概述

本策略通过识别快速上涨的股票,并在突破新高的时候建仓做多,采取固定百分比止盈的方式来获利。该策略属于趋势跟踪策略。

原理

该策略主要基于两个指标:

快速RSI:通过计算最近3根K线的涨跌变化,来判断价格动量。当快速RSI低于10时,视为股票处于超跌状态。

主体过滤:计算最近20根K线的实体平均大小,当价格实体大于平均实体的2.5倍时,视为有效突破。

当快速RSI低于10,且实体过滤有效时,进行做多开仓。之后设置20%的固定止盈点位,当价格超过开仓价*(1+止盈比例)时,平仓止盈。

该策略的优点是能捕捉趋势开始阶段的突破机会,通过快速RSI判断底部区域,实体过滤来避免假突破。采取固定止盈方式来锁定每单盈利,可以持续把握行情趋势。

优势分析

该策略具有以下优势:

利用快速RSI判断底部超跌区域,可以提高入场准确率。

主体过滤机制可以避免因震荡造成的假突破。

采取固定百分比止盈方式,可以持续获利,把握行情趋势。

策略逻辑简单清晰,容易理解实现。

代码结构优雅,可扩展性强,便于进行策略优化。

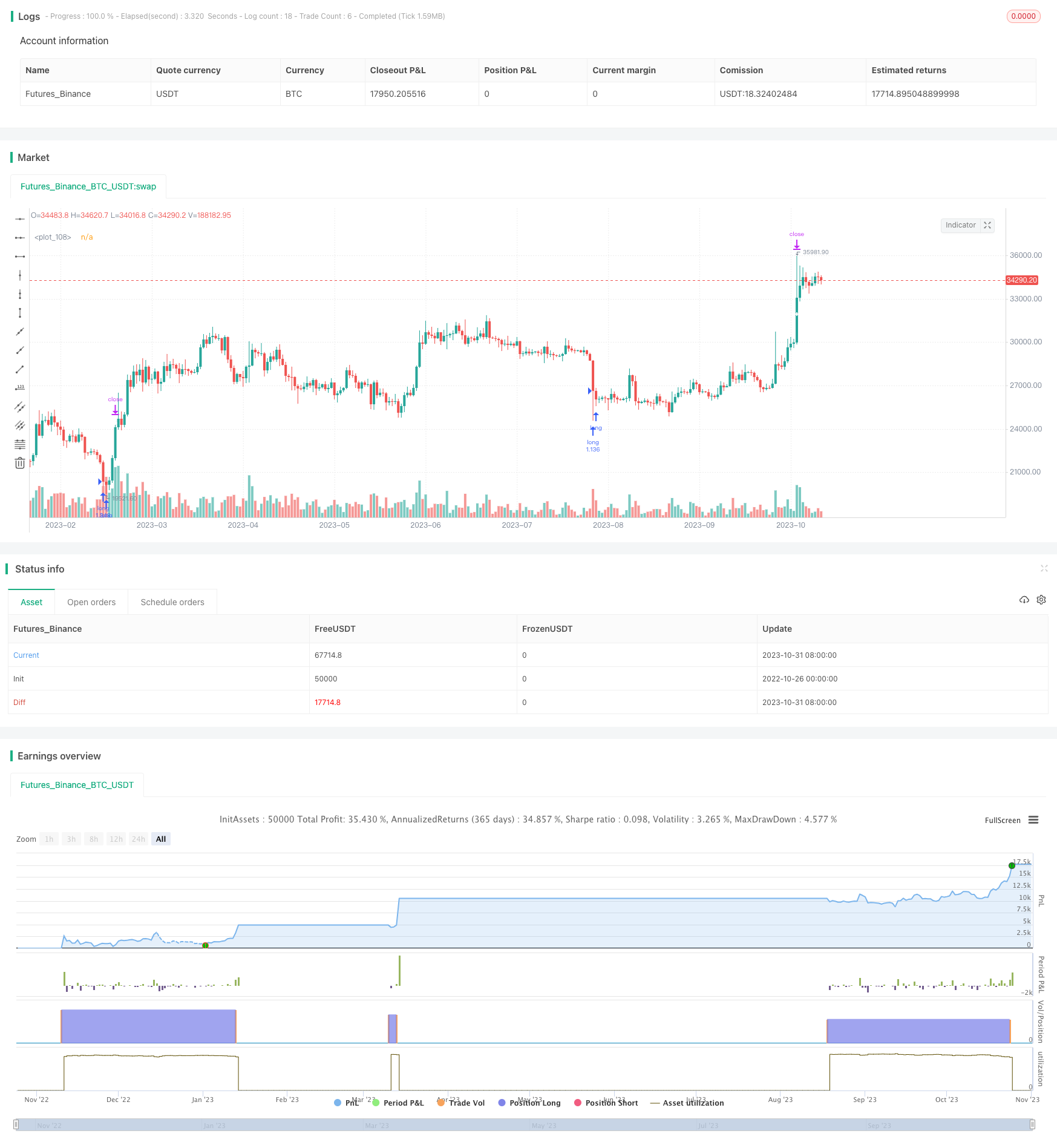

回测期内,策略获得稳定正收益,胜率较高。

风险分析

该策略也存在一些风险需要注意:

策略没有止损机制,存在单笔损失扩大的风险。

固定止盈点位设置不当可能导致过早止盈或止盈点过深。

行情震荡时,容易产生连续小亏损的情况。

未考虑融资融券成本,实盘时收益会有所减少。

策略参数优化不足,不同品种需要调整参数。

优化方向

该策略可以从以下方面进行优化:

增加止损机制,可以控制单笔损失。

优化止盈点位,使其能动态跟踪趋势。

优化突破的判断指标,提高入场的准确性。

增加仓位管理模块,优化仓位占用。

增加品种参数优化模块,自动优化不同品种的参数。

增加过滤条件,避免行情过于震荡时的亏损。

考虑加入仓位平均成本管理模块。

总结

本策略总体来说是一个非常简洁优雅的趋势跟踪策略。它利用快速RSI判断超跌,实体过滤确定有效突破,采取固定止盈点位获取稳定收益。虽然存在一些可优化的空间,但该策略响应敏捷,适合捕捉行情快速变化的场景,是一个非常实用的交易策略。通过不断优化,相信可以成为一个强大可靠的长线持仓策略。

/*backtest

start: 2022-10-26 00:00:00

end: 2023-11-01 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

// this is based on https://www.tradingview.com/v/PbQW4mRn/

strategy(title = "ONLY LONG V4 v1", overlay = true, initial_capital = 1000, pyramiding = 1000,

calc_on_order_fills = false, calc_on_every_tick = false, default_qty_type = strategy.percent_of_equity, default_qty_value = 50, commission_value = 0.075)

//study(title = "ONLY LONG V4 v1", overlay = true)

//Fast RSI

src = close

fastup = rma(max(change(src), 0), 3)

fastdown = rma(-min(change(src), 0), 3)

fastrsi = fastdown == 0 ? 100 : fastup == 0 ? 0 : 100 - (100 / (1 + fastup / fastdown))

//Body Filter

body = abs(close - open)

abody = sma(body, 20)

mac = sma(close, 20)

len = abs(close - mac)

sma = sma(len, 100)

max = max(open, close)

min = min(open, close)

up = close < open and len > sma * 2 and min < min[1] and fastrsi < 10 and body > abody * 2.5

// Strategy

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

var bool longCondition = na

longCondition := up == 1 ? 1 : na

// Get the price of the last opened long

var float last_open_longCondition = na

last_open_longCondition := longCondition ? close : nz(last_open_longCondition[1])

// Get the bar time of the last opened long

var int last_longCondition = 0

last_longCondition := longCondition ? time : nz(last_longCondition[1])

// Take profit

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

tp = input(20, "TAKE PROFIT %", type = input.float, minval = 0, step = 0.5)

long_tp = crossover(high, (1+(tp/100))*last_open_longCondition) and not longCondition

// Get the time of the last tp close

var int last_long_tp = na

last_long_tp := long_tp ? time : nz(last_long_tp[1])

Final_Long_tp = long_tp and last_longCondition > nz(last_long_tp[1])

// Count your long conditions

var int sectionLongs = 0

sectionLongs := nz(sectionLongs[1])

var int sectionTPs = 0

sectionTPs := nz(sectionTPs[1])

// Longs Counter

if longCondition

sectionLongs := sectionLongs + 1

sectionTPs := 0

if Final_Long_tp

sectionLongs := 0

sectionTPs := sectionTPs + 1

// Signals

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

// Long

// label.new(

// x = longCondition[1] ? time : na,

// y = na,

// text = 'LONG'+tostring(sectionLongs),

// color=color.lime,

// textcolor=color.black,

// style = label.style_labelup,

// xloc = xloc.bar_time,

// yloc = yloc.belowbar,

// size = size.tiny)

// Tp

// label.new(

// x = Final_Long_tp ? time : na,

// y = na,

// text = 'PROFIT '+tostring(tp)+'%',

// color=color.orange,

// textcolor=color.black,

// style = label.style_labeldown,

// xloc = xloc.bar_time,

// yloc = yloc.abovebar,

// size = size.tiny)

ltp = iff(Final_Long_tp, (last_open_longCondition*(1+(tp/100))), na), plot(ltp, style=plot.style_cross, linewidth=3, color = color.white, editable = false)

// Backtesting

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

testStartYear = input(2019, "BACKTEST START YEAR", minval = 1, maxval = 2222)

testStartMonth = input(01, "BACKTEST START MONTH", minval = 1, maxval = 12)

testStartDay = input(01, "BACKTEST START DAY", minval = 1, maxval = 31)

testPeriodStart = timestamp(testStartYear,testStartMonth,testStartDay,0,0)

strategy.entry("long", strategy.long, when = longCondition and (time >= testPeriodStart))

strategy.exit("TP", "long", limit = (last_open_longCondition*(1+(tp/100))))

// Alerts

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

alertcondition(longCondition[1], title="Long Alert", message = "LONG")

alertcondition(Final_Long_tp, title="Long TP Alert", message = "LONG TP")