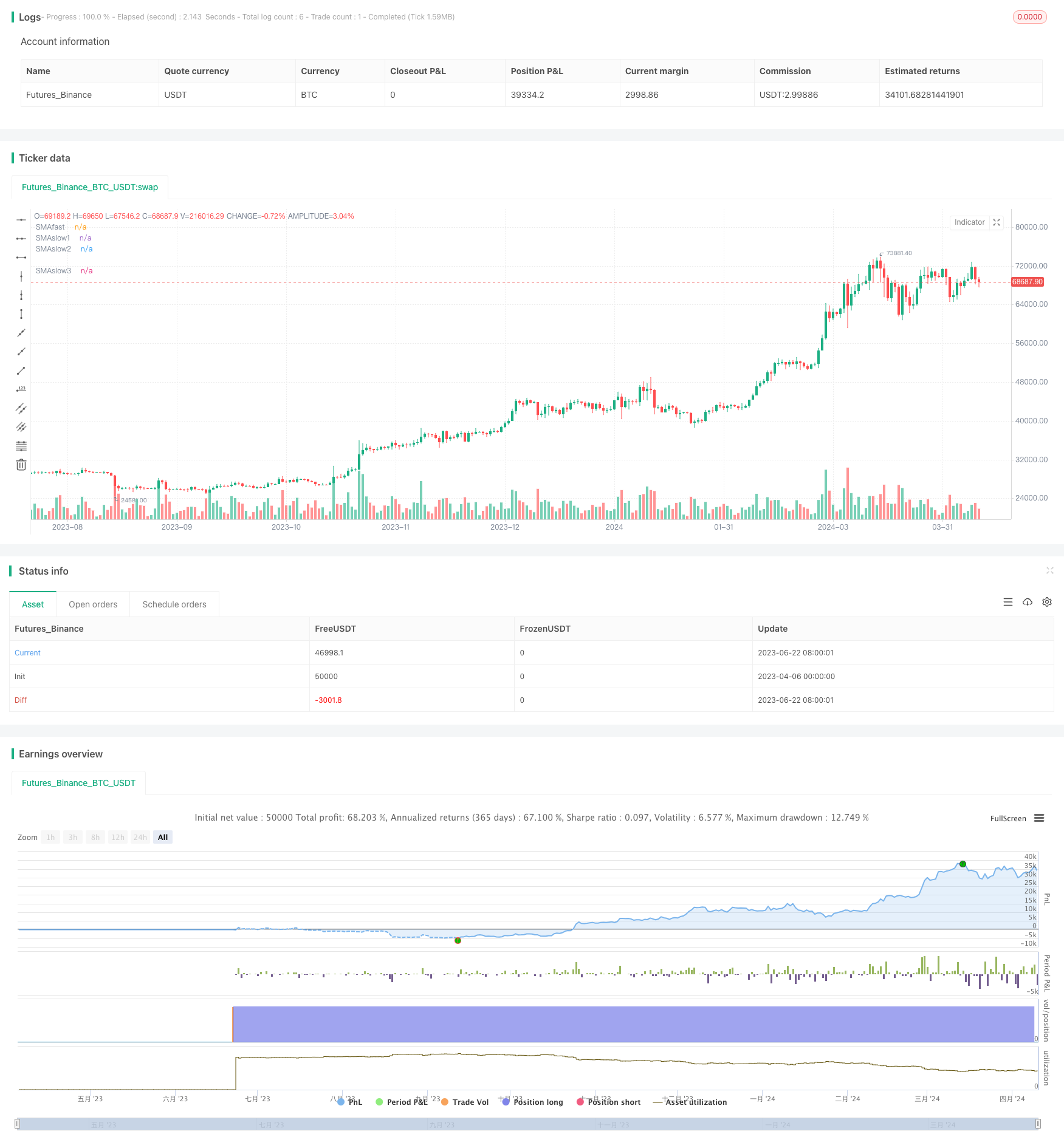

Tổng quan

Chiến lược này sử dụng đường trung bình và MACD là tín hiệu giao dịch chính. Chiến lược sử dụng đường trung bình nhanh và đường trung bình chậm để báo hiệu mở vị trí, kết hợp với âm tính của biểu đồ hình trụ MACD để đánh giá xu hướng. Chiến lược đặt nhiều mức dừng và dừng cùng lúc khi mở vị trí và liên tục sửa đổi vị trí dừng để khóa lợi nhuận khi thời gian giữ vị trí tăng lên.

Nguyên tắc chiến lược

- Đường trung bình tốc độ nhanh và đường trung bình tốc độ chậm 1 chéo lên, đồng thời giá đóng cửa trên đường trung bình tốc độ chậm 2, đồ thị MACD lớn hơn 0;

- Đường trung bình tốc độ nhanh và đường trung bình tốc độ chậm 1 chéo xuống, đồng thời giá đóng cửa bên dưới đường trung bình tốc độ chậm 2, biểu đồ MACD cột nhỏ hơn 0, làm trống;

- Bắt đầu vị trí bằng cách đặt nhiều mức dừng và dừng cùng một lúc, dừng vị trí được thiết lập theo sở thích rủi ro, và dừng lỗ được điều chỉnh liên tục theo thời gian giữ vị trí, và dần dần khóa lợi nhuận;

- Chu kỳ đường trung bình, tham số MACD, mức dừng lỗ và nhiều thứ khác có thể được điều chỉnh linh hoạt để phù hợp với môi trường thị trường khác nhau.

Chiến lược này sử dụng xu hướng bắt chéo đồng tuyến, đồng thời xác nhận hướng bằng chỉ số MACD, tăng độ tin cậy của phán đoán xu hướng. Cài đặt dừng chân đa cấp có thể kiểm soát tốt hơn rủi ro và lợi nhuận.

Lợi thế chiến lược

- Giao nhau là một phương pháp theo dõi xu hướng cổ điển, có thể bắt kịp sự hình thành của xu hướng.

- Việc sử dụng đường trung bình đa cấp cho phép đánh giá toàn diện hơn về cường độ và tính bền vững của xu hướng;

- Chỉ số MACD có thể xác định xu hướng và phán đoán động lực một cách hiệu quả, như là một bổ sung mạnh mẽ cho đường trung bình;

- Các thiết lập dừng nhiều cấp và dừng động cho phép kiểm soát rủi ro, đồng thời tăng lợi nhuận và tăng cường sự ổn định của hệ thống;

- Các tham số có thể điều chỉnh, có khả năng thích ứng, có thể được thiết lập linh hoạt theo các giống và chu kỳ khác nhau.

Rủi ro chiến lược

- Có nguy cơ tín hiệu bị tụt hậu ở đường giao thoa, có thể bỏ lỡ xu hướng ban đầu hoặc bắt kịp.

- Thiết lập không đúng các tham số có thể dẫn đến quá nhiều giao dịch hoặc quá nhiều thời gian giữ vị trí, tăng chi phí và rủi ro;

- Cài đặt dừng lỗ quá mạnh có thể dẫn đến dừng lỗ sớm, và thiết lập dừng lỗ quá bảo thủ có thể ảnh hưởng đến lợi nhuận;

- Sự thay đổi trong xu hướng hoặc sự thay đổi của thị trường có thể dẫn đến thất bại của chiến lược.

Những rủi ro này có thể được kiểm soát bằng cách tối ưu hóa các tham số, điều chỉnh vị trí và đặt các điều kiện bổ sung. Tuy nhiên, không có chiến lược nào có thể tránh hoàn toàn rủi ro và cần được nhà đầu tư thận trọng.

Hướng tối ưu hóa chiến lược

- Có thể xem xét thêm các chỉ số như RSI, BRI để xác nhận xu hướng và tín hiệu;

- Có thể tối ưu hóa các thiết lập về điểm dừng lỗ tinh tế hơn, chẳng hạn như xem xét ATR hoặc Stop Loss %;

- Có thể điều chỉnh các tham số theo biến động của thị trường để cải thiện khả năng thích ứng;

- Có thể giới thiệu mô-đun quản lý vị trí, điều chỉnh kích thước vị trí tùy theo tình trạng rủi ro;

- Các chiến lược có thể được tập hợp, tạo ra các chiến lược để phân tán rủi ro.

Thông qua việc tối ưu hóa và cải tiến liên tục, bạn có thể làm cho chiến lược trở nên vững chắc và đáng tin cậy hơn, thích ứng tốt hơn với môi trường thị trường thay đổi. Tuy nhiên, tối ưu hóa cần thận trọng và tránh quá phù hợp.

Tóm tắt

Chiến lược này được kết hợp với các chỉ số MACD và đường chéo đồng nhất để tạo ra một hệ thống giao dịch tương đối hoàn chỉnh. Thiết kế đường chéo đa cấp và hoạt động đa đầu tăng cường khả năng nắm bắt xu hướng và khả năng kiểm soát rủi ro của hệ thống.

/*backtest

start: 2023-04-06 00:00:00

end: 2024-04-11 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © maxmirus

//@version=5

strategy("My strategy_Cross_SMA(EMA)+Macd,slow3",overlay=true)

// ver 4

// Date Inputs

startDate = input(timestamp('2019-01-01T00:00:00+0300'), '' , inline='time1',

tooltip=' Время первого бара расчета стратегии. Первый ордер может быть выставлен на следующем баре после стартового.')

finishDate = input(timestamp('2044-01-01T00:00:00+0300'), '' , inline='time2',

tooltip=' Время после которого больше не будут размещаться ордера входа в позицию.')

// Calculate start/end date and time condition

time_cond = true

//SMA(EMA) Inputs

fast=input.int(12, title="Fastlength",group="MA")

slow1=input.int(54,title="Slowlength1",group="MA")

slow2=input.int(100, title="Slowlength2",group="MA")

slow3=input.int(365, title="Slowlength3",group="MA")

fastma=input.string(title="Fastlength", defval="EMA",options=["SMA","EMA"],group="MA")

slowma1=input.string(title="Slowlength1", defval="EMA",options=["SMA","EMA"],group="MA")

slowma2=input.string(title="Slowlength2", defval="EMA",options=["SMA","EMA"],group="MA")

slowma3=input.string(title="Slowlength3", defval="EMA",options=["SMA","EMA"],group="MA")

fastlength = fastma == "EMA" ? ta.ema(close, fast) : ta.sma(close, fast)

slowlength1 = slowma1 == "EMA" ? ta.ema(close, slow1) : ta.sma(close, slow1)

slowlength2 = slowma2 == "EMA" ? ta.ema(close, slow2) : ta.sma(close, slow2)

slowlength3 = slowma3 == "EMA" ? ta.ema(close, slow3) : ta.sma(close, slow3)

//Macd Inputs

macdfastline = input.int(12, title="FastMacd",group="MACD")

macdslowline = input.int(26,title="SlowMacd",group="MACD")

macdhistline = input.int(9,title="HistMacd",group="MACD")

src=input(defval=close,title="Source",group="MACD")

sma_source = input.string(title="Oscillator MA Type", defval="EMA", options=["SMA", "EMA"],group="MACD")

sma_signal = input.string(title="Signal Line MA Type", defval="EMA", options=["SMA", "EMA"],group="MACD")

fast_ma = sma_source == "SMA" ? ta.sma(src, macdfastline) : ta.ema(src, macdfastline)

slow_ma = sma_source == "SMA" ? ta.sma(src, macdslowline) : ta.ema(src, macdslowline)

macd = fast_ma - slow_ma

signal = sma_signal == "SMA" ? ta.sma(macd, macdhistline) : ta.ema(macd, macdhistline)

hist = macd - signal

//fastMACD = ta.ema(close, macdline) - ta.ema(close, signalline)

//signalMACD = ta.ema(MACD, histline)

//histMACD = MACD - aMACD

//EMA Plot

plot(fastlength,title="SMAfast",color=color.blue)

plot(slowlength1,title="SMAslow1",color=color.orange)

plot(slowlength2,title="SMAslow2",color=color.red)

plot(slowlength3,title="SMAslow3",color=color.black)

//Macd plot

//col_macd = input(#2962FF, "MACD Line ", group="Color Settings", inline="MACD")

//col_signal = input(#FF6D00, "Signal Line ", group="Color Settings", inline="Signal")

//col_grow_above = input(#26A69A, "Above Grow", group="Histogram", inline="Above")

//col_fall_above = input(#B2DFDB, "Fall", group="Histogram", inline="Above")

//col_grow_below = input(#FFCDD2, "Below Grow", group="Histogram", inline="Below")

//col_fall_below = input(#FF5252, "Fall", group="Histogram", inline="Below")

//plot(hist, title="Histogram", style=plot.style_columns, color=(hist>=0 ? (hist[1] < hist ? col_grow_above : col_fall_above) : (hist[1] < hist ? col_grow_below : col_fall_below)))

//plot(macd, title="MACD", color=col_macd)

//plot(signal, title="Signal", color=col_signal)

//Take profit

tp1=input.float(5.1,title="Take Profit1_%",step=0.1)/100

tp2=input.float(10.1,title="Take Profit2_%",step=0.1)/100

//Stop loss

sl1=input.float(5.1,title="Stop loss1_%",step=0.1)/100

sl2=input.float(0.1,title="Stop loss2_%",step=0.1)/100

sl3=input.float(-5.5,title="Stop loss3_%", step=0.1)/100

//Qty closing position

Qty1 = input.float(0.5, title="QtyClosingPosition1",step=0.01)

Qty2 = input.float(0.25, title="QtyClosingPosition2",step=0.01)

//Take profit Long and Short

LongTake1=strategy.position_avg_price*(1+tp1)

LongTake2=strategy.position_avg_price*(1+tp2)

ShortTake1=strategy.position_avg_price*(1-tp1)

ShortTake2=strategy.position_avg_price*(1-tp2)

//Plot Levels Take

plot(strategy.position_size > 0 ? LongTake1 : na,color=color.green,style=plot.style_linebr)

plot(strategy.position_size > 0 ? LongTake2 : na,color=color.green,style=plot.style_linebr)

plot(strategy.position_size < 0 ? ShortTake1 : na,color=color.green,style=plot.style_linebr)

plot(strategy.position_size < 0 ? ShortTake2 : na,color=color.green,style=plot.style_linebr)

//Stop loss long and short

LongStop1=strategy.position_avg_price*(1-sl1)

LongStop2=strategy.position_avg_price*(1-sl2)

LongStop3=strategy.position_avg_price*(1-sl3)

ShortStop1=strategy.position_avg_price*(1+sl1)

ShortStop2=strategy.position_avg_price*(1+sl2)

ShortStop3=strategy.position_avg_price*(1+sl3)

//Stop=strategy.position_avg_price

//Plot Levels Stop

plot(strategy.position_size > 0 ? LongStop1 : na,color=color.red,style=plot.style_linebr)

plot(strategy.position_size > 0 ? LongStop2 : na,color=color.red,style=plot.style_linebr)

plot(strategy.position_size > 0 ? LongStop3 : na,color=color.red,style=plot.style_linebr)

plot(strategy.position_size < 0 ? ShortStop1 : na,color=color.red,style=plot.style_linebr)

plot(strategy.position_size < 0 ? ShortStop2 : na,color=color.red,style=plot.style_linebr)

plot(strategy.position_size < 0 ? ShortStop3 : na,color=color.red,style=plot.style_linebr)

//Entry condition

LongCondition1 = ta.crossover(fastlength, slowlength1)

LongCondition2 = close>slowlength2

LongCondition3 = time_cond

LongCondition4=close>slowlength3

//LongCondition5=slowlength100>slowlength3

LongCondition6 = hist > 0

buy=(LongCondition1 and LongCondition2 and LongCondition3 and LongCondition4 and LongCondition6 ) and strategy.position_size<=0

//longCondition3 = nz(strategy.position_size) == 0//если отсутствует открытая позиция

ShortCondition1 = ta.crossunder(fastlength, slowlength1)

ShortCondition2 = close<slowlength2

ShortCondition3 = time_cond

ShortCondition4=close<slowlength3

//ShortCondition5=slowlength100<slowlength3

ShortCondition6=hist < 0

sell=(ShortCondition1 and ShortCondition2 and ShortCondition3 and ShortCondition4 and ShortCondition6 ) and strategy.position_size>=0

//Strategy entry

strategy.cancel_all(not strategy.position_size)

if(buy)

strategy.cancel_all()

strategy.entry("Buy",strategy.long)

if(sell)

strategy.cancel_all()

strategy.entry("Sell",strategy.short)

//Strategy Long exit

var int exitCounter=0

exitCounter := not strategy.position_size or strategy.position_size > 0 and strategy.position_size[1] < 0 or strategy.position_size < 0 and strategy.position_size[1] > 0 ? 0:

strategy.position_size > 0 and strategy.position_size[1]>strategy.position_size? exitCounter[1] + 1:

strategy.position_size < 0 and strategy.position_size[1]<strategy.position_size? exitCounter[1] - 1:

exitCounter[1]

if strategy.position_size > 0 and strategy.position_size[1]<=0

strategy.order("Take Long1",strategy.short, qty=math.abs(strategy.position_size*Qty1), limit=LongTake1, oca_name='Long1', oca_type=strategy.oca.cancel)

if strategy.position_size > 0 and strategy.position_size[1]<=0

strategy.order("Take Long2",strategy.short, qty=math.abs(strategy.position_size*Qty2), limit=LongTake2, oca_name='Long2', oca_type=strategy.oca.cancel)

if strategy.position_size > 0 and strategy.position_size[1]<=0

strategy.order("Stop Long1",strategy.short, qty=math.abs(strategy.position_size),stop=LongStop1,oca_name='Long1',oca_type=strategy.oca.cancel)

if ta.change(exitCounter) and exitCounter==1

strategy.order("Stop Long2",strategy.short, qty=math.abs(strategy.position_size),stop=LongStop2,oca_name='Long2',oca_type=strategy.oca.cancel)

if ta.change(exitCounter) and exitCounter==2

strategy.order("Stop Long3",strategy.short, qty=math.abs(strategy.position_size),stop=LongStop3)

// Strategy Short exit

if strategy.position_size < 0 and strategy.position_size[1]>=0

strategy.order("Take Short1", strategy.long, qty=math.abs(strategy.position_size*Qty1), limit=ShortTake1, oca_name='Short1', oca_type=strategy.oca.cancel)

if strategy.position_size < 0 and strategy.position_size[1]>=0

strategy.order("Take Short2", strategy.long, qty=math.abs(strategy.position_size*Qty2), limit=ShortTake2, oca_name='Short2', oca_type=strategy.oca.cancel)

if strategy.position_size < 0 and strategy.position_size[1]>=0

strategy.order("Stop Short1",strategy.long, qty=math.abs(strategy.position_size),stop=ShortStop1,oca_name='Short1',oca_type=strategy.oca.cancel)

if ta.change(exitCounter) and exitCounter==-1

strategy.order("Stop Short2",strategy.long, qty=math.abs(strategy.position_size),stop=ShortStop2,oca_name='Short2',oca_type=strategy.oca.cancel)

if ta.change(exitCounter) and exitCounter==-2

strategy.order("Stop Short3",strategy.long,qty=math.abs(strategy.position_size),stop=ShortStop3)