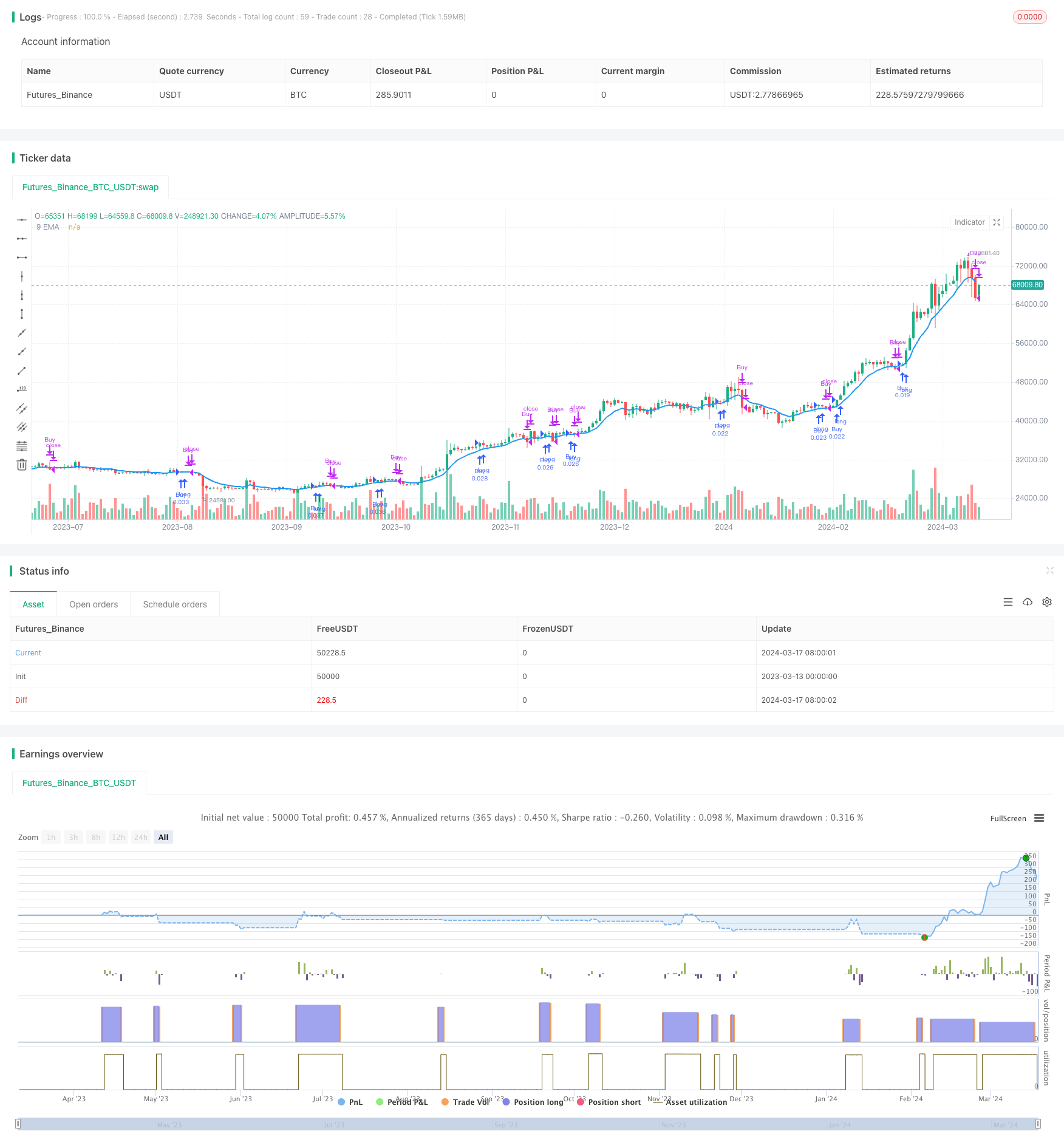

策略概述

该策略采用9周期指数移动平均线(9EMA)作为趋势判断依据,在交易日开盘10分钟内,如果连续两根5分钟K线的收盘价都非常接近最高价(大于等于最高价的99%),且收盘价位于9EMA之上,则认为出现了强势突破信号,此时以当前收盘价计算仓位大小,开仓做多。持仓直到出现第一根收盘价跌破9EMA的5分钟K线时平仓。

策略原理

该策略基于以下原理:

- 在交易日开盘阶段,如果市场出现强势突破走势,通常意味着后市有望延续强势上涨。

- 9EMA是一个相对敏感的趋势判断指标,价格站上9EMA往往意味着多头占据优势。

- 连续两根K线收盘价都非常接近最高价,说明多头力量强劲,买盘积极性高。

- 在强势趋势出现后,采用固定资金额来确定仓位大小,既可以控制风险,又能充分利用趋势行情。

- 当价格跌破9EMA时,往往意味着趋势出现了转折,此时及时平仓,可以最大限度地保护利润。

该策略通过捕捉交易日开盘阶段的强势突破行情,以动态仓位的方式参与,力求以较小风险博取较大收益。同时,该策略也采用了严格的止损条件,一旦趋势反转即果断平仓,控制回撤。

策略优势

- 交易时间集中在开盘前10分钟,把握早盘行情,交易频率低,可操作性强。

- 采用连续两根K线突破的方式来确认趋势,可以有效过滤假突破,提高信号可靠性。

- 仓位大小根据突破点的价格水平动态调整,可以自动适应不同时期的行情特点,风险可控。

- 止损条件明确,严格执行,可以有效控制单次交易的最大亏损。

- 策略逻辑简单,容易理解和执行,适合大多数交易者使用。

策略风险

- 开盘阶段虽然经常出现趋势性机会,但有时也会出现较大的波动和反复,面临一定的假突破风险。

- 策略在连续两根K线满足条件时即开仓,如果开仓后行情出现快速反转,仍有可能面临一定亏损。

- 固定资金额的仓位控制方式虽然简单,但在行情剧烈波动时,策略的收益率波动可能也会较大。

- 该策略只能捕捉到单边上涨行情,对于震荡行情和下跌趋势行情,并不适用。

针对上述风险,可以考虑从以下方面进行优化和改进:

- 加入开盘价与前一日收盘价之间的关系作为过滤条件,提高趋势判断的准确性。

- 优化止损条件,例如加入移动止损或者条件单止损,以进一步降低单次交易的风险敞口。

- 在趋势延续阶段,可以考虑采用金字塔加仓的方法,提高总体收益率。

- 尝试将该策略与其他适用于震荡行情或下跌趋势的策略进行组合,提高策略的适应性。

优化方向

- 引入更多有效的趋势判断指标,如MACD、布林带等,综合多个指标来确认趋势信号,提高开仓信号的可靠性,降低假突破风险。

- 对开仓时间窗口进行优化,可以考虑将10分钟的时间窗口缩短至5分钟或者延长至15分钟,通过回测对比,找出最佳的开仓时间。这样可以在把握趋势的同时,尽量降低初期波动的影响。

- 在仓位控制方面,可以考虑引入波动率因子,例如根据ATR(平均真实波动幅度)来动态调整每次开仓的资金比例,在波动较大时减少仓位,波动较小时加大仓位,使策略更好地适应不同的市场节奏。

- 优化止损条件,在保持原有9EMA止损逻辑的基础上,可以加入移动止损策略,即在价格向有利方向移动一定比例后,将止损位上移至成本价或者开仓价附近,从而降低回撤,锁定部分利润。

- 考虑加入一些过滤条件,例如成交量、波动率等,在开仓信号出现时,判断这些指标是否同步向好,以进一步确认趋势的有效性。这样可以帮助策略规避一些陷阱和假信号。

通过以上优化,该策略有望在趋势捕捉的同时,更好地控制风险,提高策略收益的稳定性和可持续性。当然,任何优化都需要通过严格的回测来验证其有效性,并根据实际情况进行动态调整。

总结

该策略以9EMA为核心,通过连续两根5分钟K线收盘价强势突破9EMA的方式,在交易日开盘10分钟内捕捉强势上涨行情,并采用固定资金额动态调整仓位的方式进行交易。该策略逻辑简单明了,易于理解和执行,适合大多数交易者使用。同时,该策略也存在一定的局限性和风险,例如对于震荡行情和下跌趋势行情的适应性不足,以及开仓后的快速反转风险等。针对这些问题,可以从趋势判断、仓位控制、止损优化、过滤条件等方面进行改进和优化,使策略能够更好地把握市场机会,控制风险。总的来说,该策略思路清晰,可塑性较强,值得进一步探索和实践。

策略源码

/*backtest

start: 2023-03-13 00:00:00

end: 2024-03-18 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy("Two 5min Closes Above 9EMA Strategy with Dynamic Position Size", overlay=true)

// Define the fixed amount for position sizing

fixedAmount = 1000

// Calculate the 9-period EMA

ema9 = ta.ema(close, 9)

// Define time constraints (9:30 AM to 9:40 AM EST, adjust for your timezone)

sessionStart = 0930

sessionEnd = 0940

timeCondition = (hour * 100 + minute) >= sessionStart and (hour * 100 + minute) < sessionEnd

// Detect two consecutive 5-min bars where close is near 0.99 times the high and above 9 EMA

closeNearHighAndAboveEMA = close >= high * 0.99 and close > ema9

twoConsecutiveBars = closeNearHighAndAboveEMA and closeNearHighAndAboveEMA[1]

// Entry condition: Within the first 10 minutes of the day and two consecutive bars match criteria

entryCondition = twoConsecutiveBars

// Exit condition: First 5-min close below 9 EMA after entry

exitCondition = close < ema9

// Plot EMA for visualization

plot(ema9, color=color.blue, linewidth=2, title="9 EMA")

// Calculate position size

positionSize = fixedAmount / close

// Strategy execution

if (entryCondition)

strategy.entry("Buy", strategy.long, qty=positionSize)

if (exitCondition)

strategy.close("Buy")