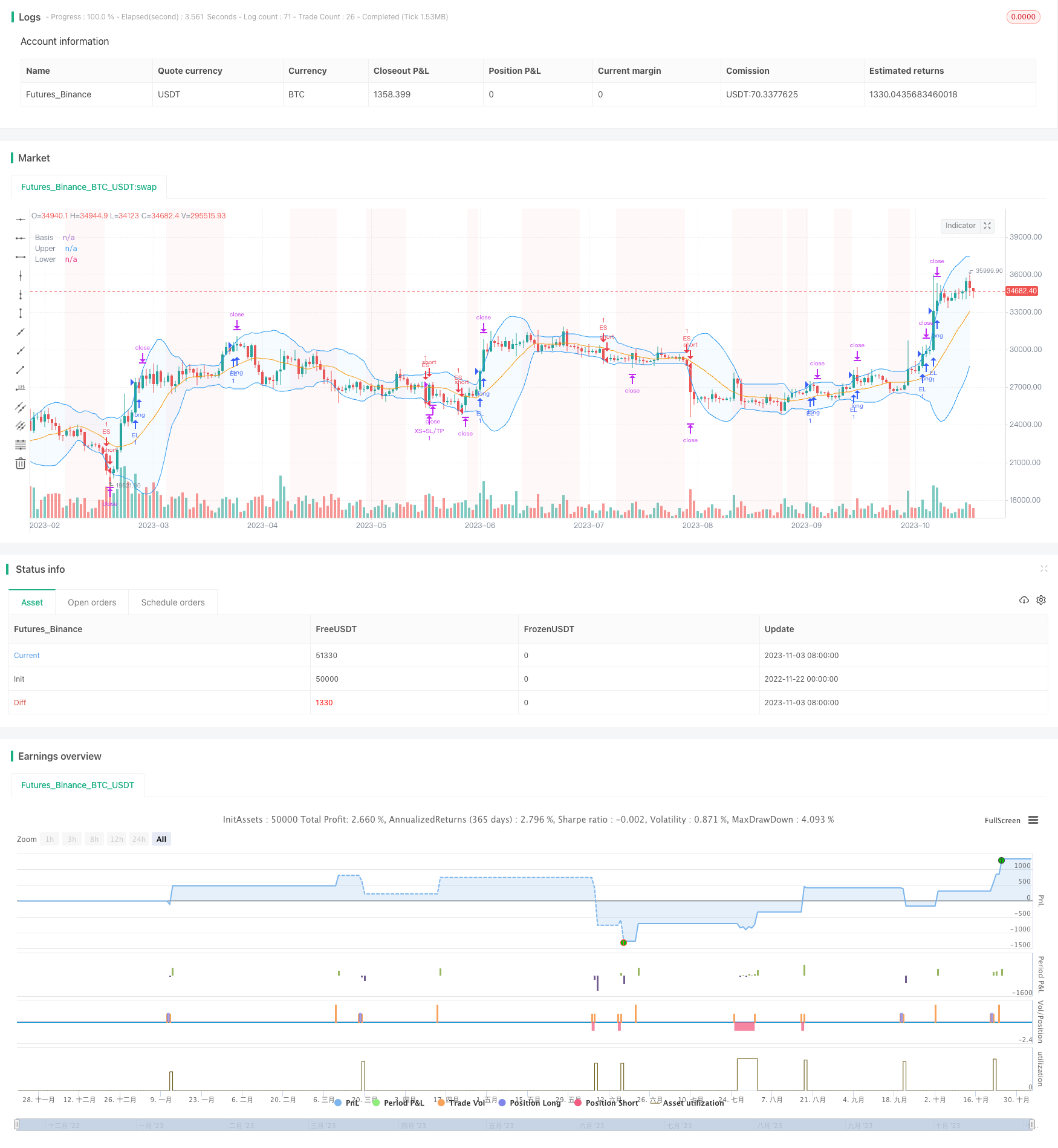

概述

布林带突破策略是一个基于布林带指标的短期趋势跟踪型策略。它可以执行多头和空头两种方向的操作,适用于现货和永续合约,尤其适用于趋势行情。

该策略具有高度的可配置性,允许用户设置布林带的参数期间和偏差,趋势过滤器,波动性过滤器,交易方向过滤器,变化率过滤器和日期过滤器等。此外,它还为多头和空头仓位设置了止损,止盈和跟踪止损,确保全面的风险管理方法。每日最大亏损的加入提供了另一层保护,使其成为一个值得信赖的专业化自适应交易系统。

策略原理

该策略的核心指标是布林带。布林带由中轨、上轨和下轨三条线组成,代表价格的均值线、波动的上限和波动的下限。当价格突破上轨时,做多;当价格突破下轨时,做空。

此外,策略还设置了多个辅助过滤器,避免Noise交易。这些过滤器包括:

趋势过滤器:价格在移动平均线上方做多,价格在移动平均线下方做空;

波动性过滤器:仅在波动性扩大时交易;

交易方向过滤器:根据标的属性选择只做多、只做空或双向交易;

变化率过滤器:价格相对前一交易日收盘价的变化率达到一定水平时才进入;

日期过滤器:用于回测的时间区间设置。

当所有过滤条件满足时产生交易信号。止盈、止损和跟踪止损确保风险管理。此外,最大日内亏损设置避免单日大幅回撤。

优势分析

该策略具有以下优势:

采用布林带这个成熟指标作为核心交易信号,可靠性高;

多重过滤器设计避免误交易,可配置性强;

止盈、止损、跟踪止损全面、灵活;

最大日内亏损设置有效控制单日回撤。

适合趋势市,收益潜力大。

风险分析

该策略也存在一定风险:

布林带突破容易形成头部假突破和底部假突破,可能造成损失;

在盘整市中,过滤器可能过于严格,错过交易机会;

大幅度跳空可能直接突破止损线造成损失;

极端行情中,无法完全避免巨额亏损。

针对上述风险,可以适当放宽过滤条件,或人工干预关闭部分仓位,降低止损距离等。

优化方向

该策略可以考虑从以下几个方面进行优化:

尝试不同的参数组合,寻找最佳的参数区间;

增加机器学习模型,实现参数的动态优化;

研究更有效的止损方式,如时间止损,振幅止损等;

结合情绪指标,在极端行情中主动干预;

结合相关产品,进行统计套利。

总结

布林带突破策略是一个成熟可靠的短线趋势跟随策略。它采用布林带指标作为信号,并设置了多重过滤器确保信号的可靠性。同时,全面的止损和风控机制控制了风险。该策略适合活跃的趋势市,具有良好的收益潜力。通过不断优化,有望成为一个强大的量化交易系统。

/*backtest

start: 2022-11-22 00:00:00

end: 2023-11-04 05:20:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Bollinger Bands - Breakout Strategy",overlay=true

)

// Define the length of the Bollinger Bands

bbLengthInput = input.int (15,title="Length", group="Bollinger Bands", inline="BB")

bbDevInput = input.float (2.0,title="StdDev", group="Bollinger Bands", inline="BB")

// Define the settings for the Trend Filter

trendFilterInput = input.bool(false, title="Above/Below", group = "Trend Filter", inline="Trend")

trendFilterPeriodInput = input(223,title="", group = "Trend Filter", inline="Trend")

trendFilterType = input.string (title="", defval="EMA",options=["EMA","SMA","RMA", "WMA"], group = "Trend Filter", inline="Trend")

volatilityFilterInput = input.bool(true,title="StdDev", group = "Volatility Filter", inline="Vol")

volatilityFilterStDevLength = input(15,title="",group = "Volatility Filter", inline="Vol")

volatilityStDevMaLength = input(15,title=">MA",group = "Volatility Filter", inline="Vol")

// ROC Filter

// f_security function by LucF for PineCoders available here: https://www.tradingview.com/script/cyPWY96u-How-to-avoid-repainting-when-using-security-PineCoders-FAQ/

f_security(_sym, _res, _src, _rep) => request.security(_sym, _res, _src[not _rep and barstate.isrealtime ? 1 : 0])[_rep or barstate.isrealtime ? 0 : 1]

high_daily = f_security(syminfo.tickerid, "D", high, false)

roc_enable = input.bool(false, "", group="ROC Filter from CloseD", inline="roc")

roc_threshold = input.float(1, "Treshold", step=0.5, group="ROC Filter from CloseD", inline="roc")

closed = f_security(syminfo.tickerid,"1D",close, false)

roc_filter= roc_enable ? (close-closed)/closed*100 > roc_threshold : true

// Trade Direction Filter

// tradeDirectionInput = input.string("Auto",options=["Auto", "Long&Short","Long Only", "Short Only"], title="Trade", group="Direction Filter", tooltip="Auto: if a PERP is detected (in the symbol description), trade long and short\n Otherwise as per user-input")

// tradeDirection = switch tradeDirectionInput

// "Auto" => str.contains(str.lower(syminfo.description), "perp") or str.contains(str.lower(syminfo.description), ".p") ? strategy.direction.all : strategy.direction.long

// "Long&Short" => strategy.direction.all

// "Long Only" => strategy.direction.long

// "Short Only" => strategy.direction.short

// => strategy.direction.all

// strategy.risk.allow_entry_in(tradeDirection)

// Calculate and plot the Bollinger Bands

[bbMiddle, bbUpper, bbLower] = ta.bb (close, bbLengthInput, bbDevInput)

plot(bbMiddle, "Basis", color=color.orange)

bbUpperPlot = plot(bbUpper, "Upper", color=color.blue)

bbLowerrPlot = plot(bbLower, "Lower", color=color.blue)

fill(bbUpperPlot, bbLowerrPlot, title = "Background", color=color.new(color.blue, 95))

// Calculate and view Trend Filter

float tradeConditionMa = switch trendFilterType

"EMA" => ta.ema(close, trendFilterPeriodInput)

"SMA" => ta.sma(close, trendFilterPeriodInput)

"RMA" => ta.rma(close, trendFilterPeriodInput)

"WMA" => ta.wma(close, trendFilterPeriodInput)

// Default used when the three first cases do not match.

=> ta.wma(close, trendFilterPeriodInput)

trendConditionLong = trendFilterInput ? close > tradeConditionMa : true

trendConditionShort = trendFilterInput ? close < tradeConditionMa : true

plot(trendFilterInput ? tradeConditionMa : na, color=color.yellow)

// Calculate and view Volatility Filter

stdDevClose = ta.stdev(close,volatilityFilterStDevLength)

volatilityCondition = volatilityFilterInput ? stdDevClose > ta.sma(stdDevClose,volatilityStDevMaLength) : true

bbLowerCrossUnder = ta.crossunder(close, bbLower)

bbUpperCrossOver = ta.crossover(close, bbUpper)

bgcolor(volatilityCondition ? na : color.new(color.red, 95))

// Date Filter

start = input(timestamp("2017-01-01"), "Start", group="Date Filter")

finish = input(timestamp("2050-01-01"), "End", group="Date Filter")

date_filter = true

// Entry and Exit Conditions

entryLongCondition = bbUpperCrossOver and trendConditionLong and volatilityCondition and date_filter and roc_filter

entryShortCondition = bbLowerCrossUnder and trendConditionShort and volatilityCondition and date_filter and roc_filter

exitLongCondition = bbLowerCrossUnder

exitShortCondition = bbUpperCrossOver

// Orders

if entryLongCondition

strategy.entry("EL", strategy.long)

if entryShortCondition

strategy.entry("ES", strategy.short)

if exitLongCondition

strategy.close("EL")

if exitShortCondition

strategy.close("ES")

// Long SL/TP/TS

xl_ts_percent = input.float(2,step=0.5, title= "TS", group="Exit Long", inline="LTS", tooltip="Trailing Treshold %")

xl_to_percent = input.float(0.5, step=0.5, title= "TO", group="Exit Long", inline="LTS", tooltip="Trailing Offset %")

xl_ts_tick = xl_ts_percent * close/syminfo.mintick/100

xl_to_tick = xl_to_percent * close/syminfo.mintick/100

xl_sl_percent = input.float (2, step=0.5, title="SL",group="Exit Long", inline="LSLTP")

xl_tp_percent = input.float(9, step=0.5, title="TP",group="Exit Long", inline="LSLTP")

xl_sl_price = strategy.position_avg_price * (1-xl_sl_percent/100)

xl_tp_price = strategy.position_avg_price * (1+xl_tp_percent/100)

strategy.exit("XL+SL/TP", "EL", stop=xl_sl_price, limit=xl_tp_price, trail_points=xl_ts_tick, trail_offset=xl_to_tick,comment_loss= "XL-SL", comment_profit = "XL-TP",comment_trailing = "XL-TS")

// Short SL/TP/TS

xs_ts_percent = input.float(2,step=0.5, title= "TS",group="Exit Short", inline ="STS", tooltip="Trailing Treshold %")

xs_to_percent = input.float(0.5, step=0.5, title= "TO",group="Exit Short", inline ="STS", tooltip="Trailing Offset %")

xs_ts_tick = xs_ts_percent * close/syminfo.mintick/100

xs_to_tick = xs_to_percent * close/syminfo.mintick/100

xs_sl_percent = input.float (2, step=0.5, title="SL",group="Exit Short", inline="ESSLTP", tooltip="Stop Loss %")

xs_tp_percent = input.float(9, step=0.5, title="TP",group="Exit Short", inline="ESSLTP", tooltip="Take Profit %")

xs_sl_price = strategy.position_avg_price * (1+xs_sl_percent/100)

xs_tp_price = strategy.position_avg_price * (1-xs_tp_percent/100)

strategy.exit("XS+SL/TP", "ES", stop=xs_sl_price, limit=xs_tp_price, trail_points=xs_ts_tick, trail_offset=xs_to_tick,comment_loss= "XS-SL", comment_profit = "XS-TP",comment_trailing = "XS-TS")

max_intraday_loss = input.int(10, title="Max Intraday Loss (Percent)", group="Risk Management")

//strategy.risk.max_intraday_loss(max_intraday_loss, strategy.percent_of_equity)

// Monthly Returns table, modified from QuantNomad. Please put calc_on_every_tick = true to plot it.

monthly_table(int results_prec, bool results_dark) =>

new_month = month(time) != month(time[1])

new_year = year(time) != year(time[1])

eq = strategy.equity

bar_pnl = eq / eq[1] - 1

cur_month_pnl = 0.0

cur_year_pnl = 0.0

// Current Monthly P&L

cur_month_pnl := new_month ? 0.0 :

(1 + cur_month_pnl[1]) * (1 + bar_pnl) - 1

// Current Yearly P&L

cur_year_pnl := new_year ? 0.0 :

(1 + cur_year_pnl[1]) * (1 + bar_pnl) - 1

// Arrays to store Yearly and Monthly P&Ls

var month_pnl = array.new_float(0)

var month_time = array.new_int(0)

var year_pnl = array.new_float(0)

var year_time = array.new_int(0)

last_computed = false

if (not na(cur_month_pnl[1]) and (new_month or barstate.islast))

if (last_computed[1])

array.pop(month_pnl)

array.pop(month_time)

array.push(month_pnl , cur_month_pnl[1])

array.push(month_time, time[1])

if (not na(cur_year_pnl[1]) and (new_year or barstate.islast))

if (last_computed[1])

array.pop(year_pnl)

array.pop(year_time)

array.push(year_pnl , cur_year_pnl[1])

array.push(year_time, time[1])

last_computed := barstate.islast ? true : nz(last_computed[1])

// Monthly P&L Table

var monthly_table = table(na)

cell_hr_bg_color = results_dark ? #0F0F0F : #F5F5F5

cell_hr_text_color = results_dark ? #D3D3D3 : #555555

cell_border_color = results_dark ? #000000 : #FFFFFF

// ell_hr_bg_color = results_dark ? #0F0F0F : #F5F5F5

// cell_hr_text_color = results_dark ? #D3D3D3 : #555555

// cell_border_color = results_dark ? #000000 : #FFFFFF

if (barstate.islast)

monthly_table := table.new(position.bottom_right, columns = 14, rows = array.size(year_pnl) + 1, bgcolor=cell_hr_bg_color,border_width=1,border_color=cell_border_color)

table.cell(monthly_table, 0, 0, syminfo.tickerid + " " + timeframe.period, text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 1, 0, "Jan", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 2, 0, "Feb", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 3, 0, "Mar", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 4, 0, "Apr", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 5, 0, "May", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 6, 0, "Jun", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 7, 0, "Jul", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 8, 0, "Aug", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 9, 0, "Sep", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 10, 0, "Oct", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 11, 0, "Nov", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 12, 0, "Dec", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

table.cell(monthly_table, 13, 0, "Year", text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

for yi = 0 to array.size(year_pnl) - 1

table.cell(monthly_table, 0, yi + 1, str.tostring(year(array.get(year_time, yi))), text_color=cell_hr_text_color, bgcolor=cell_hr_bg_color)

y_color = array.get(year_pnl, yi) > 0 ? color.lime : array.get(year_pnl, yi) < 0 ? color.red : color.gray

table.cell(monthly_table, 13, yi + 1, str.tostring(math.round(array.get(year_pnl, yi) * 100, results_prec)), bgcolor = y_color)

for mi = 0 to array.size(month_time) - 1

m_row = year(array.get(month_time, mi)) - year(array.get(year_time, 0)) + 1

m_col = month(array.get(month_time, mi))

m_color = array.get(month_pnl, mi) > 0 ? color.lime : array.get(month_pnl, mi) < 0 ? color.red : color.gray

table.cell(monthly_table, m_col, m_row, str.tostring(math.round(array.get(month_pnl, mi) * 100, results_prec)), bgcolor = m_color)

results_prec = input(2, title = "Precision", group="Results Table")

results_dark = input.bool(defval=true, title="Dark Mode", group="Results Table")

monthly_table(results_prec, results_dark)