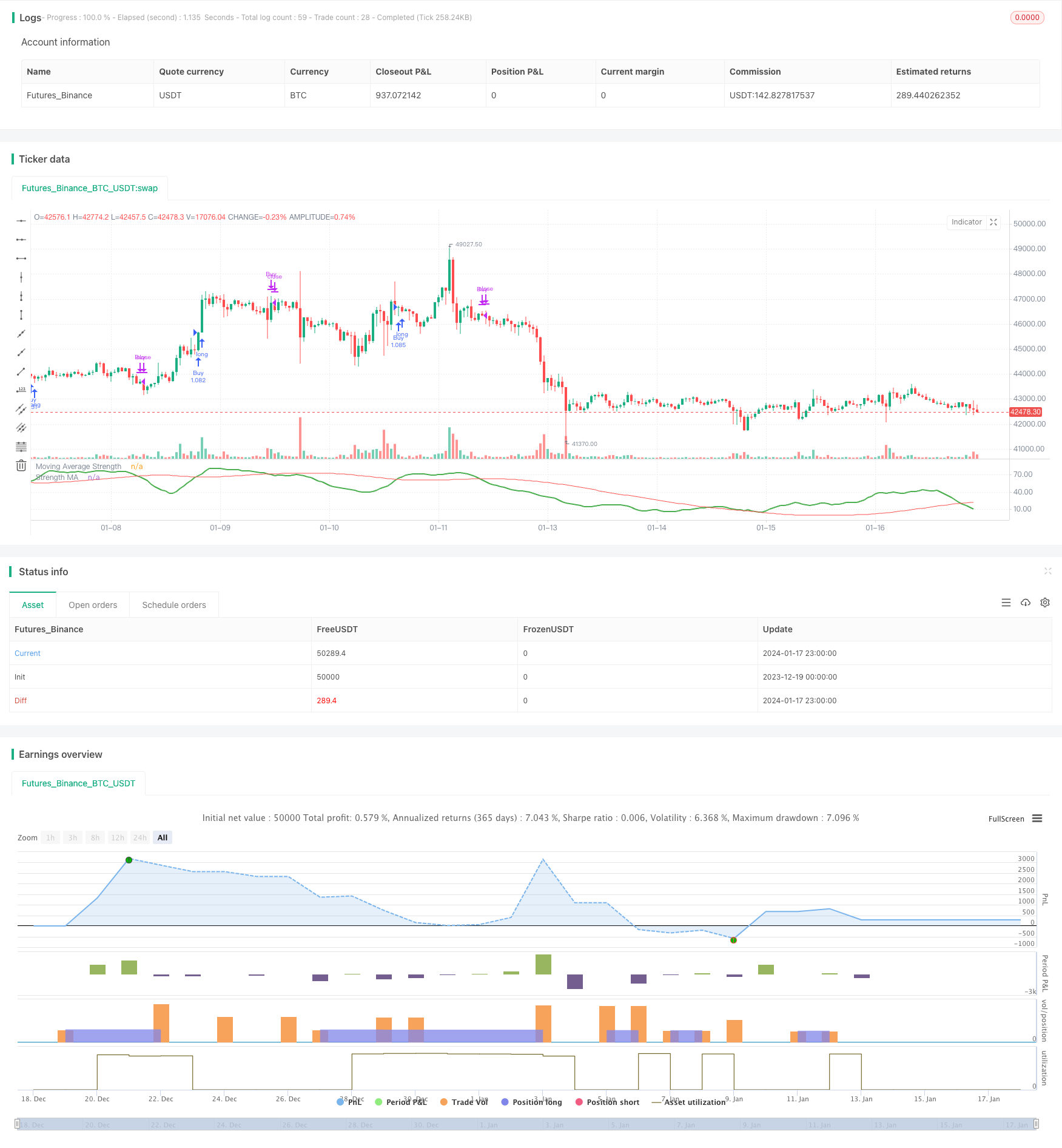

概述

该策略通过计算多时间段的移动平均线(MA)强弱情况,评估市场趋势强弱,实现对趋势的判断和追踪。当短期MA指标连续上扬,记高分,形成“MA强度”指标。当该指标超过其本身的长期MA时,产生买入信号。策略可配置长短期MA组合,追踪不同周期趋势。

策略原理

- 计算5日、10日、20日等多组MA,判断价格是否突破每个MA向上,突破记分,积分形成“MA强度”。

- 对“MA强度”应用移动平均线,形成均线指标,判断均线多空,产生交易信号。

- 可配置追踪周期参数:短期MA组数、长期均线周期、开仓条件等。

该策略主要判定均线指标的多空,通过均线指标反应MA线组的平均强度。MA线组集中判断趋势方向和力度,均线指标判断持续性。

优势分析

- 评估趋势力度的多维度模型。单一MA线无法确定力度足够;该策略测量多MA突破,确保力度足够后发出信号,可靠性高。

- 可配置追踪周期。调整短期MA参数可捕捉不同级别趋势;调整长期MA参数可控制出场节奏。用户可根据市场调整周期。

- 仅做多可避免错杀,跟踪长期上涨趋势。策略仅做多,只追涨不追跌,可减少反转损失。

风险分析

- 存在回撤风险。当短线均线下穿长线均线时,存在较大回撤的风险。可通过止损方式减少单笔损失。

- 存在反转风险。市场长期运行必然存在调整,策略必须及时止损Exiting。建议结合波段、通道等技术判断大周期末,控制反转风险。

- 参数风险。不当的参数配置可能得到错误信号。应调整参数适合不同品种,确保参数稳定。

优化方向

- 结合更多指标过滤进场。可考虑结合成交量,在量能验证下发出信号,避免假突破。

- 增加止损方式。移动止损、曲线止损可在回调中减少损失。止盈方式也可考虑,锁定利润,避免反转。

- 考虑配置期货、外汇品种。MA线突破更适合趋势性品种。可评估不同期货品种的参数稳定性,选择最佳品种。

总结

该策略通过计算MA强度指标判断价格趋势,并以均线交叉作为信号源,进行趋势追踪。策略优势是准确判断趋势力度,可靠性较高。主要风险在于趋势反转和参数调整。通过优化入场信号准确性,增加止损方式,选择合适品种,可以获得较好收益。

策略源码

/*backtest

start: 2023-12-19 00:00:00

end: 2024-01-18 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © HeWhoMustNotBeNamed

//@version=4

strategy("MA Strength Strategy", overlay=false, initial_capital = 20000, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, commission_type = strategy.commission.percent, pyramiding = 1, commission_value = 0.01)

MAType = input(title="Moving Average Type", defval="ema", options=["ema", "sma", "hma", "rma", "vwma", "wma"])

LookbackPeriod = input(10, step=10)

IndexMAType = input(title="Moving Average Type", defval="hma", options=["ema", "sma", "hma", "rma", "vwma", "wma"])

IndexMAPeriod = input(200, step=10)

considerTrendDirection = input(true)

considerTrendDirectionForExit = input(true)

offset = input(1, step=1)

tradeDirection = input(title="Trade Direction", defval=strategy.direction.long, options=[strategy.direction.all, strategy.direction.long, strategy.direction.short])

i_startTime = input(defval = timestamp("01 Jan 2010 00:00 +0000"), title = "Start Time", type = input.time)

i_endTime = input(defval = timestamp("01 Jan 2099 00:00 +0000"), title = "End Time", type = input.time)

inDateRange = true

f_getMovingAverage(source, MAType, length)=>

ma = sma(source, length)

if(MAType == "ema")

ma := ema(source,length)

if(MAType == "hma")

ma := hma(source,length)

if(MAType == "rma")

ma := rma(source,length)

if(MAType == "vwma")

ma := vwma(source,length)

if(MAType == "wma")

ma := wma(source,length)

ma

f_getMaAlignment(MAType, includePartiallyAligned)=>

ma5 = f_getMovingAverage(close,MAType,5)

ma10 = f_getMovingAverage(close,MAType,10)

ma20 = f_getMovingAverage(close,MAType,20)

ma30 = f_getMovingAverage(close,MAType,30)

ma50 = f_getMovingAverage(close,MAType,50)

ma100 = f_getMovingAverage(close,MAType,100)

ma200 = f_getMovingAverage(close,MAType,200)

upwardScore = 0.0

upwardScore := close > ma5? upwardScore+1.10:upwardScore

upwardScore := ma5 > ma10? upwardScore+1.10:upwardScore

upwardScore := ma10 > ma20? upwardScore+1.10:upwardScore

upwardScore := ma20 > ma30? upwardScore+1.10:upwardScore

upwardScore := ma30 > ma50? upwardScore+1.15:upwardScore

upwardScore := ma50 > ma100? upwardScore+1.20:upwardScore

upwardScore := ma100 > ma200? upwardScore+1.25:upwardScore

upwards = close > ma5 and ma5 > ma10 and ma10 > ma20 and ma20 > ma30 and ma30 > ma50 and ma50 > ma100 and ma100 > ma200

downwards = close < ma5 and ma5 < ma10 and ma10 < ma20 and ma20 < ma30 and ma30 < ma50 and ma50 < ma100 and ma100 < ma200

trendStrength = upwards?1:downwards?-1:includePartiallyAligned ? (upwardScore > 6? 0.5: upwardScore < 2?-0.5:upwardScore>4?0.25:-0.25) : 0

[trendStrength, upwardScore]

includePartiallyAligned = true

[trendStrength, upwardScore] = f_getMaAlignment(MAType, includePartiallyAligned)

upwardSum = sum(upwardScore, LookbackPeriod)

indexSma = f_getMovingAverage(upwardSum,IndexMAType,IndexMAPeriod)

plot(upwardSum, title="Moving Average Strength", color=color.green, linewidth=2, style=plot.style_linebr)

plot(indexSma, title="Strength MA", color=color.red, linewidth=1, style=plot.style_linebr)

buyCondition = crossover(upwardSum,indexSma) and (upwardSum > upwardSum[offset] or not considerTrendDirection)

sellCondition = crossunder(upwardSum,indexSma) and (upwardSum < upwardSum[offset] or not considerTrendDirection)

exitBuyCondition = crossunder(upwardSum,indexSma)

exitSellCondition = crossover(upwardSum,indexSma)

strategy.risk.allow_entry_in(tradeDirection)

strategy.entry("Buy", strategy.long, when= inDateRange and buyCondition, oca_name="oca_buy")

strategy.close("Buy", when = considerTrendDirectionForExit? sellCondition : exitBuyCondition)

strategy.entry("Sell", strategy.short, when= inDateRange and sellCondition, oca_name="oca_sell")

strategy.close( "Sell", when = considerTrendDirectionForExit? buyCondition : exitSellCondition)