Heiken Ashi und Super Trend Kombinationsstrategie

Schriftsteller:ChaoZhang, Datum: 2023-12-15 11:11:27Tags:

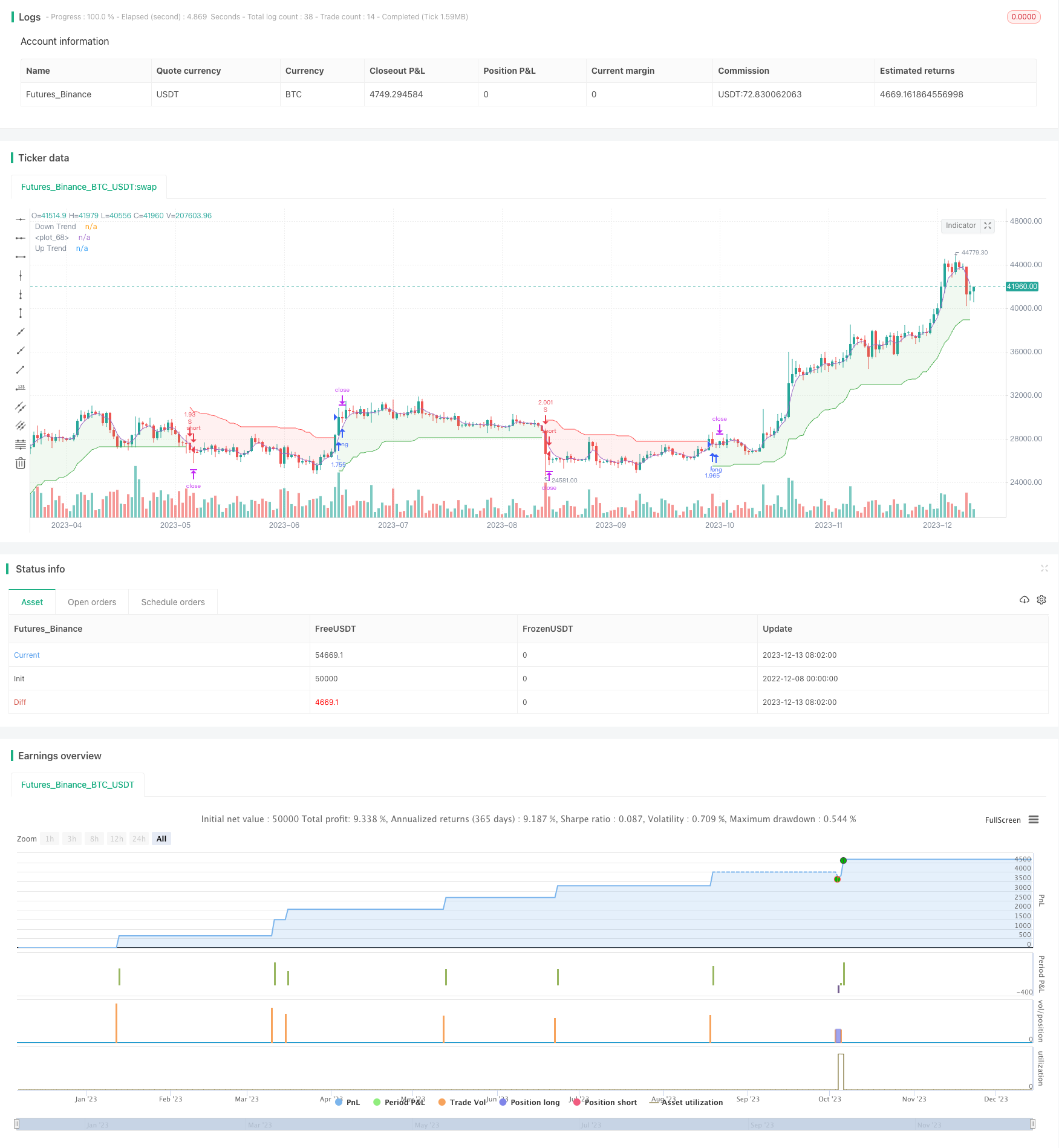

Übersicht

Dies ist eine quantitative Handelsstrategie, die die Indikatoren Heiken Ashi und Super Trend kombiniert. Die Strategie verwendet hauptsächlich Heiken Ashi, um Kerzen zu glätten und Marktlärm zu filtern, und verwendet den Super Trend-Indikator, um die Kursentwicklung zu beurteilen, um Trends zu verfolgen.

Strategieprinzip

- Verwenden Sie den Heiken Ashi-Indikator, um Kerzen zu verarbeiten, Filter aus etwas Marktlärm und machen den Trend offensichtlicher

- Berechnung der oberen und unteren Bands des Supertrends anhand von ATR und Faktoren

- Wenn der Preis durch die obere Schiene bricht, ist es ein bärisches Signal.

- Je größer der Faktor, desto weniger Super Trend Signale, desto besser der Tracking-Effekt, aber die Anzahl der Einträge sinkt

- Kombination von Heiken Ashi und Super Trend Indikatoren zur Beurteilung und Verfolgung von Trends

Vorteile der Strategie

- Heiken Ashi Indikator filtert effektiv etwas Marktlärm und macht die Grafik klarer

- Der Super Trend-Indikator hat eine gute Optimierungseffekt und kann flexibel die Frequenz des Eintrags anpassen

- Durch die Kombination doppelter Indikatoren wird die Preisentwicklung besser beurteilt

- Automatische Verfolgung starker Trends

Risiken der Strategie

- Die Kombination der Indikatoren kann keine falschen Signale im Zeitraum der Marktkonsolidierung vollständig vermeiden.

- Große Lücken können zu ungültigen Indikatoren führen und somit wichtige Signalpunkte verpassen

- Wenn der Super Trend-Faktor zu groß eingestellt wird, werden Trendchancen verpasst.

Lösungen:

(1) Richten Sie die Super Trend-Parameter so ein, dass sie den Tracking-Effekt und die Eintrittsfrequenz ausgleichen

(2) Erhöhung anderer Indikatoren, die bei der Beurteilung helfen, um Probleme durch Lücken zu vermeiden

Optimierungsrichtung der Strategie

- Anpassung des ATR-Zyklus und des Super Trend-Faktors zur Optimierung der Eintrittsfrequenz

- Steigerung des Stop-Loss-Indikators zur Kontrolle einzelner Verluste

- Kombination anderer Indikatoren zur Bestimmung des Trendtyps, um einen unsachgemäßen Umgang mit dem Rhythmus von Trendschokken zu vermeiden

- Erhöhung von Algorithmen für maschinelles Lernen zur Beurteilung der Trendrichtung

Zusammenfassung

Diese Strategie integriert die Vorteile der doppelten Indikatoren Heiken Ashi und Super Trend, nutzt die Indikatoren, um die Richtung des Preistrends zu bestimmen, und erreicht automatische Verfolgung. Im Vergleich zu der Verwendung eines einzigen Indikators ist der Effekt der Beurteilung von Kursbewegungen besser und die Stabilität der Strategie wird verbessert. Natürlich gibt es noch Raum für Verbesserungen. In Zukunft kann die Optimierung aus den Aspekten der Eintrittsfrequenz und des Stop-Loss durchgeführt werden, um die Strategie profitabler und weniger riskant zu machen.

/*backtest

start: 2022-12-08 00:00:00

end: 2023-12-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © RingsCherrY

//@version=5

strategy("Heiken Ashi & Super Trend", overlay=true, pyramiding=1,initial_capital = 10000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.02)

///////////////////////////////////////////////////

////////////////////Function///////////////////////

///////////////////////////////////////////////////

heikinashi_open = request.security(ticker.heikinashi(syminfo.tickerid), timeframe.period, open)

heikinashi_high = request.security(ticker.heikinashi(syminfo.tickerid), timeframe.period, high)

heikinashi_low = request.security(ticker.heikinashi(syminfo.tickerid), timeframe.period, low)

heikinashi_close= request.security(ticker.heikinashi(syminfo.tickerid), timeframe.period, close)

heikinashi_color = heikinashi_open < heikinashi_close ? #53b987 : #eb4d5c

// plotbar(heikinashi_open, heikinashi_high, heikinashi_low, heikinashi_close, color=heikinashi_color)

x_sma(x, y) =>

sumx = 0.0

for i = 0 to y - 1

sumx := sumx + x[i] / y

sumx

x_rma(src, length) =>

alpha = 1/length

sum = 0.0

sum := na(sum[1]) ? x_sma(src, length) : alpha * src + (1 - alpha) * nz(sum[1])

x_atr(length) =>

trueRange = na(heikinashi_high[1])? heikinashi_high-heikinashi_low : math.max(math.max(heikinashi_high - heikinashi_low, math.abs(heikinashi_high - heikinashi_close[1])), math.abs(heikinashi_low - heikinashi_close[1]))

//true range can be also calculated with ta.tr(true)

x_rma(trueRange, length)

x_supertrend(factor, atrPeriod) =>

src = (heikinashi_high+heikinashi_low)/2

atr = x_atr(atrPeriod)

upperBand = src + factor * atr

lowerBand = src - factor * atr

prevLowerBand = nz(lowerBand[1])

prevUpperBand = nz(upperBand[1])

lowerBand := lowerBand > prevLowerBand or heikinashi_close[1] < prevLowerBand ? lowerBand : prevLowerBand

upperBand := upperBand < prevUpperBand or heikinashi_close[1] > prevUpperBand ? upperBand : prevUpperBand

int direction = na

float superTrend = na

prevSuperTrend = superTrend[1]

if na(atr[1])

direction := 1

else if prevSuperTrend == prevUpperBand

direction := heikinashi_close > upperBand ? -1 : 1

else

direction := heikinashi_close < lowerBand ? 1 : -1

superTrend := direction == -1 ? lowerBand : upperBand

[superTrend, direction]

///////////////////////////////////////////////////

////////////////////Indicators/////////////////////

///////////////////////////////////////////////////

atrPeriod = input(10, "ATR Length")

factor = input.float(3.0, "Factor", step = 0.01)

[supertrend, direction] = x_supertrend(factor, atrPeriod)

bodyMiddle = plot((heikinashi_open + heikinashi_close) / 2, display=display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style=plot.style_linebr)

downTrend = plot(direction < 0? na : supertrend, "Down Trend", color = color.red, style=plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps=false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps=false)

///////////////////////////////////////////////////

////////////////////Strategy///////////////////////

///////////////////////////////////////////////////

var bool longCond = na, var bool shortCond = na, longCond := nz(longCond[1]), shortCond := nz(shortCond[1])

var int CondIni_long = 0, var int CondIni_short = 0, CondIni_long := nz(CondIni_long[1]), CondIni_short := nz(CondIni_short[1])

var float open_longCondition = na, var float open_shortCondition = na

long = ta.change(direction) < 0

short = ta.change(direction) > 0

longCond := long

shortCond := short

CondIni_long := longCond[1] ? 1 : shortCond[1] ? -1 : nz(CondIni_long[1])

CondIni_short := longCond[1] ? 1 : shortCond[1] ? -1 : nz(CondIni_short[1])

longCondition = (longCond[1] and nz(CondIni_long[1]) == -1)

shortCondition = (shortCond[1] and nz(CondIni_short[1]) == 1)

open_longCondition := long ? close[1] : nz(open_longCondition[1])

open_shortCondition := short ? close[1] : nz(open_shortCondition[1])

//TP

tp = input.float(1.1 , "TP [%]", step = 0.1)

//BACKTESTING inputs --------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

testStartYear = input.int(2000, title="start year", minval = 1997, maxval = 3000, group= "BACKTEST")

testStartMonth = input.int(01, title="start month", minval = 1, maxval = 12, group= "BACKTEST")

testStartDay = input.int(01, title="start day", minval = 1, maxval = 31, group= "BACKTEST")

testPeriodStart = timestamp(testStartYear,testStartMonth,testStartDay,0,0)

testStopYear = input.int(3333, title="stop year", minval=1980, maxval = 3333, group= "BACKTEST")

testStopMonth = input.int(12, title="stop month", minval=1, maxval=12, group= "BACKTEST")

testStopDay = input.int(31, title="stop day", minval=1, maxval=31, group= "BACKTEST")

testPeriodStop = timestamp(testStopYear, testStopMonth, testStopDay, 0, 0)

testPeriod = true

// Backtest ==================================================================================================================================================================================================================================================================================================================================

if longCond

strategy.entry("L", strategy.long, when=testPeriod)

if shortCond

strategy.entry("S", strategy.short, when=testPeriod)

strategy.exit("TP_L", "L", profit =((open_longCondition * (1+(tp/100))) - open_longCondition)/syminfo.mintick)

strategy.exit("TP_S", "S", profit =((open_shortCondition * (1+(tp/100))) - open_shortCondition)/syminfo.mintick)

- Momentum-Indikator Handelsstrategie für Entscheidungen

- MACD-Lange Umkehrstrategie

- Strategie zur Nachverfolgung von Trends in zwei Zeiträumen

- Breakout-Strategie mit Bestätigung in mehreren Zeitrahmen

- Umfassende Strategie für mehrere Kerzenmuster

- Konsolidierungsausbruchsstrategie

- Vier EMA-Kreuzstrategie

- Quant Trading Strategie auf der Grundlage der monatlichen und vierteljährlichen gleitenden Durchschnittsoperation

- Eine Strategie der Kombination mehrerer Faktoren mit adaptiven gleitenden Durchschnitten

- EMA Golden Cross Kurzfristige Handelsstrategie

- Strategie zur Umkehrung der Abwärtsentwicklung

- Handelsstrategie mit dynamischem Momentumsoszillator

- WMX Williams-Fraktale Umkehrung Pivot-Strategie

- Stochastische Crossover-Lange- und Kurzstrategie

- Lineare MACD freischaltet die Magie der linearen Regression im TradingView

- Strategie zur Umkehrung der Drehzahl

- Valeria 181 Roboter Strategie verbessert 2.4

- Stochastische RSI-Strategie für den Handel mit Kryptowährungen

- Strategie zur Nachverfolgung von Trendwechseln

- Volumengewichtete gleitende Konvergenzdivergenz