Bandpass Filter Reversed Strategy

Author: ChaoZhang, Date: 2024-01-24 15:28:26Tags:

Overview

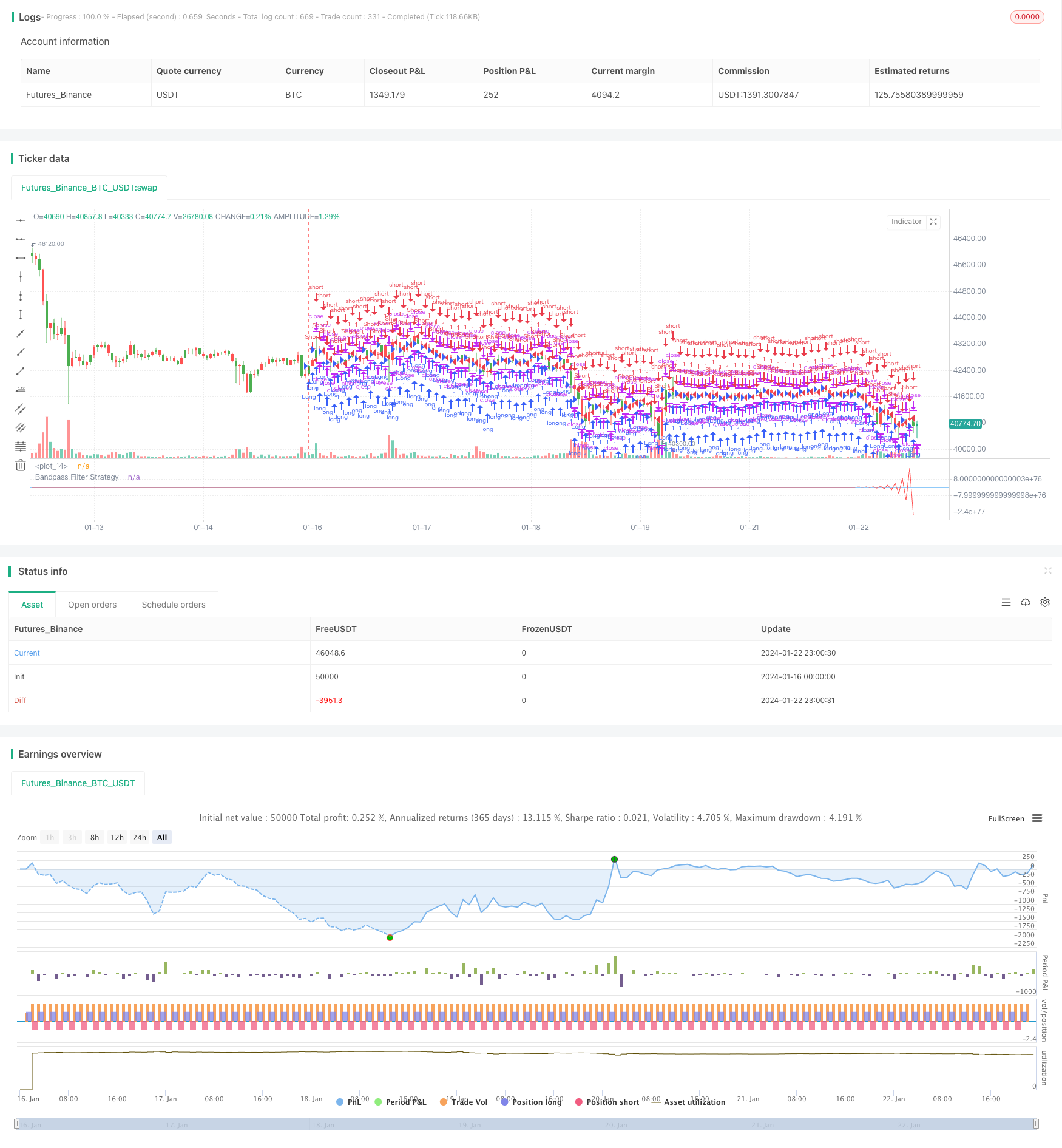

The Bandpass Filter Reversed Strategy is a stock trading strategy based on bandpass filters. It constructs a cos and sine function to simulate a bandpass filter and generates buy and sell signals. When the filter output exceeds or falls below a certain trigger level, the strategy will take reverse operations, i.e. buying or selling.

Strategy Principle

The core of this strategy is to build a bandpass filter BP, which consists of two parameters: center frequency and bandwidth. The center frequency determines the main cycle passed by the filter, and the bandwidth determines the range of passed cycles. These parameters determine the transfer characteristic of the filter.

Specifically, the strategy constructs the following variables:

- Length: Center cycle of the filter

- Delta: Bandwidth parameter

- Beta: Coefficient related to center frequency

- Gamma: Coefficient related to bandwidth

- Alpha: Intermediate variable related to Beta and Gamma

According to these variables, the strategy builds a first-order IIR (Infinite Impulse Response) filter:

BP = 0.5*(1 - alpha)*(xPrice - xPrice[2]) + beta*(1 + alpha)*nz(BP[1]) - alpha*nz(BP[2])

When BP is above or below TriggerLevel, the strategy will take actions in the opposite direction.

Advantage Analysis

The main advantages of this strategy are:

- Using a bandpass filter can remove high and low frequency noise and only extract useful medium frequency cycle signals to improve signal-to-noise ratio.

- It is relatively simple and intuitive. Only a few parameters need to be adjusted to adapt to different cycles and market environments.

- Adopting a reverse strategy can timely capture short-term price reversal and quickly close positions after profiting to reduce holding risks.

Risk Analysis

This strategy also has some risks:

- The parameter settings of the bandpass filter need to be adjusted according to different cycles and market environments. If set improperly, it will miss trading opportunities or generate more false signals.

- Reversal strategies are prone to illusion reversals. If the reversal fails and the price continues in the original direction, it will cause losses.

- The trading frequency may be high. It is necessary to prevent over-optimization and control trading costs.

To reduce these risks, the following optimization methods can be considered:

- Use adaptive filters to automatically adjust parameters based on market changes.

- Combine trend filters to avoid opening positions against the trend.

- Optimize parameter combinations to make strategies parameterized to adapt to more market conditions.

Optimization Directions

The main aspects that this strategy can be optimized include:

-

Cycle and parameter self-adaptation: Dynamically adjust parameters such as Length and Delta according to different cycles and recent price movements in a time window, so that the filter adapts to market environment changes in real time.

-

Combine with trend judgment: On the basis of the bandpass filter, technical indicators such as MACD and MA are added to determine the trend direction and avoid opening positions against the trend.

-

Multi-timeframe combination: Deploy strategies on multiple time frames (such as 5 minutes, 15 minutes, 30 minutes, etc.). Perform signal verification between different time frames to improve signal accuracy.

-

Stop loss mechanism: Set reasonable stop loss positions. Take the initiative to close positions when losses reach stop loss bits to effectively control the size of single losses.

Through the above optimizations, the stability, adaptability and profitability of the strategy can be greatly improved.

Summary

The Bandpass Filter Reversed Strategy extracts useful medium-frequency signals by constructing a bandpass filter, and takes reverse operations when the filter output triggers the level to capture short-term price reversal opportunities. The strategy is relatively simple. Through parameter optimization, it can adapt to various market environments. The main optimization directions include adaptive filters, trend judgments, multi-timeframe combinations, stop loss mechanisms, etc.

/*backtest

start: 2024-01-16 00:00:00

end: 2024-01-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version = 2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 24/11/2016

// The related article is copyrighted material from

// Stocks & Commodities Mar 2010

// You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

// Please, use it only for learning or paper trading. Do not for real trading.

////////////////////////////////////////////////////////////

strategy(title="Bandpass Filter Reversed Strategy")

Length = input(20, minval=1)

Delta = input(0.5)

TriggerLevel = input(0)

xPrice = hl2

hline(TriggerLevel, color=blue, linestyle=line)

beta = cos(3.14 * (360 / Length) / 180)

gamma = 1 / cos(3.14 * (720 * Delta / Length) / 180)

alpha = gamma - sqrt(gamma * gamma - 1)

BP = 0.5 * (1 - alpha) * (xPrice - xPrice[2]) + beta * (1 + alpha) * nz(BP[1]) - alpha * nz(BP[2])

pos = iff(BP > TriggerLevel, -1,

iff(BP <= TriggerLevel, 1, nz(pos[1], 0)))

if (pos == 1)

strategy.entry("Long", strategy.long)

if (pos == -1)

strategy.entry("Short", strategy.short)

barcolor(pos == -1 ? red: pos == 1 ? green : blue )

plot(BP, color=red, title="Bandpass Filter Strategy")

- RSI and EMA Based Trend Following Strategy

- Trend Confirmation Tracking Strategy

- The RSI Divergence Indicator Strategy

- Momentum Moving Average Consolidation Strategy

- Fast QQE Crossover Trading Strategy Based on Trend Filter

- Adaptive Moving Average Tracking Strategy

- Scalping Strategy in Trend Reversal Market

- Bidirectional EMA Cross Quant Trading Strategy

- EMA Intraday Scalping Strategy

- Compound Stop Loss and Take Profit Strategy Based on Random Entry

- Dual Moving Average Crossover Trading Strategy

- RSI Combined with Bollinger Bands and Dynamic Support/Resistance Quantitative Strategy

- Dynamic Dual EMA Trailing Stop Strategy

- Multi-indicator Combined Quantitative Trading Strategy

- Contrarian Donchian Channel Touch Entry Strategy with Post-Stop Loss Pause and Trailing Stop Loss

- Intraday Single Candle Indicator Combo Short Term Trading Strategy

- Moving Average Crossover Trading Strategy

- RSI Bollinger Bands Trading Strategy

- Trend Following Strategy Based on Dual EMA

- Dual Moving Average Breakout Strategy