Balancing listing strategies with teaching strategies

Author: Inventors quantify - small dreams, Created: 2020-09-02 17:05:25, Updated: 2024-12-10 10:09:34

Balancing listing strategies with teaching strategies

The essence of the strategy described here is a dynamic balancing strategy, which always balances the value of the coin to the value of the coin. Although designed to be pre-listed, the strategy logic is very simple. The main purpose of writing this strategy is to show all aspects of the strategy design.

-

Strategic logical wrapping Wrapping together some data, mark variables, and strategy logic at run time ("wrapping into objects").

-

Code that handles initialization tasks Initial account information is recorded at the initial run to be used for earnings calculations and whether data is recovered at the initial run based on parameter selection.

-

The code for strategic interaction processing A simple pause, continuous interaction is designed.

-

Code for the Strategic Benefit Calculation The earnings are calculated using the coin-bit method.

-

Key data persistence mechanisms in the strategy Mechanisms for designing data recovery

-

The code that shows the policy processing information The status bar data is displayed.

The Strategy Code

var Shannon = {

// member

e : exchanges[0],

arrPlanOrders : [],

distance : BalanceDistance,

account : null,

ticker : null,

initAccount : null,

isAskPending : false,

isBidPending : false,

// function

CancelAllOrders : function (e) {

while(true) {

var orders = _C(e.GetOrders)

if(orders.length == 0) {

return

}

Sleep(500)

for(var i = 0; i < orders.length; i++) {

e.CancelOrder(orders[i].Id, orders[i])

Sleep(500)

}

}

},

Balance : function () {

if (this.arrPlanOrders.length == 0) {

this.CancelAllOrders(this.e)

var acc = _C(this.e.GetAccount)

this.account = acc

var askPendingPrice = (this.distance + acc.Balance) / acc.Stocks

var bidPendingPrice = (acc.Balance - this.distance) / acc.Stocks

var askPendingAmount = this.distance / 2 / askPendingPrice

var bidPendingAmount = this.distance / 2 / bidPendingPrice

this.arrPlanOrders.push({tradeType : "ask", price : askPendingPrice, amount : askPendingAmount})

this.arrPlanOrders.push({tradeType : "bid", price : bidPendingPrice, amount : bidPendingAmount})

} else if(this.isAskPending == false && this.isBidPending == false) {

for(var i = 0; i < this.arrPlanOrders.length; i++) {

var tradeFun = this.arrPlanOrders[i].tradeType == "ask" ? this.e.Sell : this.e.Buy

var id = tradeFun(this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount)

if(id) {

this.isAskPending = this.arrPlanOrders[i].tradeType == "ask" ? true : this.isAskPending

this.isBidPending = this.arrPlanOrders[i].tradeType == "bid" ? true : this.isBidPending

} else {

Log("挂单失败,清理!")

this.CancelAllOrders(this.e)

return

}

}

}

if(this.isBidPending || this.isAskPending) {

var orders = _C(this.e.GetOrders)

Sleep(1000)

var ticker = _C(this.e.GetTicker)

this.ticker = ticker

if(this.isAskPending) {

var isFoundAsk = false

for (var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_SELL) {

isFoundAsk = true

}

}

if(!isFoundAsk) {

Log("卖单成交,撤销订单,重置")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

if(this.isBidPending) {

var isFoundBid = false

for(var i = 0; i < orders.length; i++) {

if(orders[i].Type == ORDER_TYPE_BUY) {

isFoundBid = true

}

}

if(!isFoundBid) {

Log("买单成交,撤销订单,重置")

this.CancelAllOrders(this.e)

this.arrPlanOrders = []

this.isAskPending = false

this.isBidPending = false

LogProfit(this.CalcProfit(ticker))

return

}

}

}

},

ShowTab : function() {

var tblPlanOrders = {

type : "table",

title : "计划挂单",

cols : ["方向", "价格", "数量"],

rows : []

}

for(var i = 0; i < this.arrPlanOrders.length; i++) {

tblPlanOrders.rows.push([this.arrPlanOrders[i].tradeType, this.arrPlanOrders[i].price, this.arrPlanOrders[i].amount])

}

var tblAcc = {

type : "table",

title : "账户信息",

cols : ["type", "Stocks", "FrozenStocks", "Balance", "FrozenBalance"],

rows : []

}

tblAcc.rows.push(["初始", this.initAccount.Stocks, this.initAccount.FrozenStocks, this.initAccount.Balance, this.initAccount.FrozenBalance])

tblAcc.rows.push(["当前", this.account.Stocks, this.account.FrozenStocks, this.account.Balance, this.account.FrozenBalance])

return "时间:" + _D() + "\n `" + JSON.stringify([tblPlanOrders, tblAcc]) + "`" + "\n" + "ticker:" + JSON.stringify(this.ticker)

},

CalcProfit : function(ticker) {

var acc = _C(this.e.GetAccount)

this.account = acc

return (this.account.Balance - this.initAccount.Balance) + (this.account.Stocks - this.initAccount.Stocks) * ticker.Last

},

Init : function() {

this.initAccount = _C(this.e.GetAccount)

if(IsReset) {

var acc = _G("account")

if(acc) {

this.initAccount = acc

} else {

Log("恢复初始账户信息失败!以初始状态运行!")

_G("account", this.initAccount)

}

} else {

_G("account", this.initAccount)

LogReset(1)

LogProfitReset()

}

},

Exit : function() {

Log("停止前,取消所有挂单...")

this.CancelAllOrders(this.e)

}

}

function main() {

// 初始化

Shannon.Init()

// 主循环

while(true) {

Shannon.Balance()

LogStatus(Shannon.ShowTab())

// 交互

var cmd = GetCommand()

if(cmd) {

if(cmd == "stop") {

while(true) {

LogStatus("暂停", Shannon.ShowTab())

cmd = GetCommand()

if(cmd) {

if(cmd == "continue") {

break

}

}

Sleep(1000)

}

}

}

Sleep(5000)

}

}

function onexit() {

Shannon.Exit()

}

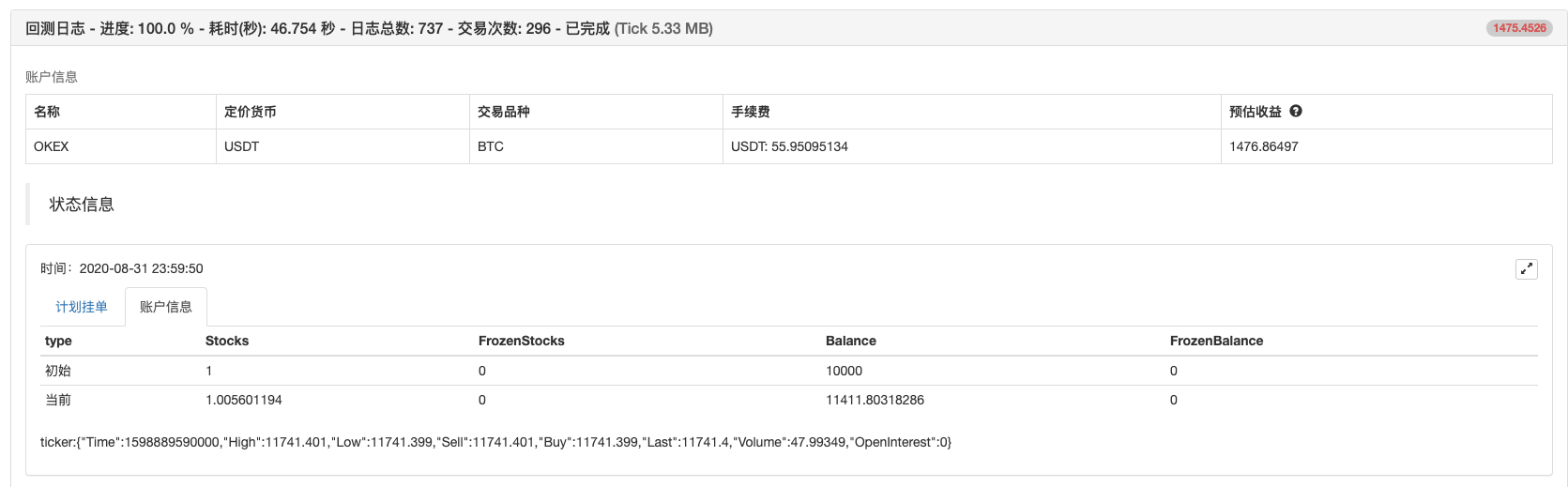

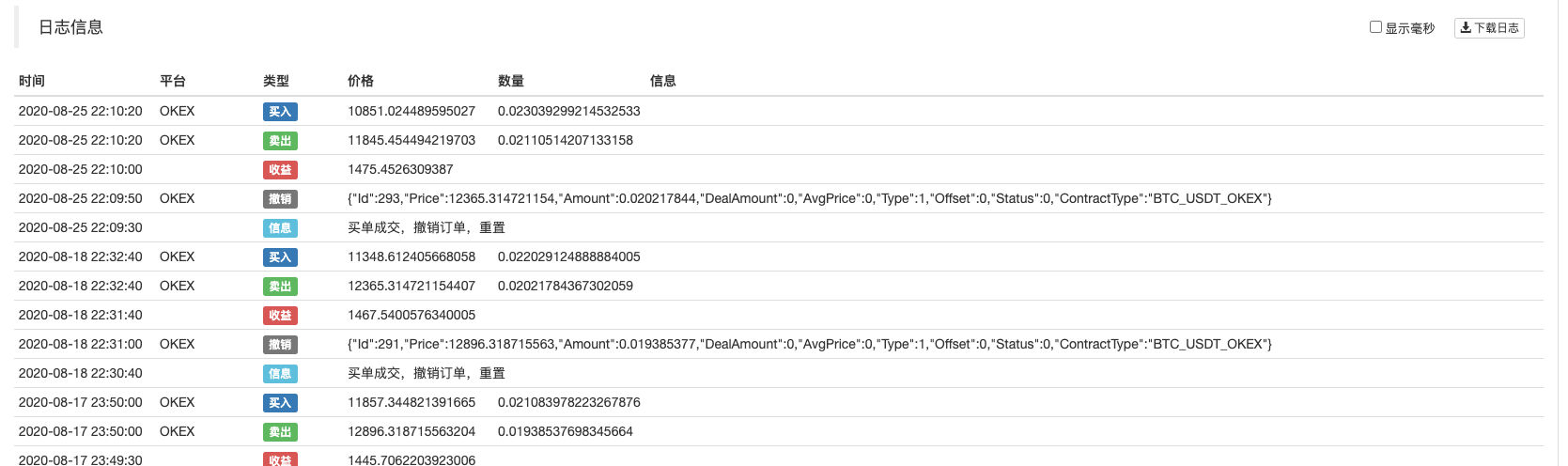

The retest is running

Optimized expansion

- The virtual listing mechanism can be added, and some trades all the listing limits, so it is possible that the order will not actually be hung, and you need to wait for the price to get closer to the real listing.

- Joining the futures market

- Expanded to multi-variety, multi-exchange version

The tactics are only for teaching purposes and should be used sparingly. The policy address:https://www.fmz.com/strategy/225746

- Introduction to Lead-Lag Arbitrage in Cryptocurrency (2)

- Introduction to the Lead-Lag suite in the digital currency (2)

- Discussion on External Signal Reception of FMZ Platform: A Complete Solution for Receiving Signals with Built-in Http Service in Strategy

- Discussing FMZ platform external signal reception: a complete set of strategies for the reception of signals from built-in HTTP services

- Introduction to Lead-Lag Arbitrage in Cryptocurrency (1)

- Introduction to the Lead-Lag suite in digital currency (1)

- Discussion on External Signal Reception of FMZ Platform: Extended API VS Strategy Built-in HTTP Service

- External signal reception on FMZ platforms: extended API vs. built-in HTTP services

- Discussion on Strategy Testing Method Based on Random Ticker Generator

- Strategy testing methods based on random market generators explored

- New Feature of FMZ Quant: Use _Serve Function to Create HTTP Services Easily

- How to dissect cabbage harvesters (1)

- Years from now, you'll feel like this is the most valuable article in your investment career, figuring out the source of the return and the source of the risk.

- 5 bands 80 times the power of high-frequency tactics

- Futures counter-hand doubled algorithm strategy commentary details

- Simply put, why is it not feasible to move OKEX's assets through a contractual hedging strategy?

- Thinking about moving assets through a contract hedging strategy

- Visualize editing strategies to extend custom libraries

- Solution for getting a host to send an HTTP request message

- Use of servers in quantitative transactions

- [Millennium War] Bitcoin exchange rate approximate strategy 3 butterfly hedging

- RSI2 Mean Reversion Strategy using in futures

- The futures and cryptocurrency API explanation

- Quickly implement a semi-automatic quantitative trading tool

- Introducing the Aroon indicator

- Preliminary Study on Backtesting of Digital Currency Options Strategy

- The Difference between Quantitative Trading and Subjective Trading

- ATR Channel strategy Implemented on crypto market

- Thermostat Strategy using on crypto market by MyLanguage

- hans123 intraday breakthrough strategy

- Digital currency options strategy back to basics