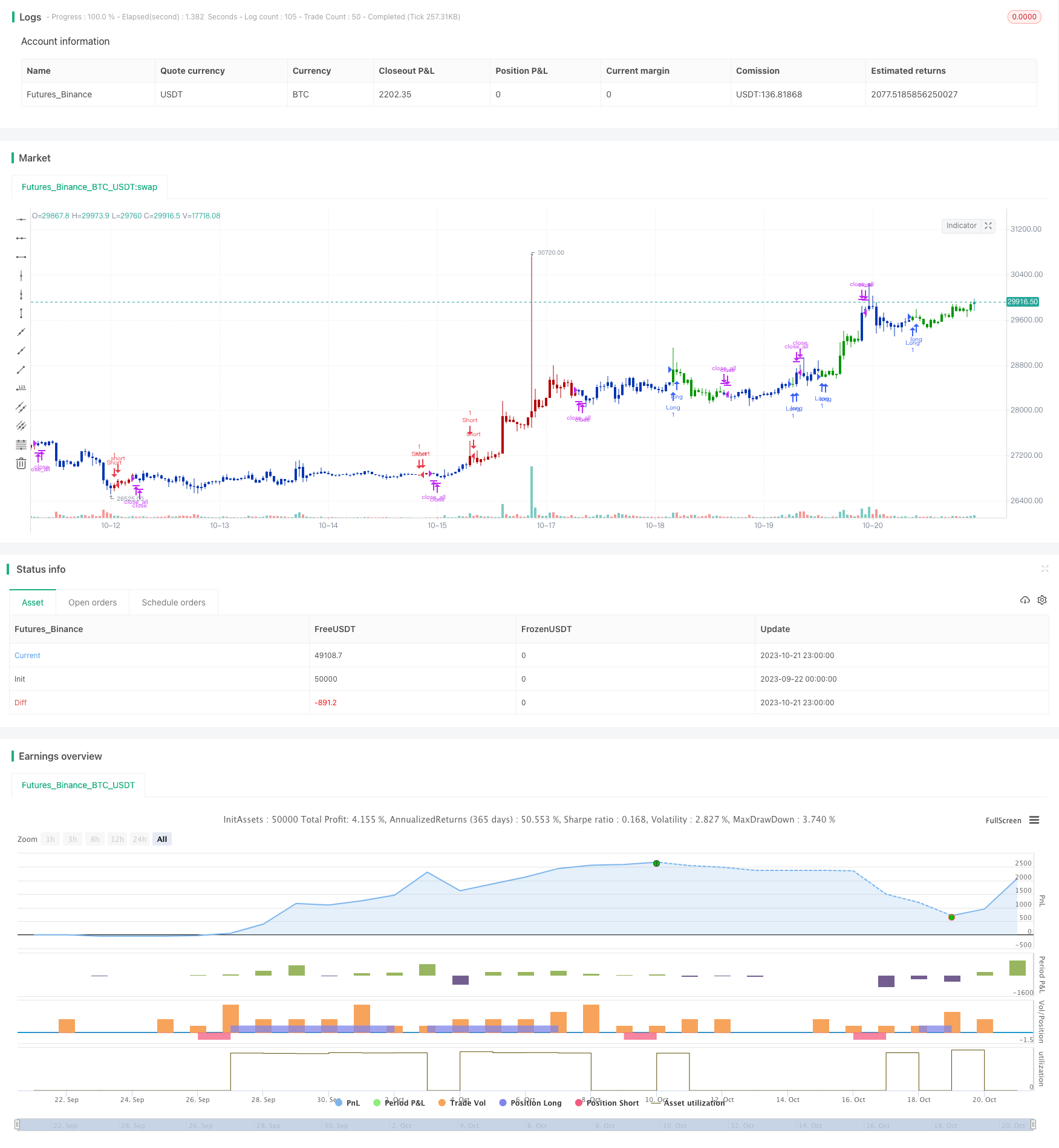

概述

本策略通过组合使用动量指标CMO和反转指标Stochastic,实现多因子模型,以发掘不同市场环境下的交易机会。

原理分析

该策略由两个子策略组成:

123反转策略

- 使用9日Stochastic指标判断超买超卖

- 如果收盘价连续2日上涨,且Stochastic低于50,做多

- 如果收盘价连续2日下跌,且Stochastic高于50,做空

CMO绝对值策略

- 计算CMO的绝对值

- CMO绝对值高于70时,认为处于超买状态,做空

- CMO绝对值低于20时,认为处于超卖状态,做多

最后,如果两个子策略信号一致,则发出交易信号。

该策略充分利用了动量指标CMO和反转指标Stochastic的优势。CMO能较好地识别趋势,Stochastic则可发现短期反转机会。两者结合使用,能在不同阶段发掘交易机会。

优势分析

本策略具有以下优势:

多因子模型,结合动量和反转,能适应不同市场环境

CMO识别趋势能力强,Stochastic判断反转点准确

只在两个信号一致时交易,避免错信号,提高获利概率

参数优化空间大,可以针对不同品种和周期进行调整

采用长短周期指标结合,能发现更多交易机会

规则简单清晰,容易理解实现,适合算法交易

风险分析

本策略也存在以下风险:

子策略发出错误信号的概率存在,需要优化参数

突发事件导致趋势反转,会产生较大亏损

交易频率可能过高,交易成本是需要考虑的因素

子策略均为延迟指标,存在时间滞后问题

需针对不同品种调整参数,对参数优化要求较高

对策:

优化子策略参数,降低错误信号概率

设置止损,控制单笔亏损

调整开仓条件,降低交易频率

使用实时tick数据,减少滞后问题

利用机器学习方法自动优化参数

优化方向

本策略可以从以下方面进行优化:

引入更多因子,如波动率、量价等,形成系统性的多因子模型

构建动态参数优化机制,根据市场情况调整参数

优化开仓逻辑,引入概率和指数平滑等方法

在短期内对冲长期仓位,实现双重目标

利用深度学习提取更多特征,建立非线性交易规则

探索无参数模型,避免人工选择参数带来的偏差

结合高频数据、新闻事件,减少信号滞后问题

总结

本策略通过运用动量指标CMO和反转指标Stochastic,实现多因子模型,在穿越式市场中发掘更多交易机会。相比单一指标,多因子组合能够适应更加复杂的市场环境。同时,本策略参数优化空间大、规则简单,适合算法交易开发。但是也需要注意风险控制,对参数选择和模型优化要求较高。总体来说,多因子动量反转策略是一个可供参考和拓展的系统化交易思路。

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 17/09/2019

// This is combo strategies for get a cumulative signal.

//

// First strategy

// This System was created from the Book "How I Tripled My Money In The

// Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

// The strategy buys at market, if close price is higher than the previous close

// during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

// The strategy sells at market, if close price is lower than the previous close price

// during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

//

// Second strategy

// This indicator plots the absolute value of CMO. CMO was developed by Tushar

// Chande. A scientist, an inventor, and a respected trading system developer,

// Mr. Chande developed the CMO to capture what he calls "pure momentum". For

// more definitive information on the CMO and other indicators we recommend the

// book The New Technical Trader by Tushar Chande and Stanley Kroll.

// The CMO is closely related to, yet unique from, other momentum oriented indicators

// such as Relative Strength Index, Stochastic, Rate-of-Change, etc. It is most closely

// related to Welles Wilder`s RSI, yet it differs in several ways:

// - It uses data for both up days and down days in the numerator, thereby directly

// measuring momentum;

// - The calculations are applied on unsmoothed data. Therefore, short-term extreme

// movements in price are not hidden. Once calculated, smoothing can be applied to

// the CMO, if desired;

// - The scale is bounded between +100 and -100, thereby allowing you to clearly see

// changes in net momentum using the 0 level. The bounded scale also allows you to

// conveniently compare values across different securities.

//

// WARNING:

// - For purpose educate only

// - This script to change bars colors.

////////////////////////////////////////////////////////////

Reversal123(Length, KSmoothing, DLength, Level) =>

vFast = sma(stoch(close, high, low, Length), KSmoothing)

vSlow = sma(vFast, DLength)

pos = 0.0

pos := iff(close[2] < close[1] and close > close[1] and vFast < vSlow and vFast > Level, 1,

iff(close[2] > close[1] and close < close[1] and vFast > vSlow and vFast < Level, -1, nz(pos[1], 0)))

pos

CMOabs(Length, TopBand, LowBand) =>

pos = 0

xMom = abs(close - close[1])

xSMA_mom = sma(xMom, Length)

xMomLength = close - close[Length]

nRes = abs(100 * (xMomLength / (xSMA_mom * Length)))

pos := iff(nRes > TopBand, -1,

iff(nRes < LowBand, 1, nz(pos[1], 0)))

pos

strategy(title="Combo Backtest 123 Reversal & CMOabs", shorttitle="Combo", overlay = true)

Length = input(14, minval=1)

KSmoothing = input(1, minval=1)

DLength = input(3, minval=1)

Level = input(50, minval=1)

//-------------------------

LengthCMO = input(9, minval=1)

TopBand = input(70, minval=1)

LowBand = input(20, maxval=0)

reverse = input(false, title="Trade reverse")

posReversal123 = Reversal123(Length, KSmoothing, DLength, Level)

posCMOabs = CMOabs(LengthCMO, TopBand, LowBand)

pos = iff(posReversal123 == 1 and posCMOabs == 1 , 1,

iff(posReversal123 == -1 and posCMOabs == -1, -1, 0))

possig = iff(reverse and pos == 1, -1,

iff(reverse and pos == -1 , 1, pos))

if (possig == 1)

strategy.entry("Long", strategy.long)

if (possig == -1)

strategy.entry("Short", strategy.short)

if (possig == 0)

strategy.close_all()

barcolor(possig == -1 ? #b50404: possig == 1 ? #079605 : #0536b3 )